“How should we celebrate our 20th anniversary, Honey? How about a Caribbean cruise?” My husband was excited about his plan. But that celebration never happened. No big party either. Instead, I became a member of the group no one wants to join — the “widows club.”

More than 76% of the 15 million widowed persons in the United States are women, according to the U.S. Census Bureau. That number is growing annually. Financial professionals may be especially interested in these staggering statistics:

Approximately 70% of married women will experience widowhood

80% of men die married, while 80% of women pass away single

The average age a wife becomes a widow is 59, leaving her to navigate financial decisions independently for years or even decades

70% of widows part ways with financial advisors they used as a couple, moving their assets and the assets they inherited from their deceased spouse.

Advisors who want to support and retain widowed clients should be aware of how to communicate as well as understand her changing tax status (more on that later). Below are some suggested communication techniques — these are approaches that I have used:

Ask Questions and Listen

Initiate conversations by asking about her story and listening actively. Understand her emotional journey without immediately prescribing financial solutions. Encourage her to reminisce about her late spouse, acknowledging the significance of those memories in her healing process.

Example: “Mrs. Jones, unfortunately, I didn’t have the opportunity of knowing your husband before his death. How do you hope others remember him?”

Avoid jumping to make major irrevocable financial decisions during the initial grief stage. Help organize her financial information, guide her through immediate tasks, and defer investment decisions until a strategic plan aligns with her future.

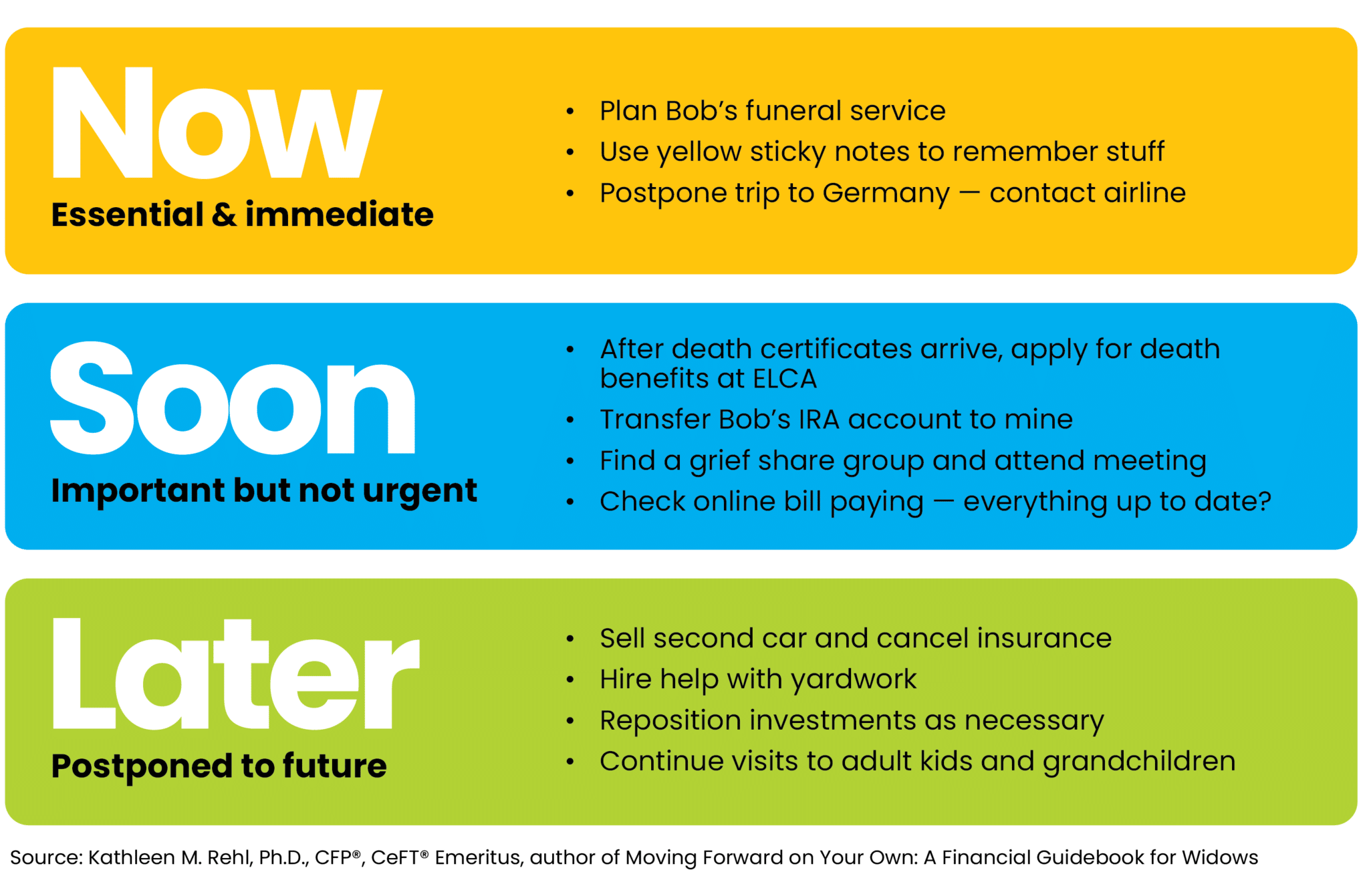

Example: “You’ve shared your concerns about what needs to be done, and you don’t have to do everything at once. Rather, let’s organize things into NOW, SOON, and LATER groups.” Then divide a page into three sections. Invite the widow to write the items you two discuss in the appropriate sections. She will remember these better if she writes rather than you. This page is her takeaway until you meet the next time, when you’ll help update what she’s done and prepare a new NOW, SOON, LATER page.

Help Widows Feel Safe and Secure

Spoken or not, many widows are thinking, “Am I going to be okay financially?” Even a millionaire widow may fear becoming a bag lady. Instead of focusing on market performance, prioritize her peace of mind. She’ll feel more confident knowing you have processes and tools to assist. Focus on the personal side rather than the technical side of money.

Example: “Over the years that we’ve worked together before Bob died, you two built a strong foundation that’s still in place today, even though he’s gone. You don’t need to make any immediate changes now. Everything is safe where it is. When the time is right, we’ll revisit your financial plans to make adjustments that fit your new life going forward.”

Engage in Mindful Communication

Steer clear of clichés and insensitivity. Engage with empathy, acknowledging her pain. Handwritten notes of encouragement and ongoing thoughtful gestures matter, such as suggesting a grief support group that may be appropriate for your widowed client.

Example: Don’t offer platitudes like “I’m so sorry for your loss,” or “He’s in a better place now.” Rather say, “I can’t imagine the pain you’re experiencing. Please know I’m here to support you on this new journey.”

Simplify Financial Discussions as her Partner and Guide

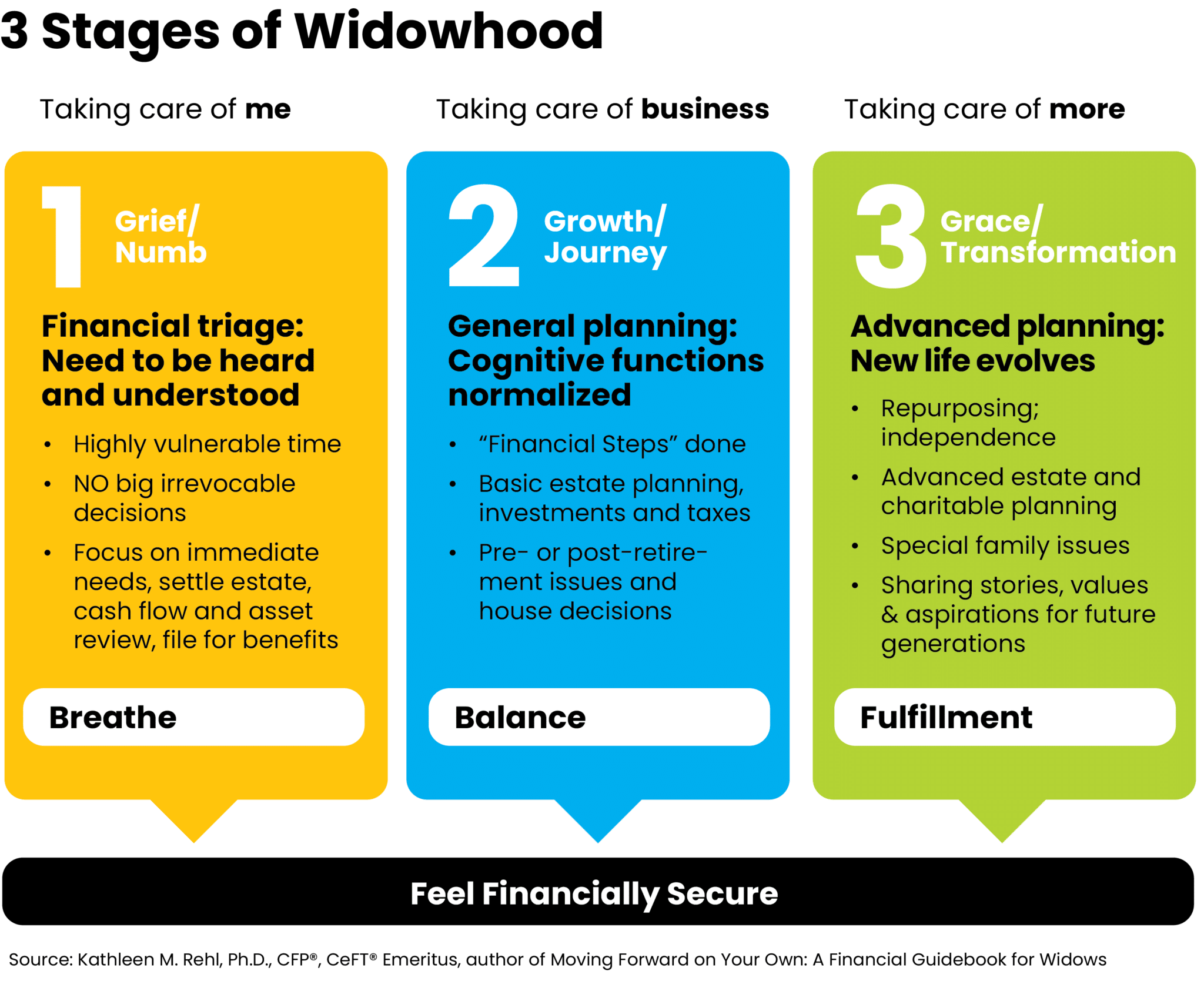

Use plain language and summaries during meetings. One-page overviews can work well, especially during a widow’s early stages of grief when she may say she’s experiencing “Jello brain.” Recognize potential challenges with attention and memory and provide concise action steps. Engage her in decision-making by offering options and guiding her through possible strategies.

Example: The chart below is a one-page overview of the 3 stages of widowhood that I use with widows. After explaining each stage, I would ask, “What stage would you say you’re at now, looking at this overview?” Then, a rich dialog generally follows as she speaks about her path. (You can learn more about these three stages here.)

Tax Considerations for Widows

Federal Income Tax

As a result of changing her tax filing status from married filing jointly to single, surviving spouses may be surprised to see a significant spike in their federal income tax and Medicare premiums. Likewise, net investment income tax may apply when she must change her filing status.

A widow is considered married for the whole year her spouse died and can file a joint tax return. The standard deduction for married couples in 2024 is $29,200, plus an additional amount for those over 65. But the next year she must file as a single person, with a greatly reduced standard deduction of $14,600.

For example, a married couple with a taxable income of $90,000 would pay at the marginal tax rate of 12%. Even if her taxable income falls to $70,000 after her husband dies, a widow is pushed into the 22% tax bracket. Ouch! Income tax brackets are narrower for singles than for married folks. (Even if a widow qualifies as “head of household” the year after her spouse’s death, her tax bracket is not as wide as when she was married.)

Tax on Social Security

A widow’s Social Security benefits may be more taxable than when she was married. If her combined adjusted gross income as a single person exceeds $25,000, up to 85% of her Social Security benefits may be subject to federal income tax paid at ordinary tax rates. Conversely, Social Security benefits are not taxed for married couples with less than $32,000 of combined income.

IRMAA

In 2024, the standard Medicare Part B monthly premium is $174.70. Married-filing-jointly Medicare recipients with 2022 incomes above $206,000 pay a surcharge known as an income-related monthly adjustment amount (IRMAA). That increases the Medicare premium for each spouse to between $244.60 and $594.00. However, a widow filing as single is hit with this surcharge when her income exceeds only $103,000. If her income pushes past that limit by just $1, she jumps to the next level, paying an extra $69.90 a month for Medicare Part B IRMAA. Her surcharge continues to increase with income, rising to a combined premium and surcharge of $594 per month when her income tops $500,000. Conversely, those filing as married don’t reach this summit until their income exceeds $750,000.

Sale of Primary Residence

Widows who sell their main residence in less than two years after the death of their spouse can exclude up to $500,000 of long-term capital gain. After that, the capital gain exclusion drops to $250,000. Remember that at least half of the property’s basis will be stepped up to its value on the spouse’s date of death. This will often result in no capital gain on the home’s sale.

Military Death Benefit

When a servicemember dies, a surviving widow may receive $400,000 from Servicemembers’ Group Life Insurance (SGLI), plus an additional $100,000 for a combat-related fatality. The widow can roll all or part of the death benefit payout directly into a Roth IRA, as part of the Heroes Earning Assistance and Relief Tax Act of 2008 (HEART Act). The original principal in the account will grow tax-free, although Roth earnings can’t be withdrawn without penalty before age 59½. This is a great way to save for retirement or children’s college education. Likewise, it can reduce net investment income tax, if applicable.

Tax-Efficient Charitable Giving

For charitably inclined widows age 70½ and older, consider these two options:

Qualified charitable distribution. In 2024, widows over age 70½ can make charitable contributions from their individual retirement account (IRA) of up to $105,000 without recognizing this amount as taxable income. Identified as a qualified charitable distribution (QCD), this gifting strategy reduces her adjusted gross income, lowering her federal income tax. This action may also decrease her Medicare surcharge and net investment income tax.

One-time “Legacy IRA” rollover. Making this rollover for a charitable gift annuity will pay lifetime income to the donor and provide a QCD. For example, in 2023, I used this strategy when I contributed $50,000 from my traditional IRA. I now receive 6.8% income from my gift annuity. I saved $12,000 in federal income tax and reduced my IRMAA Medicare premium surcharge. At my death, the remaining principal will benefit three nonprofits that I support, including an international widows organization. You can read the details here. (Note: This win-win strategy isn’t just for widows; it works for everyone, no matter their marital status.)

Advisors who assist widows in transition know this isn’t just a niche — it’s an opportunity to build lasting trust and relationships. By demonstrating empathy, providing holistic support and integrating specialized planning into their financial strategies, advisors can secure lifelong clients while making a meaningful difference in these women’s lives.

Kathleen M. Rehl, PhD, CFP®, CeFT® Emeritus wrote the award-winning book “Moving Forward on Your Own: A Financial Guidebook for Widows.” She owned Rehl Financial Advisors for 18 years before an encore career empowering widows. Now “reFired,” Rehl writes legacy stories and assists nonprofits. Her work has appeared in the New York Times, Wall Street Journal, Kiplinger’s, CNBC and more. She’s an adjunct at The American College of Financial Services. Her website is https://www.kathleenrehl.com.

Help Widows Feel Safe and Secure

Help Widows Feel Safe and Secure