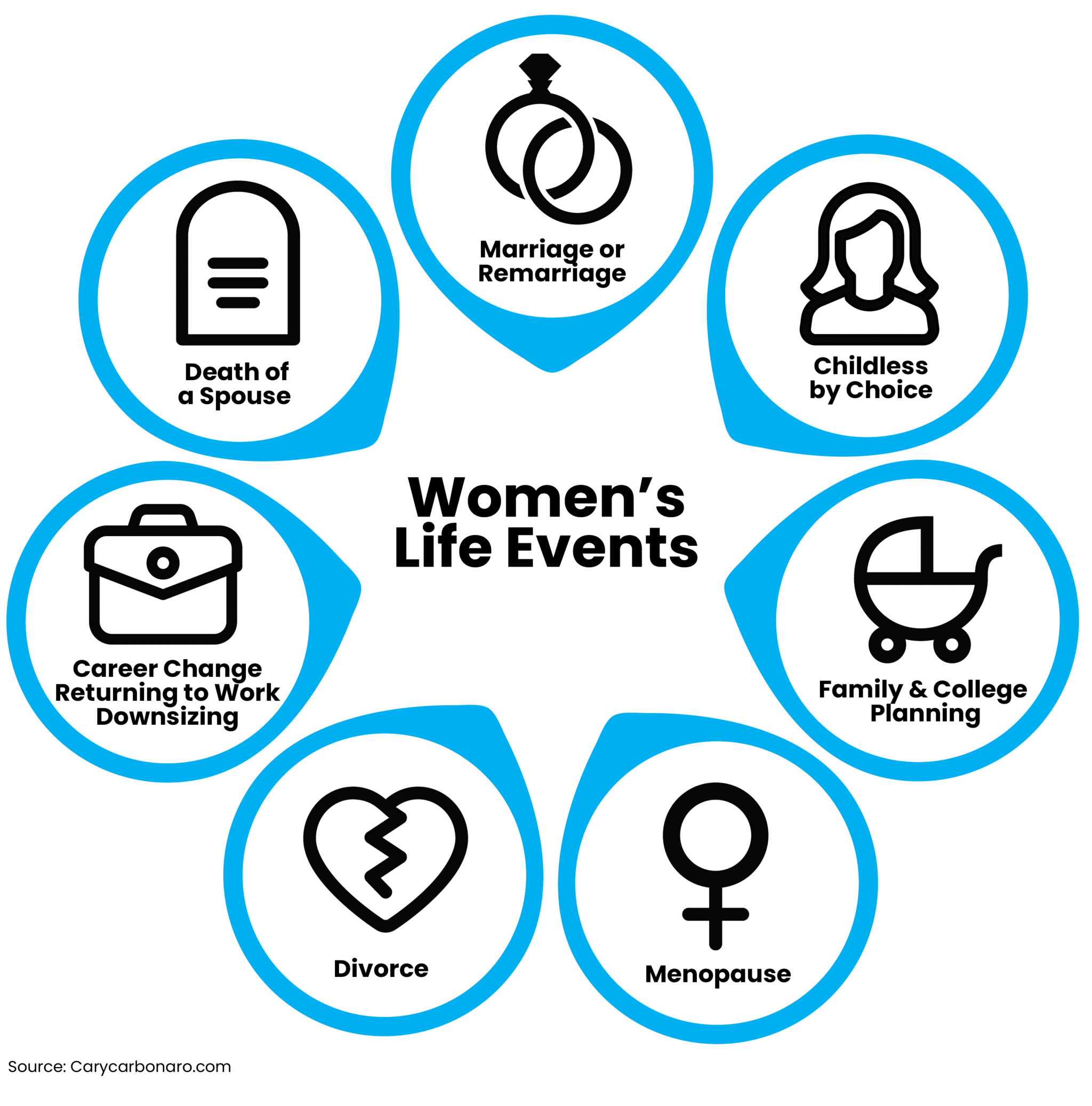

Wealth management for women has traditionally focused on widows first, divorcees second and pretty much nothing else. It is as if all women fall into these two boxes. Sorry, wealth management industry: Women are much more than those two life events. When I look at women’s life cycles, I come up with seven distinct ones.

Yes, of course, we have the first two: death of a spouse/widowhood and divorce/separation. But advisors should give more thought to all seven of these life events — the others which we’ll get to shortly — to help their female clients and strengthen their client relationships. Most of these life events are triggers to review financial plans and beneficiaries, and advisors should encourage clients to inform them should these events arise.

Here’s a look at the seven cycles.

Death of a Spouse/Widowhood

As many as 70% of female clients leave their financial advisors soon after their husbands die. I am usually on the receiving end of this, and I wrote about this client segment last year.

When women lose their life partner, every decision can seem impossible to make alone. It is a great time to work with an advocate who can help them work on the big life and financial decisions while they are dealing with grief. Everyone grieves differently. This is a time for an empathetic financial advisor to shine.

Widows have so many decisions to make, including “What do I want the rest of my life to look like without my spouse?” and “Am I staying in the house and can I afford to?

If you already have a strong relationship with your widowed client, be sure to be there for her. Whenever a client’s spouse dies, I attend the funeral service. One of my clients wanted me sit next to her; I held her hand the entire time because she was crying. I also get many clients right after their spouses dies. Establishing a relationship in the middle of her grief is even more difficult, but the key again is giving them what they need.

Divorce/Separation

This is another emotionally charged time in a women’s life. Sometimes this is worse than the death of a spouse. It is a time where they are literally burning the house down and starting over. It is scary but it is another time in their life when you can shepherd them through it and you can shine.

I get involved early on when their marriage is coming apart and sometimes it takes years before a divorce is final. I am involved in the mediations and negotiations, and I am a friend and a voice of reason the entire time. For me, the best part is that I can share my personal experiences because I went through a four-year divorce that costs hundreds of thousands of dollars. I always say that since I got through it, you can too — and that it is so beautiful on the other side. I am an open book; I don’t hold anything back.

Most of my divorced clients come to me while the divorce proceedings are in process so I don’t know the spouse. One of my client couples has been in the process of divorcing for two years and I’m still working with both spouses. In such cases, it’s critical to communicate with and remain a fiduciary to both spouses.

Career Change/Returning to Work

Our careers are important to us. Losing a job not by choice is a life-altering event. I’ve seen this with my clients over and over. Even when it is their choice, it still is a life change that needs help and guidance to be navigated. I’ve also worked with clients who want to obtain “returnships” to help them re-enter the workforce after a long gap. You can google which companies offer them.

One of my clients participated in the JPMorgan Chase returnship; my connections helped her land a spot. She was in her 40s at the time and wanted to get back into finance after leaving the workforce to raise her children. The program provided her with lots of training. Returnships can be similar to the management training programs designed for new college graduates — lots of classroom and group learning.

Menopause

Menopause is a huge life change when you are in it, and you are in it for the rest of your life. It has physical, mental and financial consequences. Menopause is a good time to review retirement plans, healthcare costs and mental health support with your clients. Every woman’s experience is unique. It is a time for reflection. I also wrote an article on this last year.

Talk to each woman in this stage of life about her expected retirement age, her retirement savings and her expected Social Security benefits. Evaluate her healthcare costs: Menopause can change a woman’s healthcare needs because it’s often a time when new medical conditions develop. Factors to help her consider are her health insurance coverage, her potential medical expenses, and her long-term care needs.

Marriage or Remarriage

Getting married or remarried is a huge life event for clients. They are not only merging their lives, they are merging their money. They need a financial planner to make sure they are aligned with their new partner. Do they have the same goals? Is one a saver and one a spender? Have they gotten financially naked? This means being honest and sharing info such as net worth (including all assets and liabilities). If either partner has credit card debt or student loans, the other one needs to know this.

Money is one of the top reasons for divorce, so getting on the same page is a great first step in a new marriage. Most couples need an expert to help navigate this. I’ve had conversations with clients about prenuptial agreements and have recommended attorneys. When a client has significantly more wealth than their spouse-to-be or new spouse, I strongly recommend prenups.

Childless by Choice

Yes, this is a thing and an entire category of women. A woman without a child does not need to do any additional financial or estate planning than women with children. She has to decide who her beneficiaries are, and she needs to have a will, a health care proxy and a power of attorney. She can also decide if she needs a trust.

Some people say that women who are childless by choice have to worry about not having a child take care of them as they age. That’s not true: We often have more money to pay for top-notch care, from often spending more time in the workforce and not incurring the expense of raising and supporting children, and there are many choices for care. And the reality is, children don’t always help their parents.

It is also important not to be judgmental of women who are childless by choice. Many people think a woman who choses this life hates children and that is often absolutely untrue. I identify closely with this group because I am part of it. I never felt less than or not fulfilled because I got so much satisfaction from my career. I was also married to “Mr. Wrong” during my childbearing years. Here’s an NPR interview I did on this subject.

And never ask a woman if they regret their life choices. In the Netflix show, “House of Cards,” Claire Underwood is asked, “Do you ever regret not having kids?” She replies, “Do you ever regret having them?”

Family and College Planning

I’ve worked with many clients who have said to me that they wanted to plan for having a baby. Some questions to consider: Will they or their spouse stay home or will they get a nanny? Will they take a sabbatical from work? Will they want to fund college? How much life insurance will they need now that they are responsible for a human life? These are also huge financial decisions that you as their advisor can help them think through.

The cost of raising a child or children can be huge, especially if they attend private school from kindergarten through high school. The cost of nannies and summer camp can also add up. The average cost of summer camp is $178 a day for day camp and $448 a day for sleepaway camp, according to the American Camp Association.

I worked with a couple where the dad stayed home for three years. After crunching the numbers, I told him he had to go back to work after that, but he never did. His working wife grew resentful and they eventually divorced. To date, I’ve never worked with a single woman who wanted a child but this would also require a lot of planning.

Empowering Women

In recognizing and addressing the diverse life cycles of women, the wealth management industry has the opportunity to break free from traditional stereotypes. By providing tailored and empathetic financial guidance throughout these distinct phases, financial advisors can empower women to navigate their unique journeys successfully. Embracing the richness of women’s financial experiences goes beyond widows and divorcees. We can and should create a more inclusive and supportive wealth management landscape for all women.

Cary Carbonaro, CFP, MBA, is SVP, director of Women & Wealth at ACM Wealth, the wealth planning team of Advisors Capital Management. She was appointed and has served as a CFP Board ambassador since 2014. Cary is the author of “The Money Queen’s Guide: For Women Who Want Build Wealth and Banish Fear.” She has spoken all over the world about financial literacy for women. You can reach her at cary.carbonaro@advisorscenter.com.