I am very fortunate that many of my choices created amazing opportunities over the years. One was my selection of my final accounting course: Tax Research, Practice and Procedures. Although I was never motivated by governmental accounting, this course was also a requirement for the master’s level program. I achieved the second highest grade in the class, a C+. The highest grade was a B.

This extremely difficult class changed my life. I learned how to be transformative with the businesses and business owners I serve, particularly in helping them benefit from well-designed ERISA retirement plans. (As an aside, if anyone can introduce me to Shark Tank’s Daymond John, let me know. From what I can tell, he is probably missing a $40M tax deduction unrelated to retirement plans.)

Retirement plans can provide benefits that create scale in ways that few financial professionals really share or understand. The tax and regulatory incentives often go unnoticed and underutilized.

As we know, business owners take deductions all the time for the benefit of not paying taxes. I routinely see them buy equipment they can fully deduct in the year bought just so they don’t have to pay the taxes. Ten years later, the equipment is still new.

Retirement plans not only offer a tax deduction for business owners, but can be advantageous for their retirement and estate planning. In addition to tax incentives, there are also regulatory incentives. Combining these incentives greatly reduces business owners’ out-of-pocket costs — sometimes by up to 75%. Perhaps by even more.

What follows is a roadmap regarding these incentives and some real-world perspectives. You might first want to review the major kinds of retirement plans and how to indulge in the three layers of the retirement plan cake.

Tax Incentives

Adopting retirement plans offers layers of tax incentives. Some are obvious; others may reveal themselves through the planning process. The industry, and your client, will typically focus on the total top-line number, not the out-of-pocket costs. Professionals should help the client focus on the bottom-line impact of employer contributions to retirement plans.

Many business owners have worked very hard building their businesses. Some have worked 80- to 100- hour work weeks and now want to save money for retirement after investing their time, effort and money into their business for a decade or two. Acquiring and sharing knowledge about tax incentives with your clients will significantly reduce their out-of-pocket costs.

Plan sponsors have the option to pay for various expenses or pass along these expenses to their plan

participants. It’s important to note that tax incentives only apply to the payments a plan sponsor makes, not the costs they pass along to participants.

Familiar Tax Incentives

Many of us are aware of some basic tax credits and tax deductions although we may not all know the specifics.

Section 104 of the SECURE Act increases the tax credit small business owners may apply to the startup costs of pension plans launched after December 31, 2019. The tax credit may be applied for up to three years and caps out at $5,000.

Employers who adopt an automatic enrollment arrangement get a $500 tax credit. Automatic enrollment is formally known as a Qualified Automatic Contribution Arrangement (QACA).

Employers may also deduct whatever they do not get as a credit for plan expenses. This includes contributions to the plan for employees.

Lesser-Known Tax Incentives

Employers generally do not have to pay Social Security, Medicare or worker’s compensation taxes on the contributions they make on behalf of their workers to a 401(k), profit-sharing or cash balance plan. These social insurance payments can add up to a noticeable portion of wages for jobs in construction (30%), agriculture (20%) and service-based businesses (10%).

Construction companies seeking government contracts are often required to pay a higher prevailing wage that includes a variety of benefits for employees. Let’s say an electrician on a prevailing wage contract is paid $80 per hour. The prevailing wage schedule may list health insurance at $10.53 per hour, pension plan contributions at $14.43 per hour.

Service-based businesses like medicine, law, accounting and consulting, as well as many others, may also enjoy increased deductions due to qualified business incentive deductions under Section 199A of the Internal Revenue Code. If your client qualifies, it may reduce their taxes by more than $15,000 with no out-of-pocket expenditures.

The employee benefits too. They do not have Social Security taxes withheld on matching and profit-sharing contributions received from their employer. Cash balance plan contributions have similar favorable benefits.

Regulatory Incentives

Regulatory incentives also greatly reduce the cost of retirement plans for your client. While tax incentives are recognized when a tax return is filed, regulatory incentives are recognized the year after an employee who has not satisfied the employment requirements for the plan leaves the business.

Each layer of the retirement plan cake allows the business owner to recapture the employer’s contribution to the employee’s 401(k) plan if the employee does not stay with the company long enough to be fully vested. The recapture of the employer payments made are transferred to a forfeiture account. Money in the forfeiture account can be applied against plan expenses for the next year’s funding of profit-sharing and cash balance plan contributions.

Here are the general rules regarding vesting:

Profit-sharing non-elective safe harbor

The employer’s contributions typically vest immediately. The exception is if the plan includes an automatic enrollment feature. It is in the best interest of the participants to include an automatic enrollment feature (QACA), as established under the Pension Protection Act of 2006. If a QACA is adopted, your client can recapture in the plan’s forfeiture account any contributions made during the first two years of an employee’s eligibility.

Profit-sharing other than non-elective contributions

Other profit-sharing contributions can be subject to a six-year graded vesting schedule. This means that each year your client’s employee has satisfied eligibility, the employee is entitled to a greater percentage of the account balance. The amount due to the employee is said to be vested. A common vesting schedule over the six years is 0%, 20%, 40%, 60%, 80%, 100%.

In an employment environment where it is difficult to find employees, and competitors offer more to our employees resulting in turnover, this portion of a profit-sharing plan can be a good opportunity to attract and retain key employees.

Cash balance plans

A cash balance plan usually implements a three-year-cliff vesting schedule. (Participants become fully vested after three years of service, but are not vested at all prior to that.) If your client experiences a 25% turnover rate annually, using this vesting schedule may be able to reduce their plan-funding costs over time by about 50%.

Offering the different layers of the retirement plan cake can also help your business-owner clients attract and retain a more experienced workforce. This, too, can ultimately save them money in other ways. Training employees takes time, costs money and reduces productivity. Newer employees also tend to give customers the wrong answers and make more mistakes. One employer we spoke with in the agriculture industry said he sustains equipment breakage costs of $10,000 to $20,000 per employee in their first year. Having a more experienced workforce that knows the culture and procedures of your client’s business reduces costs

Integrating Retirement Plans for Success

The opportunities around retirement plans are enormous. Explaining the concept of the retirement plan cake to business owner clients is a simple and effective way to share with your clients what their options are. Explaining how they can tweak their current plans will also greatly improve plan outcomes.

For example, amending the plan to include automatic enrollment at 5% and automatic escalation will increase participation in your 401(k) plans. The U.S. House of Representatives recognized the importance of automatic enrollment by including it in the H.R. 2954 Securing A Strong Retirement Act of 2021 (SECURE Act 2.0) that passed in early 2022.

Plans that integrate both tax incentives and regulatory incentives can see powerful results. In fact, small companies with 10 or fewer employees have the potential to have a negative cost when all the tax and regulatory incentives are taken into consideration. Your business owner client could receive a significant tax-deductible contribution and contribute a significant amount to their Roth 401(k).

Hypothetical and Real-Life Examples

Here are ways retirement plans can be tweaked for different size businesses.

Typical Small Company

My office recently made a proposal for a company with 70 employees. Many of those employees are under 21 and work part-time. A plan document can exclude employees younger than 21 from participation in a plan even if they work full time. However, part-time employees who work more than 1,000 hours a year can be considered eligible employees. In this particular business owner’s case, only five out of the 70 employees were considered eligible along with the husband and wife.

But don’t assume a cash balance plan is inappropriate if a company employs many low-paid workers; it’s always important to have a third-party administrator and an actuary work together to run the numbers.

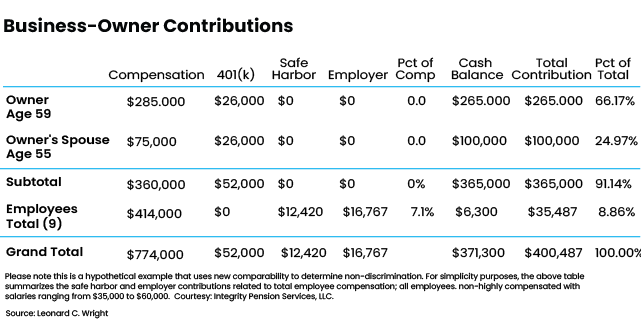

The chart below, simplified for illustrative purposes, shows the contributions a hypothetical business owner would be required to contribute to employees on the different layers of the retirement plan cake. The company is run by a husband and wife and has nine eligible employees. For simplicity, we’ll assume the nine eligible employees don’t make salary deferrals and the employer makes contributions for them.

If set up properly, the safe-harbor-contribution layer ($12,420) can be subject to a two-year cliff vesting schedule; the profit-sharing contribution ($16,767) can be set up with a six-year graded vesting schedule.; and the cash-balance-plan contribution ($6,300) can be set up with a three-year cliff vesting schedule. Total contribution to employees as shown in the chart is $35,487.

Together, the spouses who work in the example business contribute $52,000 in salary deferrals to their 401(k) plans and $365,000 to their cash-balance plan. Their total salary deferrals and cash balance plan contributions are $417,000.

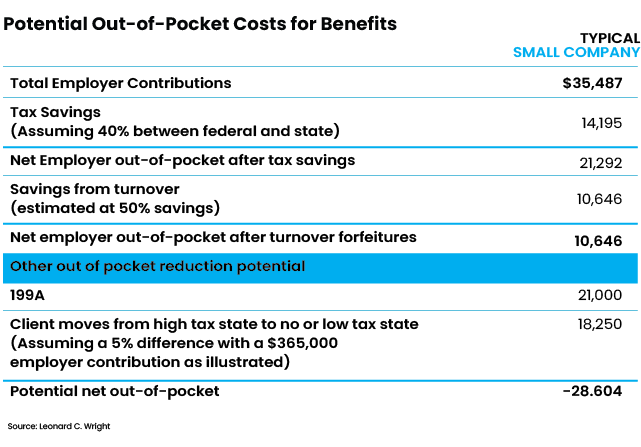

Now here’s where it gets more interesting. Although the employer’s total contributions for employees is $35,487, he could wind up paying only $10,646 out-of-pocket to give employees this $35,487 benefit, as illustrated in the next chart below.

First, I assumed a savings that will come from a 40% tax rate for the business which includes state, local and federal income taxes. Business owners don’t have to pay taxes on contributions to workers so this resulted in a tax reduction in the current year of $14,195 ($35,487 x 0.4). Next, I assumed a 50% reduction in costs ($10, 646) from forfeiture of employer contributions made to employees who left the firm before being fully vested. The client also qualified for a Section 199A deduction of $21,000. Finally, the client moved from a state with high income taxes to a state with low (or no) income taxes – a 5% difference in tax rates. That resulted in a tax savings of $18,250 ($365,000 total retirement plan contributions x .05). All told, the employer could receive a net out-of-pocket benefit of $28,604 from setting up a cash balance plan.

The benefits of small business cases are far greater than communicated by the retirement plan industry. Remember, the results will be different for companies each year. Your clients’ outcomes will vary depending on the planning. Any tax savings will be received each year at tax time, but it’ll take a while for the savings from turnover to be realized.

Larger Businesses

Many third-party administrators that offer cash balance plans specialize in small businesses that generally have 15 or fewer employees. However, cash balance plan presentations should be considered for just about any company that has up to 100 employees per member, shareholder or partner. When out-of-pocket costs are considered, cash balance plans carry significant benefits that are not perceived when examining top-line outcomes.

Let’s look at a hypothetical company that has 65 eligible employees.

In recent years, it the business has undergone with two key changes:

Owner compensation has increased, which enables the business owner to save more.

The plan has shifted from a matching safe-harbor plan to a non-elective profit-sharing safe harbor. The outcome is:

a. Greater contribution for the business owners.

b. Reduced contribution to the employees. The safe-harbor match does not count toward the integrated profit-sharing and cash-balance testing; the non-elective safe-harbor profit-sharing contribution does. This makes those contributions more effective and reduces the total required employee contributions.

The business owner in the example above does not have a cash-balance plan and did not take into account other tax and regulatory incentives that may have been available. However, it’s important to explain these concepts up front when speaking with clients and prospects.

Simple Math, Big Influence

When a prospect is considering adding a cash balance plan to an existing 401(k) plan, segregate the additional costs associated with the plan and highlight that, not the total cost.

I would suggest, since most plans require about a 7% profit sharing contribution and $1,000 cash balance plan contribution per employee, to use this math when explaining this concept to prospects. Here’s what it would look like:

If payroll is $3,000,000 per year and there are 80 eligible employees, this results in $210,000 for a profit-sharing contribution ($3,000,000 x .07) plus $80,000 (80 x $1,000) for the cash balance plan contribution. If the business owner was already providing a match or a profit-sharing contribution of $90,000 per year in their existing retirement plan, their extra cost to add a different profit-sharing and a cash-balance plan would be only $200,000 ($210,000 + $80,000 – $90,000). Throw in the tax and regulatory incentives and the estimated additional out-of-pocket cost could be only $50,000 ($200,000 x 0.5 tax rate x 0.5 regulatory incentives).

If the business owner is in their late 50s and their spouse works in the business, it is possible they could achieve a $500,000 tax deduction — a significant opportunity for your client. It’s also an amazing opportunity to get low-income and minority communities on track for retirement. And you will be there to help your client achieve success.

The benefits of small business cases are far greater than shared. The assumptions of how the out-of-pocket costs are computed and what other tax benefits there may be with clients that are small service-based businesses and those who may be contemplating a move from a state that has high taxes to a lower tax state produce significant benefits. And, the differences can be more significant. I assumed a 40% tax rate for the business which includes state, local, and federal income taxes. That is a reduction of taxes in the current year of $14,195 in the example. The example assumes a 50% reduction in cost due to a turnover of an additional $10,646. Remember, results will be different by company by year. There are a couple other opportunities that the chart shares, 199A small business deductions and/or moving out of state. With the additional permanent elimination of taxes, it is quite favorable to set up a cash balance plan, and in this case, the client benefits significantly over $28,000.

There are significant benefits to most profitable companies. Companies that have up to 100 employees per shareholder, partner, or member should have an analysis run by a third-party administrator to determine the opportunities for the company. Smaller companies that have a reasonable profit margin should have a third-party administrator run what benefits there may be now or at some time in the future. The planning around ERISA plans (401 (k)/Profit Sharing, and cash balance plans), engages your client in discussions around corporate culture and what is in the best interest of the business, its participants, and the business owner. These discussions can open additional opportunities around business buy-sell planning, personal investments, and risk management planning.

Leonard C. Wright, CPA/PFS, CGMA, AIF, CFP, CLU, ChFC is the past chair of the Member Retirement Plan Committee at the Association of International Certified Professional Accountants (AICPA). His mission is to create clarity around the opportunities ERISA plans can provide to business owners, key employees and all plan participants who help them grow their businesses. He has clients across the U.S. His team’s mission statement is “Working together to achieve financial success through understanding, education, and action.”