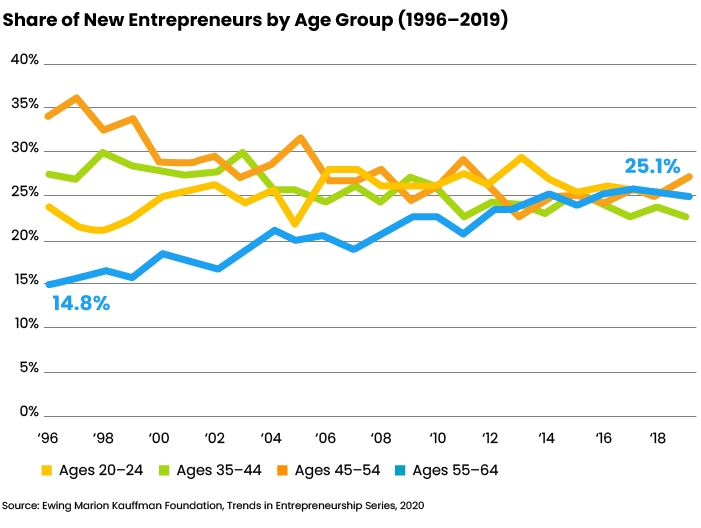

A growing number of adults age 50-plus are starting their own businesses. Americans age 55 to 64 represented just over 25% of entrepreneurs in 2019, up from about 15% in 1996, According to a study from the Ewing Marion Kauffman Foundation, this percentage tends to accelerate after recessions.

Some of these new entrepreneurs are dissatisfied with working in corporate America; some find themselves forced out of long-held careers; others want to turn a passion into a profession.

This growth in near-retiree business owners means chances are a client or two of yours will come up with a business idea. Our approach to these would-be entrepreneurs balances supportive counseling with the realities of financial management.

On the one hand, advisors are generally in a good position to evaluate different business models. We tend to work with clients from many different professions, and we analyze conditions at the company or general economic level when we make investments. On the other hand, considering the specific client, we may realize that the financial burdens of a new business will jeopardize his retirement planning.

“He decided that the way out of his predicament was to start a business — which set off alarm bells in my head.”

The “Interview Method”

One client of ours, Bob, was laid off in his 50s from a middle management job. With slender savings locked up in an IRA, he and his wife were forced to downsize, moving to a different town where living expenses were lower. While his wife was able to find a job right away, Bob could not. He decided that the way out of his predicament was to start a business — which set off alarm bells in my head. Capital resources simply were not available to support a business. I worried about his wife; she was very supportive of Bob but not prepared for the possibility that she would be left with nothing if this idea failed.

We elected to use what we call the ‘interview’ method, to ask Bob questions until he came to his own conclusion that this was not a perfect idea. We wanted him to feel like it was his stake in the ground. When people come to solutions that way, they are more likely not to deviate later on. Our questions ran along the lines of:

• How much do you think you need as start up capital? We reminded him about insurance, licenses, taxes, and services such as bookkeeping and accounting. Bob didn’t know what business he wanted to start yet, but he felt somewhere around $30,000 would be necessary — an amount that was 12% of the value of his IRA.

• Where are you thinking the money should come from? The only funding source Bob had was his IRA but we wanted to hear him say that. We pointed out that drawing IRA money would incur an income and excise tax burden — so instead of taking $30,000, he would need something closer to $45,000 to net $30,000.

• How much do you think you can make, and by when? And what’s the plan for restoring your retirement funds?

This last question was where our Q&A halted, because Bob began to see that this half formed idea was far too risky.

In the end, Bob decided to start a capital-less business doing odd jobs and deliveries. This suited his outgoing personality and saved his IRA, which now supports the couple in retirement ten years later.

Collaboration

Contrast Bob’s situation with a client we will call Joan. She is in her 40s, married with a child. Joan is planning to start an event business with a friend from college. Her prior career was in public relations, and her partner was in marketing.

Joan inherited around $1 million in two accounts, about evenly split between an IRA and a taxable account. Withdrawals have been restrained over the years and the couple recently sold their house — netting another several hundred thousand dollars — in order to rent while they decide where to live in the post-pandemic world.

Joan specifically asked for advice. Our discussion covered many topics including: Was the business a good idea; what kinds of things should they think about that didn’t involve actually putting on events (licenses, taxes, rented equipment, the contract with her partner, the lease for the space, technology, photographers); what about a space with an apartment so eventgoers could remain on premises; how would they market for both weekday and weekend events and to whom; and how far she was willing to commute to find a reasonably priced space.

Unlike Bob, Joan has drawn a boundary around the financial commitment. She and her partner will each put in $50,000 over time to get the business up and running, and if they haven’t started making money after running through that amount, they will pull the plug.

We could unreservedly support Joan’s idea. The business uses skills both partners have; their homework was impeccable and included interviewing competitors, and a business plan; the financial commitment is reasonable; and the family is light on other financial obligations at the moment.

Our conversation with Joan amounted to collaborating with her, whereas our conversation with Bob was meant to lead him to a conclusion that he could own, to protect his and his wife’s financial future. Tuning up to those differences can help advisors craft the right response to clients who want to take the leap to entrepreneurship.

Michelle Rand is founder and CEO of Cascade Investment Advisors, Inc., located in Oregon City, Oregon. The firm is a service-first, investment management firm.