Thanks to the SECURE Act signed into law in December 2020, this year was the first year where a business owner could adopt an ERISA plan to potentially receive a significant tax deduction for the prior year as long as they funded the plan before they filed their tax return in the current year. Although the 2020 tax year is over for business owners with a calendar year end at 12/31/2020, there are many businesses who have their fiscal year-end for 2020 sometime this year.

While many businesses were adversely impacted by COVID-19, there were also many businesses that thrived and had record years during these unprecedented times. This includes mortgage brokers and many in construction, technology and medicine, to name a few. One small business owner consulted our team because the company had the best year ever and was anticipating a substantially higher tax bracket than in the past due to the pass-through nature of its corporate structure. Through the “retirement plan cake,” we were able to plan for a $200,000-plus tax deduction in 2020.

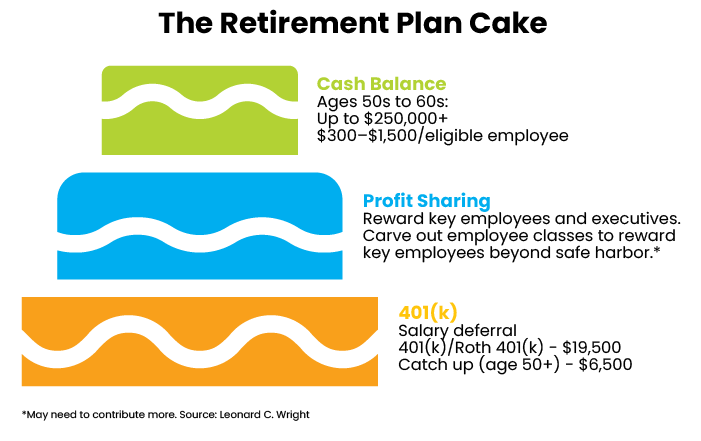

Most are familiar with the first two layers of the retirement plan cake – 401(k) and Profit Sharing.

Layer 1: 401(k) Plan

The first layer is the 401(k) plan where employees may contribute up to $19,500 (plus $6,500 if over age 50) per year through salary deferral either on a pre-tax or Roth basis. While many are accustomed to 401(k) plans, few business owners and highly compensated employees understand that they can potentially contribute up to $26,000 per year to a Roth at age 50; they typically figure they make too much money to save to a Roth but, though that may be true for Roth IRAs, that rule does not apply to Roth-designated accounts in 401(k) plans.

For business owners and highly compensated employees to contribute the maximum amounts, the plan should include a safe harbor. That way they don’t have to worry about receiving a refund at the end of the year because the non-highly compensated employees didn’t save enough to their plan. There are essentially two options for safe harbor – 1. safe harbor match, or 2. safe harbor non-elective. There’s also a third option that’s generally less known, which is Qualified Automatic Contribution Arrangement or “QACA.” How you decide to set up the plan for safe harbor impacts the next layer of the retirement plan cake.

Layer 2: Profit-Sharing Plan

The next layer is the profit-sharing plan. This layer is important because you may be able to use these contributions to arrive at optimal results in the top layer. Moreover, business owners can reward key employees through profit-sharing contributions rather than bonuses. Often, there are a handful of employees within a business that help the owner drive outcomes and profits. If the employee makes less than $130,000 per year and is not related to the owner, they may be eligible for unique rewards beyond the safe harbor contribution. For example, one of our business owner clients wanted to celebrate her employee’s 25th work anniversary by giving them $25,000 that year. Because of how the profit-sharing plan is set up, our client was able to make a $25,000 contribution to that individual’s profit-sharing plan without having to do anything extra for the rest of her employees.

Layer 3: Cash-Balance Plan

The final layer, with all the goodies at the top, is the cash-balance plan. This is a defined benefit plan whereas the first two layers are defined contribution plans. The cash balance plan proposal is created using actuarial valuations based on the company’s census and past data. How much the business owner can contribute for themself will be calculated using their highest three years of consecutive income since the company’s inception. Many business owners tend to pay themselves a lower salary so it may make sense to increase their compensation for a few years to achieve better tax deductions in the future through the cash balance plan.

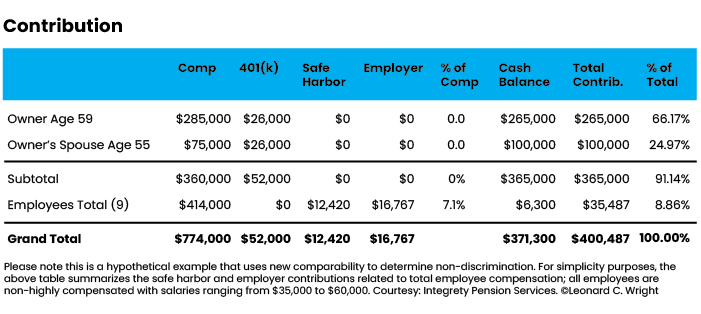

In the above example, the owner and spouse both work in the business and there are nine total employees. Since the owner and spouse are in their 50s, together they could potentially save up to $52,000 on a tax-free growth basis through the first layer, the 401(k) plan. For the owners to save the maximum 401(k) amount, this illustration uses the safe harbor non-elective contribution.

The next layer, the profit-sharing plan, serves as a gateway to the cash balance plan; in this example, the employer must give 7.1% of the employees’ compensation in the profit-sharing plan to potentially receive a $365,000 tax deduction via the cash balance plan. This results in 91% of the total contributions going to the owners and only about 9% to the employees. However, 9% may be less over time if there is high turnover in the company because each of these layers including the safe harbor arrangement may be tied to a vesting schedule if the plan is properly set up.

There is significant opportunity for meaningful tax deductions through retirement plans, especially because we’re now able to offer this as a solution retroactively. Another benefit of the SECURE Act is that it boosted tax credits around adoption of a plan; employers now receive a tax credit of $250 per non-highly compensated eligible participant, capping out at 50% of eligible expenses up to a maximum of $5,000.

It’s important to work with a solid team of professionals in this niche because many advisors tend to be dabblers rather than retirement plan specialists. Most plans tend to be cookie-cutter plans and lack the necessary features to achieve the best outcomes. There are many moving parts and it’s essential to customize the retirement plan to fit the company’s unique corporate culture to get the most value out of the plan. The client’s goals and objectives should be kept at the center and the team of professionals which includes the advisor, CPA, third-party administrator and recordkeeper should be working together to provide ideas and solutions in the best interest of the client.

Amie Agamata, CFP, AIF, RICP, ChFC, CLU, is a financial planner in San Diego, Calif. She serves as the NexGen President for the Financial Planning Association (FPA) of San Diego and is member of the FPA Retirement Income Planning Advisory Council. She is the incoming FPA National NexGen President-Elect in 2022.