Editor’s note: This is the author’s third article in asix-part seriesfor Rethinking65 on working with widows.

Laura Mattia

Having the opportunity to prepare, the first stage of widowhood can in some ways be a gift since you can assist your client in preparing both mentally and financially. Having the luxury of preparation reduces anxiety, although this doesn’t mean the grief is any easier.

But often, death is sudden, leaving no time for preparation. The end just happens and the widow finds her role, her relationships and maybe even her life purpose are changed overnight. The ending stage is the time immediately following the death, the days, weeks and months. This period can last even longer — a year or two.

Many believe it is this first year of widowhood that is the most difficult. A widow’s emotions are reeling and she is experiencing the cognitive disconnect associated with high-stress levels. Biologically her thinking brain, the neocortex, shuts down and she feels numb, “in a daze” and maybe even absentminded. The range of emotions can be endless and can include anger, guilt and anxiety.

Protect Her From Scammers and Greedy Relatives

If that was all and she took her thinking mind offline for a while, spending time focused on her grief, she probably would not get herself into trouble, but often that isn’t the case. When widows are in shock, and everything feels urgent, unscrupulous salespeople will often target her, encouraging her to make irrevocably adverse decisions.

Widows are often seen as easy prey by individuals who want to take advantage of their inheritance. While you don’t want to scare her, she must be aware of scam artists and unscrupulous debt collectors with fake documents and demands that require her to act immediately. Propose that you serve as her gatekeeper, screening all offers that may come her way before she makes a commitment or hasty decision.

Often in affluent families, adult children and potential suitors can be just as demanding, requesting funds for a new home or business venture. Advise her to tell all inquiring parties that she will consider their requests and immediately pass them to you. You can then explain to the family members that you will be preparing an analysis to ensure the widow has enough for her own needs now and in the future before making any gifts.

Identify Everything on Her Mind

You want to advise your client to postpone all significant decisions in the first year whenever possible. You can help her assess what requires immediate attention. Help her take care of filing for death benefit payments and determining which bills to prioritize while encouraging her to postpone other decisions until she has moved a little further through her grieving process.

It is essential to be aware that some widows may be in such shock that everything feels urgent. They could be feeling highly reactive and anxious. An excellent first exercise to work on together is to have her write down everything she thinks must be done, doing a brain dump of everything on her mind. Once this list is down on paper, she can begin to gain clarity. As she writes, you can help her co-create this list by discussing each task and listening to her concerns and fears associated with the undertakings. While often illogical, most widows feel financially insecure and fear becoming a bag lady. They want to know three things:

What resources do I have and where are they?

What do I need to pay for? What are my upcoming expenses?

Will I be OK?

Create a Roadmap

It may be tempting to develop a net worth and cash flow statement to answer these questions. I recommend postponing the application of sophisticated financial statements since it may feel overwhelming and stressful. Instead, help organize and rank what requires attention using a financial triage process. Focus on immediate needs by reviewing the list.

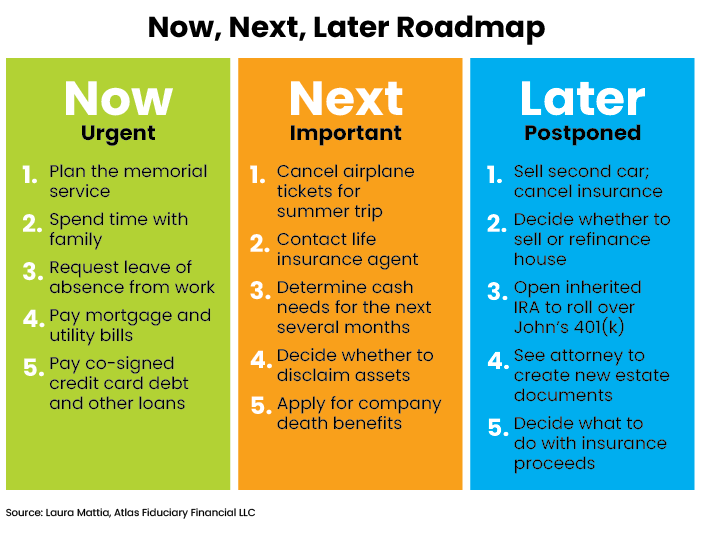

As you discuss the roster, help her recognize irrational fears and clarify what indeed requires her attention. A tool I learned to use years ago while working with the product development team in a large company is the Now, Next, Later Roadmap (see Figure 1). I like this tool because you can identify broad plans without committing to specific deadlines. The focus is on prioritization.

To create a roadmap, ask her to take a second sheet of paper and divide it into three columns. On the top, she should label each column: Now, Next, Later. Have the widow do the writing since this gives her the control, which will empower her. Help her categorize what is essential right now, such as planning the memorial service, spending time with the people she loves, making sure her employer is aware of what has happened and paying essential bills such as the mortgage.

Encourage her to put some of the items on her mind into the next column since these are important things that have a longer time horizon. Register those things with no pending time deadline under the later heading. Instruct her to keep this roadmap somewhere visible so she doesn’t have to contemplate all the tasks on her plate. It will help her stay focused on the critical things and put her mind at ease that there is nothing she is forgetting.

What About the House?

This exercise will help push out irrevocable decisions until a later date. Now is not the time to sell anything. Often, a widow may feel uncomfortable being alone in her house and compelled to sell her house, wanting to put that into the now column. This decision should be postponed and thoughtfully considered later when her rational thinking mind is back online (remember, at times of stress the neocortex, takes a holiday). There are many things to consider, including whether it is a solid real estate market and where she could move to maintain her support network and move on to her future life. A widow cannot envision her future life when she is grieving, so it is best to delay this decision.

She may be concerned about paying the loan on her home off in full. You can assure her that if she co-signed the mortgage with her spouse, federal law prohibits the lender from demanding the entire amount at his death. The mortgage terms will remain the same and she needs to continue making the monthly payments which is a now item. But before she sends the payment, she should contact the lender to inquire if an insurance policy covers the remaining balance. If not, and she is concerned about the monthly fee, you can discuss refinancing with lower interest or a more extended payoff period to make her cash flow more manageable, recording this task in the later column.

Listen to Fears and Regrets

As you listen to her fears, let her tell her story. She may want to talk about her husband and you may like to share your stories about him. In addition to fears, she may also express regrets — particularly around financial issues. You, as her advisor, should jot these regrets down. It is common for widows to have financial regrets but never share them with a financial professional. But when surveyed, they will express regrets such as:

I wish my spouse had life insurance.

We should have had a will, long-term care, disability, etc.

I wish we saved more.

I wish I knew more about our investments, the stock market, the bond market.

I wish I knew more about Social Security, Medicare, retirement choices.

I wish I knew more about how much debt we had.

Maryann was so angry with herself when she came to my office the first time. She couldn’t believe she had not been paying more attention to the family finances. Her husband had assured her they had adequate savings and never mentioned their debt balance. When I asked her about the household budget, she said there was no budget, it was not her fault the debt accumulated, and she was not going to pay it.

I explained to her that as a co-signer she was responsible even if she had no idea how or why the debt had accrued and her credit scores would be damaged if she did not pay. We put paying off the entire debt balance in her now column and I made a note to myself to work on a budgeting program with her in the future.

While it is not a good time to explore regrets now, you may want to address these items later when she moves into the growth stage of her transition. For now, your job is to give her room to grieve while keeping her grounded and ensuring nothing falls through the cracks. The Now, Next, Later Roadmap will help you both stay on task.

Laura Mattia Ph.D., MBA, CFP, is the CEO and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla.