Are target-date funds supposed to protect their investors from losses when they are a few years from retirement or newly retired? Some investors might think so, but that’s not what happened in 2022.

In fact, investors in 2025 target-date retirement investments had a bumpy ride in 2022. It was the year, Morningstar Inc. says, that “(almost) nothing worked.’’

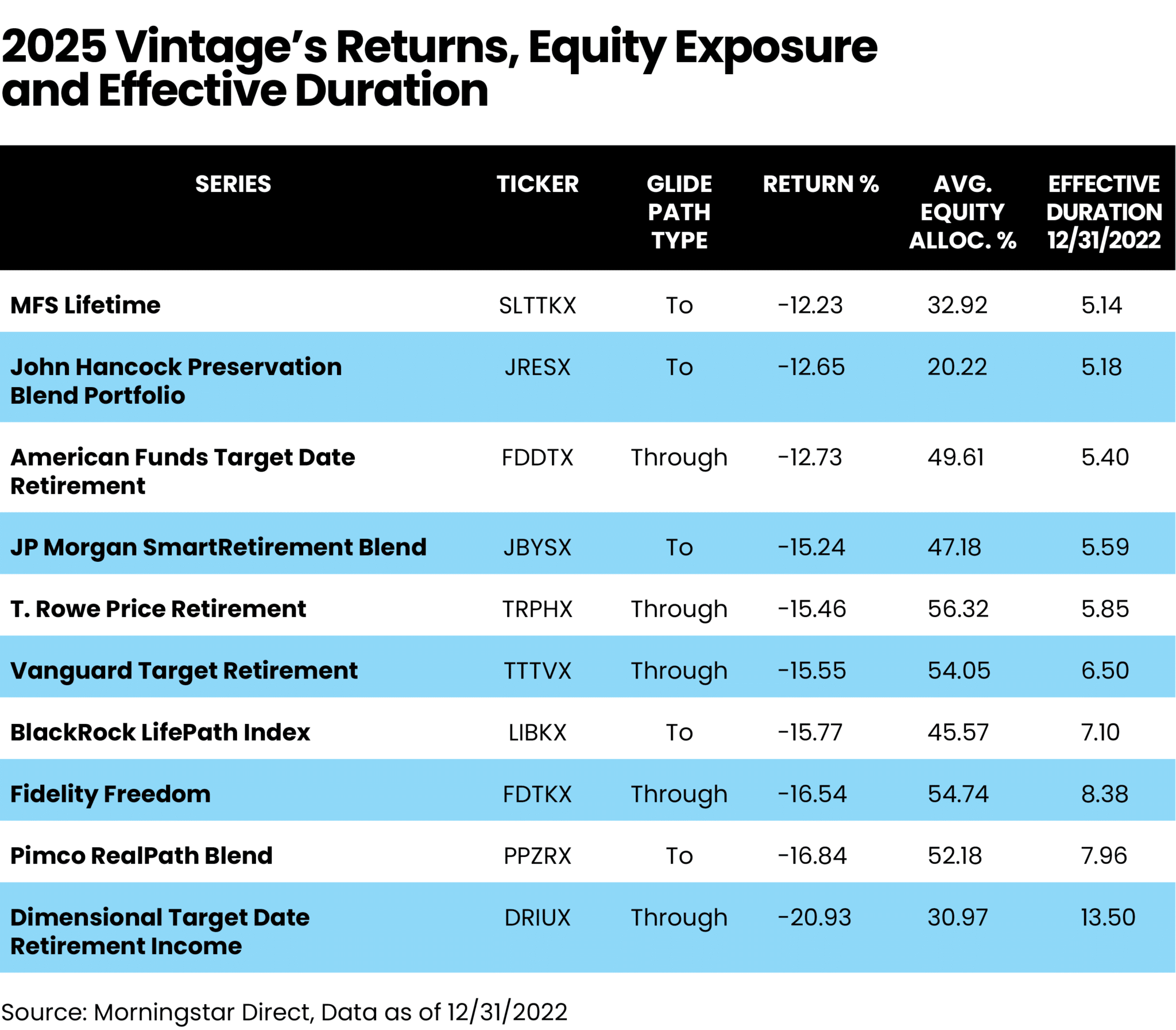

“Target dates designed for people retiring in 2025, a good proxy for people near or in retirement, all lost money regardless of their glide paths or underlying exposures,’’ says the Morningstar report, Target Date Strategy Landscape: 2023.

“The 2025 average category lost a little over 15%, which is a pretty significant amount if you are approaching retirement,’’ said Megan Pacholok, a coauthor of the report, in a recent interview. “It really depends on how your glide path is composed as to what your performance was. Higher equity exposures contributed more to losses, because equities lost more than bonds in 2022.’’

Nearly five months into 2023, target-date funds have gained about 4.7%. “They still have more to make up,’’ Pacholok said.

A 2022 analysis by Project Finance showed that over the previous 10 years, the S&P 500 vastly outperformed Vanguard’s 2030, 2040, 2050 and 2060 target-date funds. Some of the outperformance is to be expected for the 2030 fund, since the retirement date is relatively close, Project Finance said. (Vanguard target-date funds amassed the most net inflows in 2022 and have been in the top spot in all but one calendar year since 2008.)

“Target-date funds get a lot of things right (they produce a phenomenal diversified portfolio for individual retirement accounts) – but they get a lot of things wrong as well,” Project Finance said. They don’t consider investments outside the fund, they assume all investors have the same risk tolerance, don’t adapt to investors’ needs and don’t include as much equity exposure as some financial professionals think is needed.

In 2022, target-date strategies raked in $153 billion in net assets, Morningstar said. Total target-date assets fell to $2.82 trillion in 2022 from their record high of $3.27 trillion in 2021. Market depreciation drove the roughly 14% drop.

Vanguard, Fidelity, T. Rowe Price, BlackRock and American Funds dominate the target-date market, controlling about 80%; the top 10 players claim roughly 93%, said Morningstar.

When panic sets in

A losing year like 2022 can jolt “hands-off’’ workplace investors who overwhelmingly prefer that pros make investment decisions.

“Most investors for target-date investing are doing it through automatic withdrawal through work, so you don’t have to consciously go in and change your allocation,’’ said Pacholok, a Morningstar senior analyst, multi-asset manager research. “Managers who are expert in their field are in charge of asset allocation for you. It’s great for a wide audience who prefers a more hands-off approach.’’

But with losses so close to retirement in what is meant to be the safely conservative phase of target-date investing, panic can set in, withdrawals are made and losses are increased, Pacholok said.

Morningstar’s report says a “perfect storm’’ of factors pushed 2022 into the losing column.

“Market turbulence shows target-date strategies aren’t immune to market shocks and aren’t all built the same. Diversification across stocks and bonds has usually helped during market turmoil and over the long term. Sometimes, however, correlations between major asset classes, such as stocks and bonds, spike and there’s nowhere to hide.”

“That happened in 2022 as stock and bond markets fell in tandem as the Federal Reserve reined in loose monetary policy with seven interest-rate hikes, Russia invaded Ukraine, a cryptocurrency exchange imploded, and investors grew wary of any kind of risk.’’

Treasury inflation-protected securities (TIPS) suffered losses in 2022, and inflation was a major factor in the year’s disappointing performance. In fact, target-date 2025 funds with the longest bond duration performed the worst in 2022, Pacholok noted.

“Target-date portfolios constructed on the historical assumption that investment-grade bonds would serve as a ballast in rough markets suffered as their stock and bond holdings fell in 2022,’’ the report says.

Perhaps even more concerning for investors, the report said “target-date funds captured more of the equity market’s downside than expected based on their strategic equity weightings.”

Glide path impacts

But accepting the risk of losses, even as target-date fund investments reach the conservative stage, is essential, Pacholok said. “It really depends on which strategy you are invested in, which glide path.”

Target-date strategies are often structured around one of two glide paths. A “to” glide path stops lowering equity exposure at the target date, while “through” glide paths continue to lower equity exposure for 10 to 15 years after the retirement date, the Morningstar report said.

Pacholok said a through glide path can continue to be risky even with lower equity exposure. “With the kind of portfolio that has more equity, you also need to ask how much credit risk is in your portfolio. Bond portfolios can experience more volatility than fixed income,” she said. “You never expect a loss from a target-date fund, but there is always risk with investing.’’

Staying the course

The report says that “drawdowns hurt investors closer to or in retirement more because they should have bigger balances and plans to switch from contributions to withdrawals.”

Said Pacholok, “Staying the course should serve investors well, but it’s a bit different if you are nearing retirement and you start making withdrawals. If you start withdrawals, it gets worse; you’re spending down the money and you are locking in those losses and removing your ability to experience a market rebound. It’s tough advice but if you are able, stay with it; it’s one of the best things you can do.’’

In a four-decade career in journalism, Eleanor O’Sullivan has reviewed many books on best practices for financial advisors, has written for Financial Advisor and the USA Today network, and was the movie critic for the Asbury Park Press.