When I was the COO/CFO of one of America’s top jewelers, I created a marketing program during a recession that no other firm in the U.S. had ever imagined before. Recessions in the jewelry industry are really depressions. Jewelers were failing across America with revenues off by half or more, yet our firm revenues were up by over 80%. Our profits skyrocketed with no reduction of gross margin.

Many years later, I shared how I achieved the impossible with one of the top leaders in the jewelry industry. He looked at me and said, “It will never work.” He made it fit inside his box of expectations for a marketing program and therefore couldn’t make sense of it. But I wasn’t asking for his opinion; I was giving him a gift.

I share this story because it’s similar to the approach of many retirement plan professionals I encounter. Like the jewelry executive, they often look at what they know to be true in their world and fail to look outside their box. As a financial advisor, you can help small-business owners if you think bigger. Help them determine how a retirement plan fits into their overall financial plan. But first, you must learn as much about retirement plans as you can.

This article is the first in a series that will help familiarize you with the five major components of retirement plans. You can transform your business by becoming part of a team that helps deliver expertise on retirement plans, which are often misunderstood and underutilized.

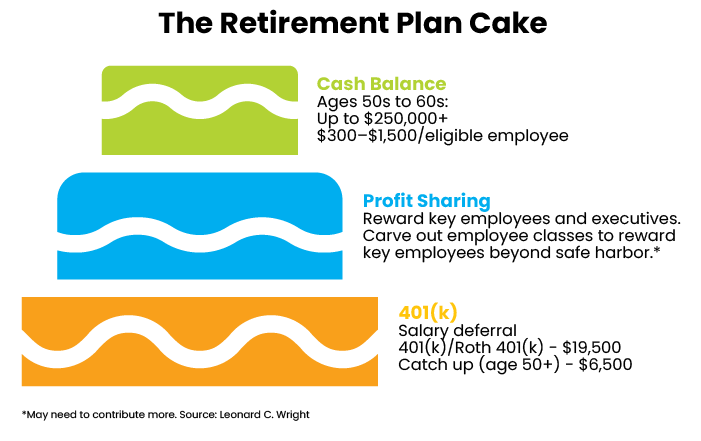

This article will provide an overview of the three major kinds of retirement plans: the 401(k) plan, the profit-sharing plan and the cash-balance pension plan. I call them the layers in the retirement-plan cake; coordinating them will deliver opportunities for your clients. With defined contribution plans such as 401(k)s and profit-sharing, the business owner defines what they contribute. The cash-balance plan is a defined benefit plan that provides a stated cash balance.

In subsequent articles, we’ll revisit these plans and dive deeper into tax and regulatory incentives, how to integrate these plans so they fit into a client’s financial plan and business culture, and how to educate members of your team.

401(k) Plans

According to the Investment Company Institute, there are about 600,000 401(k) plans with 60 million participants and $7.3 trillion under management. Considering the U.S. has about 6.1 million small businesses with employees, the opportunity for advisors to help employers start new plans is vast.

Business owners, the plan sponsors, can select traditional deferrals, Roth deferrals or non-deductible deferrals for their 401(k) plans. They can match their employees’ contributions, depending on the retirement plan message they wish to send to their employees. The first plan I set up in 1988 was a 25% match of employee contributions up to 4% of the employee’s income. Many employers today match 50% up to 6% of income.

Many business owners have told our team they don’t like contributing for employees who don’t save or who leave the company after a short stint. The conundrum is that failing to contribute to employees’ 401(k) accounts makes it more difficult for business owners to put away money for themselves and their key employees. That’s where safe-harbor 401(k) plans — something many small business owners are unfamiliar with — come in handy.

To make retirement plans simpler to administer and inclusive of highly compensated employees and owners, a business owner can select one of two options for safe-harbor contributions. One is the safe-harbor match within a 401 (k) plan. The other is the non-elective safe harbor that’s part of a profit-sharing contribution.

While safe-harbor 401(k) plans require employers to make contributions on behalf of employees, business owners and key employees also benefit without the company facing complex IRS rules. Regardless how much other workers in the plan save, the owner and all key employees can contribute the maximum deferral — $20,500 in 2022 plus a $6,500 catch-up contribution for those age 50 and older. Under safe-harbor rules, employers generally must match up to 3%, dollar for dollar, and 50% on the next 2% of compensation.

Plans without a safe-harbor provision face annual nondiscrimination testing. If a plan fails the test, it may have to refund the deferrals its highly compensated employees (those earning $135,000 or more) made during the prior year. That’s not likely to go over well.

The message advisors should be sharing with prospects is this: Small-business owners with profitable enterprises and zero to several employees benefit by implementing a 401(k) plan. Their tax advisors may have told them to set up a SIMPLE or SEP IRA instead because the costs are less. However, those retirement plans don’t offer the same planning options as 401(k)s do.

For example, most small-business owners don’t realize they can include a Roth 401(k) as part of their 401(k) retirement plans. All or part of the maximum annual contribution to a 401(k) plan can be directed into the Roth. That means a business owner and their spouse who also works for the company could each elect the maximum salary deferral to the Roth ($27,000 apiece in 2022 if they’re both 50 or older) . All distributions are tax-free. After both spouses die, their heirs will have ten years to take distributions on an inherited Roth IRA; these distributions are tax-free.

Profit-Sharing Plans

Profit-sharing plans are another way for business owners to reward employees with a percentage of their compensation. The name is a little confusing: Profit-sharing plans can even be set up in nonprofit organizations that don’t generate profits.

There are generally two different types of profit-sharing plans that are set up and in place today: traditional and new comparability. Most are traditional. The difference with new comparability plans is they allow employees to be divided into different groups that get varying employer contributions.

For example, with a new comparability plan, employers might award a greater contribution to a class of its workers who contribute disproportionately to their top-line revenues and bottom-line profits. This feature is usually for employees that make less than $135,000 per year. It’s possible for a company to establish such groups without violating IRS rules. With traditional plans, an employee usually gets profit-sharing awards based on their percentage of compensation to the total compensation the company pays its workers.

The profit-sharing safe-harbor non-elective, regulated by Section 1.401 (k)-3 (b)(1) of the Internal Revenue, requires employers to contribute to each non-highly compensated employee 3% of that employee’s compensation. The safe-harbor non-elective contribution works twice as hard for your client: It counts as a safe-harbor contribution and it also counts toward the required profit-sharing contribution requirements for a cash balance plan.

Many small companies fail to fund a profit-sharing plan. As their advisor, you can add real value by making sure they know about this opportunity by helping them create significant savings opportunities.

Cash-Balance Pension Plans

According to Ascensus, there are currently about 25,000 cash-balance pension plans. That’s rare compared with 401(k) plans, so it’s safe to say that many people aren’t familiar with them. Cash-balance plans are where the real goodies are for your business-owner clients.

A cash-balance plan, when integrated with a 401(k)/profit-sharing plan, allows the business owner to contribute significant amounts to their personal retirement savings. The Department of Labor has a helpful resource for more details around cash balance plans. . These integrated plans and the planning around them require the coordination of a team of professionals.

For example, to maximizing the business-owner contributions in a cash-balance pension plan, the company usually first needs to make a profit-sharing contribution of around 7%. A profit-sharing safe harbor non-elective 3% contribution counts toward the profit-sharing contribution of 7%. However, a third-party administrator (TPA) determines the exact amount, which usually varies between 4.5% to 8%. The cost to add a cash-balance plan is small compared with the amount that the business owner can fund for their own plan.

An advisor should focus on the net out-of-pocket cost for the employer of establishing integrated plans. Because the governments want employers to establish retirement plans, they offer tax and regulatory incentives every year that you should evaluate for each small-business client.

For some businesses owners, there can be significant benefits to implementing a cash-balance pension plan. In particular, some can make significant contributions that could exceed $250,000 per member, shareholder or partner.

The opportunities around retirement plans are enormous. Building on the concept of retirement plans as a cake, the communication around the cake concept is a simple and effective way to share with your clients what their options are.

Leonard C. Wright, CPA/PFS, CGMA, AIF, CFP, CLU, ChFC is the current chair of the Member Retirement Plan Committee at the Association of International Certified Professional Accountants (AICPA). His mission is to create clarity around the opportunities ERISA plans can provide to business owners, key employees and all plan participants who help them grow their businesses. He has clients across the U.S. His team’s mission statement is “Working together to achieve financial success through understanding, education, and action.”