Your opportunities as a financial advisor are infinite, but your time is finite. How will you invest your time in your practice in the years ahead and how will your organization change in the next five to 10 years?

Currently, the ideal workload for mature advisory businesses is based on six basic functions, listed below with approximate percentage of time spent on each.

But this is based on a limited number of hours in a day or week, not on evolving client needs. Here are my prognostications for the direction many of your organizations will take within the relatively near future to stay competitive and serve clients well.

Investment Management

Investment management is what consumers think about first when it comes to their financial well-being. Yet with all their other responsibilities of running a practice, many advisors aren’t able to give enough attention to this function. I’m not saying that they should personally be spending more than four to six hours of their week doing investment (portfolio) management — some already spend much more. But I do think we’re going to see a bigger move toward outsourcing investment management.

Perhaps as many as 75% of financial advisors will outsource this function to full-time investment analysts/specialists, many of whom offer turn-key asset management programs (TAMPs). I also expect that almost all advisors, whether or not they outsource the investment management piece, will embrace more investment models.

Portfolios in general will opt more toward low-cost ETFs and tax-efficient investments, removing even more of any value-add of an already highly commoditized service. Despite the industry’s trend toward commoditization of investment management, it still remains a high-value offering. That’s because many individual investors think it’s not worth their time, effort and cost to learn to about and make investment decisions for themselves. Full-time investment professionals can do this work, for hundreds or thousands of unstudied investors, much more effectively and efficiently.

Many advisors are already having a hard time differentiating themselves on the investment management offering. Outsourcing this function will give them more time to differentiate themselves in other ways with clients.

Business Development

Business development is the most interesting aspect of financial advisory businesses. There are at least 22 possible approaches to business development, including introductions from clients and centers of influence, niche marketing and networking. While all approaches can produce positive results, a smaller number will work for most individuals effectively and efficiently.

For today’s mature financial-advisory practices, business development at best gets 20% of an advisor’s time and most firms claim they don’t have enough time. Firms often try a couple of approaches. In the future, multi-advisor practices will more proactively focus on four or five approaches, measure their effectiveness and efficiency, and change approaches every year or two if they are not working. Introductions from clients, COIs and others; niche marketing; networking and various types of events will account for more than 90% of business-development efforts.

For some firms, business development will morph into a full-time job — or two. Client relationship managers (RMs) will focus on client servicing but will also work with the business development executive (BDE) who generated the relationship. The BDEs will be magnetic, competent advisors with the skills of the RMs and strong sales capabilities, too. The BDE will continue the relationship with the client by participating in regularly scheduled client meetings with the RM. Here’s a closer look at the role and potential compensation for both positions. Different compensation plans will evolve – a combination of salary and incentive plus bonus.

Business development executives

The BDE will be able to participate with 300 to 400 clients, which will take about 25% of their time. They will get 15-minute updates from the client relationship managers and participate in the annual review meeting and, during the year, a couple of short touch-base calls with the client.

BDEs could receive 50% of their total projected base income as salary and the other 50% if they meet their goals based on client retention, satisfaction, asset growth and introductions. If they exceed their goals, they would be eligible for bonuses to be determined. For example, they might be eligible for a 100% bonus over their projected base income.

Client relationship managers

Client relationship managers will work with clients almost 100% of their time but will also have business development responsibilities, such as acquiring introductions. RMs will ideally be certified as CFPs, or CPWAs and hold appropriate retirement counselor certifications or equivalents.

Using tools and metrics will help RMs add value. For example, firms should have client service models that define client deliverables and a services calendar that shows and describes these deliverables. During regular discussions with clients, RMs should go over the service models and service calendars. This should give them the opportunity to identify the services the client values and does not value. If there are too many deliverables not seen as of value, one should question the deliverables and/or the client fit. To determine fit, deliverables will have been discussed in the initial discovery process.

As for compensation, client relationship managers could receive 75% of their total projected base income as salary and the other 25% if they meet their goals based on client retention, satisfaction, asset growth and introductions. If they exceed their goals, they would be eligible for bonuses to be determined.

Leadership

Larger firms may separate strategic and tactical management into separate functions — a CEO and a COO (chief operating officer). Firms that use an entrepreneurial operating system (EOS) define these roles as follows:

CEO: The idea person. The CEO develops the vision, provides creative solutions and solves problems. The CEO also manages and grows relationships (including firm acquisitions), ensures a consistent and desired culture, and manages research and development.

COO: The Integrator. The COO is the lead manager responsible for the numbers (such as profit and loss) and this year’s business plan. They also beat down the bigger day-to-day issues that are barriers to effectiveness and efficiency, are responsible for day-to-day-management, and manage special projects.

The CEO, COO and their teams will step up their strategic focus to meet the needs of their firms and their clients. Smaller firms struggling to compete will be gobbled up by consolidators and the current trend of consolidation will continue and increase over time.

Organization

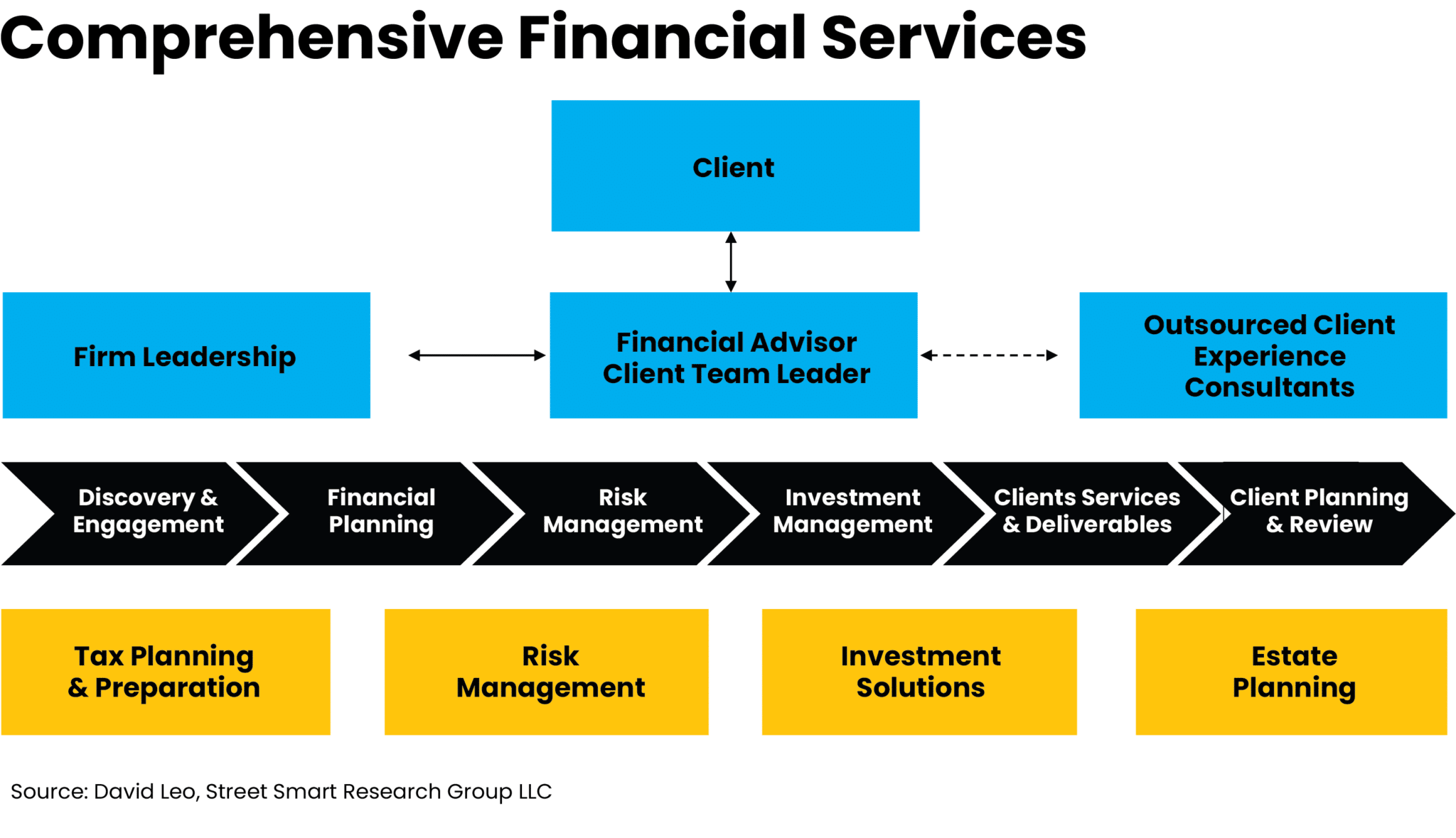

Firms will evolve to look more like the following:

Viable firms in the business for the long haul must be financial-planning based and perform the functions shown. Depending on a firm’s size and philosophy, they may choose to either directly provide or outsource the functions above shown in yellow: tax planning and preparation, risk management, investment solutions and estate planning.

Smaller firms that can’t afford full time professionals like a tax attorney could use a strategic partner outside the firm, which would enable them to provide the service without incurring the full cost. One disadvantage of outsourcing is that those professionals are outside your scope of control or management. Advisors will need to weigh the costs and benefits of such arrangements.

More 2035 Developments

We will see nominal increases in professional development as jobs and client needs grow and get more complex. These will include more online learning, which, if done correctly, can be more efficient and effective than onsite learning — even if it’s not as fulfilling. Administrative work will continue to become more automated and outsourced and will be affected positively by AI.

Client experience consultants and coaches will also become more common for advisory firms. These consultants and coaches, will work closely with the firms’ client relationship managers and business development executives to help structure and improve and grow their results. Consultants and coaches may also take on the roles of measuring client satisfaction and training advisory firms’ new and/or novice client relationship managers and business development executives.

Firms will also step up their marketing (including social media) and technology efforts but may choose to outsource these functions as it may be more cost effective. For many advisory firms, there is no competitive advantage to providing these functions in house.

In Summary

Advisory firms must evolve over the next decade to survive as competition remains challenging. Firms will get larger and more complex. In many areas of the business, outsourcing will grow at a faster rate than in the past. Firms will differentiate themselves more through the quality of their teams, services and leadership. Finally, growth will come from quality, consistency and follow through — not silver bullets.

Some questions you must ask yourself include:

Does your vision go beyond more of the same to more different?

What functions should you focus on internally and what should you outsource, i.e., where is your potential competitive advantage?

What does your team look like now and how will it change?

What characteristics do you see in your future hires?

What industry trends will dictate new roles, and will you lead or follow?

Do your growth projections address your new structures and costs?

As industry consolidation continues, will you be an absorber — a big firm buying a smaller firm — or an “absorbee”?

David Leo is the founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant and trainer to financial professionals. David is an experienced business manager who works solely with financial advisors, planners and firms who want to organize, structure and grow their businesses by attracting, servicing and retaining affluent clients. He can be reached at David@CoachDavidLeo.com, 212-598-4229 (office) or 917-379-1249 (cell).

Viable firms in the business for the long haul must be financial-planning based and perform the functions shown. Depending on a firm’s size and philosophy, they may choose to either directly provide or outsource the functions above shown in yellow: tax planning and preparation, risk management, investment solutions and estate planning.

Viable firms in the business for the long haul must be financial-planning based and perform the functions shown. Depending on a firm’s size and philosophy, they may choose to either directly provide or outsource the functions above shown in yellow: tax planning and preparation, risk management, investment solutions and estate planning.