The “experience economy” has become a very popular term although Starbucks, Ritz-Carlton, BMW and Disney have been selling experiences rather than products and services, for decades. So did many organizations before that (Anyone else remember Pan Am?). But the business world is now abuzz about experiences. The financial services industry is even starting to look at the client-review meeting as an experience, instead of as a service.

This may include sending a limo to pick up UHNW clients, meeting and greeting them in the parking lot, introducing them to your well-tailored team, serving them specially brewed coffees and their favorite treats, etc. I realize I could be overstating the experiential aspects of most meetings, but somehow many meetings are being upgraded.

In a previous article, “A Smarter Way to ‘Wow’ Clients,” I addressed some meaningful and high-value experiences that advisors can deliver. In this article, I want to call to your attention two books I recently read that focus on delivering experiences to clients, which I think advisors can learn a lot from:

“The Experience Economy: Work is Theatre & Every Business a Stage” by B. Joseph Pine II and James H. Gilmore.

“Serious Shift: How Experience Staging Can Save Your Practice” by Dennis Mosley-Williams.

‘The Experience Economy’

As “The Experience Economy” puts it, “There are props, there are scripts, there is presentation and delivery, there is a stage and scenery upon it. Some of you may be thinking that this all sounds incredibly artificial and disingenuous. It is anything but.”

Instead, “Staging and scripting an experience are simply the means by which it becomes predictable, anticipated, expertly executed and totally engaging for your clients,” the book continues. “And like the actor who knows his lines, you will become totally prepared and comfortable with what you have to say.”

It’s not yet clear to me that this statement will be true, at least for every financial advisor. That’s because as “The Experience Economy” also notes, “If not staged authentically, experiences, by virtue of being constructed or staged, can be subject to consumer suspicion that the experiences are contrived or lacking in sincerity.”

To me, this seems to require human beings to virtually “shape shift” to be something other than who we are. For example, am I writing this article for personal recognition or solely to give you thoughts to reach your own conclusions about delivering experiences to clients? Maybe it’s both, or maybe I am a pure altruist. (The latter would be unlikely.) We live with who we are, and perhaps not everyone is authentic or a skilled actor.

Conversations matter most

“The Experience Economy” is a more academic book than “Serious Shift.” By academic, I mean that it takes a very studied and scholarly approach. About 30 years ago, I met with Joe Pine, co-author of “The Experience Economy,” and I have tremendous respect for him, his work and his experience.

I agree with Pine that it’s not the scripts that matter most, but rather the preparation that goes into delivering predictable and well-executed meetings that engage clients. Ultimately, this means you have conversations, not presentations, because your goal should be for clients to talk a lot and for you to listen a lot; people tend to like you better when they talk and you listen!

“Perhaps the biggest value in ‘The Experience Economy’ is that it says companies need to be more experience driven in order to be memorable and therefore differentiable.”

Perhaps the biggest value in “The Experience Economy” is that it says companies need to be more experience driven in order to be memorable and therefore differentiable.

For me, the preview tells the story of this book: “Time is the key characteristic that distinguishes experiences from services. Services are delivered on demand while experiences are revealed over a duration of time. It’s designing what happens to people in time, in a place. So, it is for every experience. You must design the time your customers spend with you.”

“Think of it this way: services are all about time well saved, while experiences are about time well spent. Customers spend their hard-earned money and their hard-earned time on more valued experiences.”

The authors state, “To capture customers’ attention, you must stage experiences worthy of attention” and “Experiences that are robust, cohesive, personal, dramatic, and even transformative.” As I see it, if you make experience robust, personal, dramatic, and transformative, you can make experiences magical.

“The Experience Economy” also discusses and descries four realms of experiential value: entertainment, educational, escapist and aesthetic. In the financial services industry, we may focus more heavily on educational experiences, clients’ concerns and even their dreams, and how to deliver them. That could move us to the aesthetic potentially, or as the authors described, “sitting at the Caffe Florian in Old World Venice.” You should be able to help the client feel that picture of a place that’s special to them. For me, that go-to place is dinner in Room 21 in Monopoli, Italy.

“The Experience Economy” is rich with knowledge, including how to create the next phase of client delivery. The book also brings up this important point: Planning client experiences takes time and you must remain efficient. After all, your workday and work week are a constant and must be managed.

‘Serious Shift’

“Serious Shift” is the more pragmatic of the two books and reminds me of the coaching work that many of us in the financial services industry currently deliver. It provides a formal structure and reminders, much like a checklist, that can be useful to advisors and clients. It’s not a long book (175 pages plus notes).

The author, Dennis Moseley-Williams, shares his values:

“I want to help those people who wish to bring a soul to their enterprise, who believe that their success comes not only from the sound professional advice and services they provide their clients, but also from the experience they create or ‘stage.’”

“Successful people are successful, first and foremost, because they intend to be a great person and do great things. Let me repeat that: The primary intention of most successful people is to help others, not to enrich themselves.”

“The desire to be great must come before the desire to be rewarded.”

Some of the areas Moseley-Williiams addresses are basic reminders of practice management. For example:

Knowing your ideal client and their needs.

Thinking about clients as people, not portfolios.

Clarifying appropriate benchmarks vs. the Dow.

Making personal connections, knowing and understanding the client.

Segmenting time and clients, including not allowing interruptions during the day.

Doing what you do best and delegating the rest.

Recording all information, and make sure that the members of your team reference these facts in future conversations (things we know and forget to tell staff to do).

Greeting your clients when they arrive for meetings and always having printed agendas.

Holding efficient and effective weekly team meetings.

Many of these basic reminders are important to all financial advisors, whether they are novices or more experienced. This is what I mean by pragmatic. (If you would like a free copy of my summary of the book, just email me.

Moseley-Williams also provides some very good scripts that I think many financial advisors are likely to appreciate. For example, he says, “…this is exactly what I want from my advisor. I want to focus all my energy at being profitable when I am working so that I can take time off and be truly unplugged and engaged with my family when I am not. I want someone to give me a plan, update me on it, keep me informed about what’s going on, and tell me what to do about it. I want to accept their word as gospel and quickly get back to doing what I know I need to be doing, which isn’t worrying about my financial planning.”

If this is what you deliver, or want to deliver, this is an excellent way to explain to your clients what you may do for them in terms they will understand. Borrowing Moseley-Williams words, it could sound something like this: “If you want an advisor who will allow you to focus all your energy … be unplugged and engaged … give you a plan and update it … keep you informed … so you don’t have to worry about your financial planning, then we should work together.” You could even post this type of message on your website.

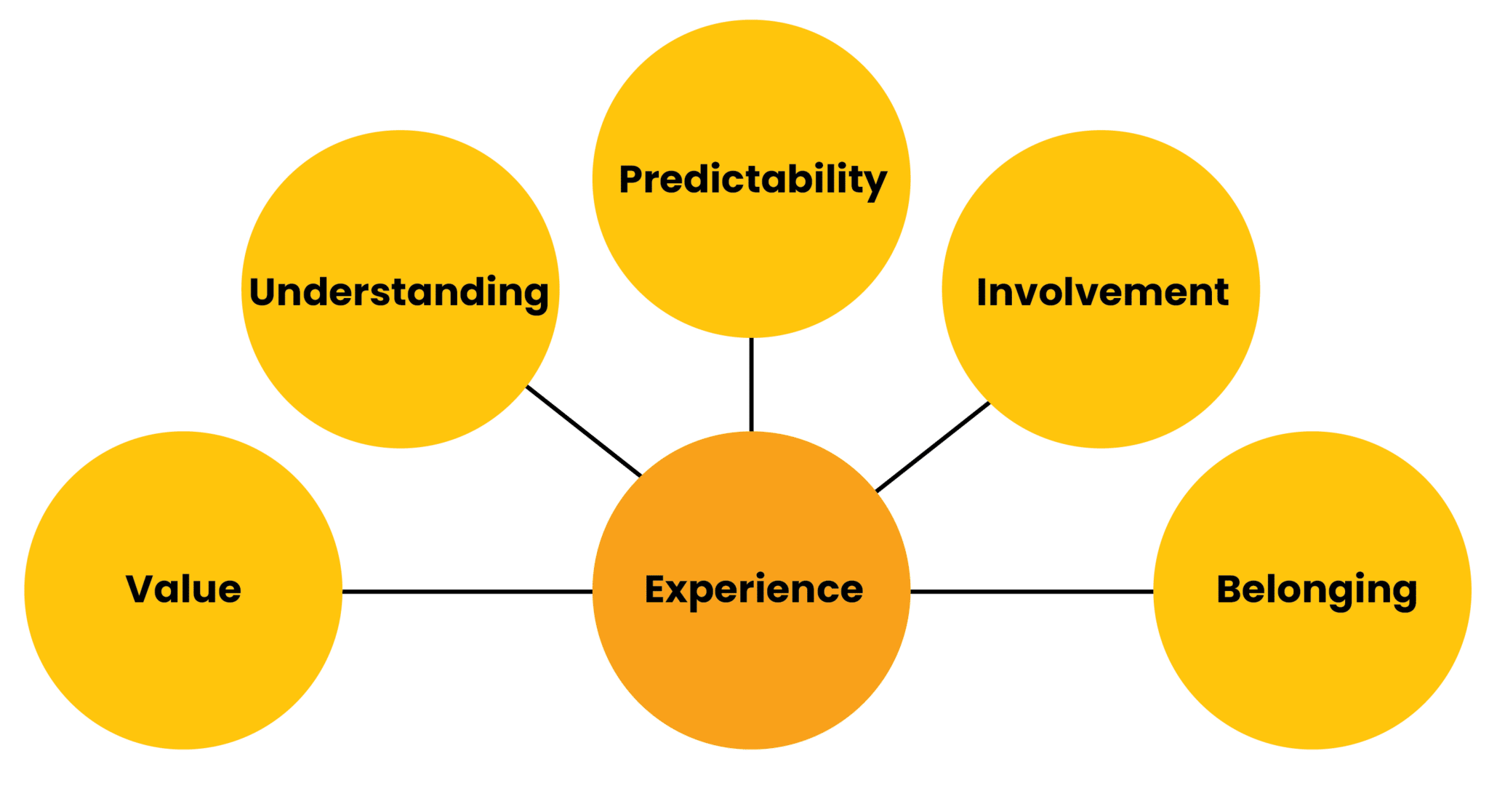

“Serious Shift” is not a repetition of “The Experience Economy” though both books think of the workers in a people-focused business as actors on a stage. The final section of “Serious Shift” made the biggest impression on me, because it contained the chart below. The chart, which should be read from right to left, can remind you of what actions to take to “up” your clients’ experiences. I discuss the components of the chart in the next section.

Six ways to improve your experience economy

As you read the rest of this article, note that it is written from my perspective as an octogenarian. I hope this somehow helps you serve your senior clients, who may think in a similar vein. However, my beliefs are of course also based on my experiences.

Belonging

“Serious Shift” author Dennis Moseley-Williams says, “Customers appreciate being recognized as members of a select community” and “Special membership bestows a sense of uniqueness to the purchaser and strengthens their commitment and allegiance to the business …”

What could give your clients more of an affinity for you and your firm? But I am not thinking that you should hand out gold cards to your clients, like your airline or hotel chains may do. In fact, the old conventions of gold, silver and bronze are not a good way to think of clients. If you don’t want to service a low-end client, wouldn’t they and you be better off if you found an advisor who valued them? If you do distinguish tiers, I suggest Triple A, Double A and A — and think in terms of their needs.

Perhaps a Triple A needs or wants monthly contacts and a Double A only needs contacts every other month. Perhaps a Triple A needs or wants annual planning reviews because of complexities and a Double A only needs this every second year. In all cases, your service model needs to be transparent to each client and tier. And keep an extra cell phone for Triple A clients only and let them know it works 24/7/365 for both spouses.

You can also plan events by tiers so you can pay equal attention to members of that group. Also think about personalized note cards that recognize your clients’ value to you. If you have 150 clients, you can write one personalized note to every client each year. You can write just one note a day on 50 Mondays, Wednesdays and Fridays – but your clients are likely to remember it all year.

Whatever you do, you must be genuine and sincere. This includes having a proactive contact plan, being highly responsive and always being an active listener. I mentioned WOW experiences before. Know the dates that are important to your client (including their family, parents and children). Make sure your support staff knows your clients. Client bios and photos can help your team get to know them too.

Make it a point to get to know not only the financial side of your clients, but even perhaps their physical, emotional and spiritual sides, so you can deliver true personalization and a feeling of belonging. Socializing with clients individually and collectively is also important. You must share yourself and be willing to be vulnerable while maintaining your professionalism. No, none of this is easy.

Involvement

Moseley-Williams states, “Customers desire a heightened level of involvement in their business interactions.” So, how can you deliver this to our advisory clients?

Many advisors adapt their language to talk about “we” and “our.” For example, it’s not your investments, it’s our investments; it’s not your plan, it’s our plan. This is about participation and collaboration. It depends on the client, but it’s about listening, sharing and asking to hear their perspective. Even if the client doesn’t know their specific holdings, help them understand why their portfolios are structured the way they are.

Get to know the client’s family, professional and personal situation, character and values. Involvement also includes sharing your true self and showing a willingness to be vulnerable, open and transparent.

Many years ago, Merrill Lynch developed a contact approach called “Supernova,” which I still profess. It includes monthly client contact: four quarterly meetings (two in person, two by phone or online) and eight shorter “check-in” calls on other months that provide more personal discussion time. This is in addition to informal, ad hoc personal meetings. Meetings must also be collaborative and it’s preferable when both spouses or partners attend.

You can personalize every relationship to some level. At some point, you may have to limit the size of your practice and have a team structure as you move towards a more experiential relationship delivery.

Predictability

“Customers need to know that what they will receive … will be consistently provided every time,” says Moseley-Williams.

Delivering predictability is a model. Every client tier has a unique client service model that is initially discussed with the client and reviewed annually to ensure that’s what the client wants, needs, expects, and, most importantly, values. The model or promise is modified as needed and/or wanted. Always aim for delivering consistent, excellent quality in your planning work, review meetings, chats, etc. It’s also important for you and your client to know that consistent quality is your goal, although the markets are not under your control.

Clients also need predictability in who you are, during good times and bad — through your attitude, your availability, etc. It has been said, “If someone is nice to you but rude to the waiter, they are not a nice person.” So, be predictably nice!

Understanding

Share your process, your service model, and your fees so clients understand what you do and why and how you do it. And let them know you want to understand them by being compassionate and empathetic. Put yourself in your client’s shoes. Feel what they are feeling and think about how you would like to be treated and/or spoken to. You know that oftentimes little you say or do will change a client’s personal situation. Try anyway.

Be highly aware of your client’s life, and when they need a friend. Do your best to be that friend. There are few greater gifts one can give than time and attention. Kindness counts.

Value

As Moseley-Williams says, clients look for value where money changes hands. More importantly he says, “What is memorable to customers is something that is personally valuable.” This ties into experiences.

For many decades, I have believed that value is a state of mind; is it not a calculation or how many basis points that keeping clients from making emotionally driven decisions. At the end of the day, clients decide what is valuable to them. Most people with assets don’t want to do what you do and therefore they will pay you or someone else. Give them a good experience, and they will see greater value.

Ask clients if they see the value in what you do — and why and how. Make sure they understand your deliverables and their portfolios, and are highly satisfied with you and your work.

Experience

The five areas discussed above — belonging, involvement, predictability, understanding and value — generate feelings and beliefs. There are no pure metrics that can be applied; you can do client satisfaction surveys to get feedback. And as you create experiences to make your clients feel good about your work together, think about the ultimate benefits they seek as a result of your careful planning.

Although I do get good feelings and experiences from my financial advisory team, the real benefit are the feelings I get from them having helped make it possible for me to live a life that includes sitting in Italy after a beautiful lunch by the sea, watching boats on the clear blue Adriatic, and then walking through the narrow streets of an old village with my wife.

As Moseley-Williams said, “By understanding these expectations, business owners can then create experiences that can be transformative, both for their clients and for their own professional and corporate growth.” He also said, “From imagination comes inspiration and inspiration, in turn, leads to innovation.”

If you can think it, you can do it.

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David has worked in the financial services industry for decades, originally as a consultant with IBM and then with UBS/Paine Webber before starting his own firm. If you would like more information about his services, contact him at David@CoachDavidLeo.com or visit www.CoachDavidLeo.com.