College costs continue to skyrocket but you wouldn’t know it by looking at the admissions office activity. The most expensive schools continue to receive a record-breaking number of applications, putting these institutions in an enviable position to turn away 90% (or more!) of the students that apply..

Imagine running an increasingly popular luxury brand business that allows you to tell 9 out of 10 customers to look elsewhere. This is an enviable business model for any industry, but particularly lucrative for prestigious colleges. In fact, some schools have stopped publicizing their admissions data, including acceptance rates and demographic breakdowns.

The Ivy League term was initially coined in the 1930s but really took hold in 1954 when eight private research universities located in the Northeast were grouped together in a collegiate athletic conference. The eight Ivy League schools (in alphabetical order) are Brown University, Columbia University, Cornell University, Dartmouth College, Harvard University, Princeton University, University of Pennsylvania and Yale University.

But these aren’t the only schools that cost more money, accept fewer students, and remain unphased by the headlines that suggest higher education is facing a serious shortage of students beginning in 2026. In fact, for the 2022-23 school year, there were at least 25 colleges that charged more than $80,000 and those prices are set to increase across the board next fall.

Perception is powerful

So why can the top 1% of colleges continue to raise prices with no end in sight?

Parents and students believe an Ivy League diploma leads to more money, more access and better networking.

Graduates of Ivy League schools do tend to make more money than non-Ivy grads. According to a PayScale/U.S. News analysis, 2022 median pay in early career (which Payscale defines as three years of work experience) was $86,025 for Ivy grads compared with $58,642 for non-Ivy grads. In mid-career (20 years), it was $161,888 Ivy vs. $101,777 non-Ivy. But the data can be skewed because most students graduating from these schools end up in higher-cost-of-living areas.

A big head start

However, it’s not only where graduates end up living but also where they hail from. More specifically, kids from wealthy homes are more likely to thrive in the workforce anyway for various reasons, experts say.

In fact, the financial value of an Ivy League degree is debatable for students from high-income families, Jeff Strohl, director of research at the Georgetown University Center on Education and the Workforce, said earlier this year in this U.S News & World Report article. Many of these students attend rigorous prep schools and already have greater career prospects than the average student by the time they arrive at an Ivy League school, said Strohl, a co-author of the book “The Merit Myth: How Our Colleges Favor the Rich and Divide America.”

And there are reports that suggest neither Harvard nor Yale make the cut in terms of giving a student the chance to make the most money over time, suggesting families would be better off looking at some non-Ivy schools for a bigger payday.

Lost in the middle

The people who can afford to send their kids to the Ivy League and other highly selective universities will continue to do so because they can. Smart kids from low-income families are also likely to have their financial needs met because most of the Ivy League schools are very generous with financial aid.

To varying degrees, well-endowed universities are helping make school affordable for growing numbers of low income and first-generation students.

Not surprisingly, the segment of the population that’s losing out is “in the middle.” Not wealthy enough to be able to pay the full ride for school but too well off to qualify for need-based aid.

Many of the mass affluent and middle-class clients we serve cannot “do whatever it takes” if their student is admitted to these increasingly expensive colleges. They make a good living, live in nice houses, drive nice cars and fund their retirement accounts — but they can’t do it all if that includes $90,000 a year in college expenses.

Reality check

Let’s go back a minute to perceived value, which is not a simple concept. Is the Porsche Cayenne really a better vehicle than the Acura MDX? In terms of metrics, there are lots to compare. But how do you measure the way you feel when you get into the vehicle or pass that truck you’re behind or hug that corner at high speed?

With schools, it’s easy to get caught up in that exhilarated feeling without thinking about the financial consequences of those decisions. That’s why we must serve as the gatekeeper and provide the guardrails for these families when they are buying college. If we helped parents approach buying college like they approach buying a house (or a car), we would serve them well.

First, we should be helping families understand and build a list of schools that make sense for their budget and can result in better economic outcomes for the whole family. Not only shouldn’t kids be saddled with out-of-control debt, parents shouldn’t be jeopardizing their retirement savings.

Reverse engineering

The “middle” households with college-bound students in America would benefit from using a straightforward “recipe for success” when it comes to funding college education.

Imagine using an affordability calculator or formula to determine what families could afford. Sounds a little like a pre-approval process on a mortgage, doesn’t it? We could then send them to shop in the college zip codes they could afford.

I found a way to do just that, using my own formula that evolved as a result of helping families for more than 20 years. This formula allows me to reverse engineer families’ spending plans and ensure that we balance their current lifestyle, their future lifestyle (aka retirement) and paying for college.

20% + 5% + 50% + 25% = 100%

Here’s what this equation is all about:

20% = family’s down payment

This is set aside in a 529 college-savings plan, I Bonds, etc. Putting down only this much for college is an interesting paradigm shift for our industry because too many parents save more for college than they do for their own retirement and don’t comprehend the tradeoff they are making.

5% = current lifestyle cash flow “offshored” to college

The cost of a student living with their parents is baked into the family’s existing lifestyle. These expenses – including food, entertainment and activities — won’t go away during the college years; they will simply be “offshored” to the college of choice.

50% = the financed portion of “buying college”

The misunderstanding of the current student-loan system has led to the underutilization of direct student loans. Every family should take advantage of the undergraduate direct student loan program because of the low origination fees, below market interest rates and attractive income-driven repayment plans. Explaining this is truly an area where financial advisors can add value.

25% = discounts, coupons or points

Perhaps the most misunderstood and overlooked component of the college funding strategy is that an entire year of college should be paid for by the student or the family’s lifestyle. This should not be with money earned but with quantifiable discounts earned. Think of it as the student’s job to “clip coupons” during high school and bring them to the register when it’s time to pay the bill.

These coupons should include merit aid, scholarships they find through organizations, and redeemable points. For example, Tuition Rewards® offers redeemable reward points for buying or doing things in everyday life. Another example is RaiseMe, a social-enterprise platform that gives high school students the opportunity to apply for micro-scholarships at the more than 330 colleges it has partnered with.

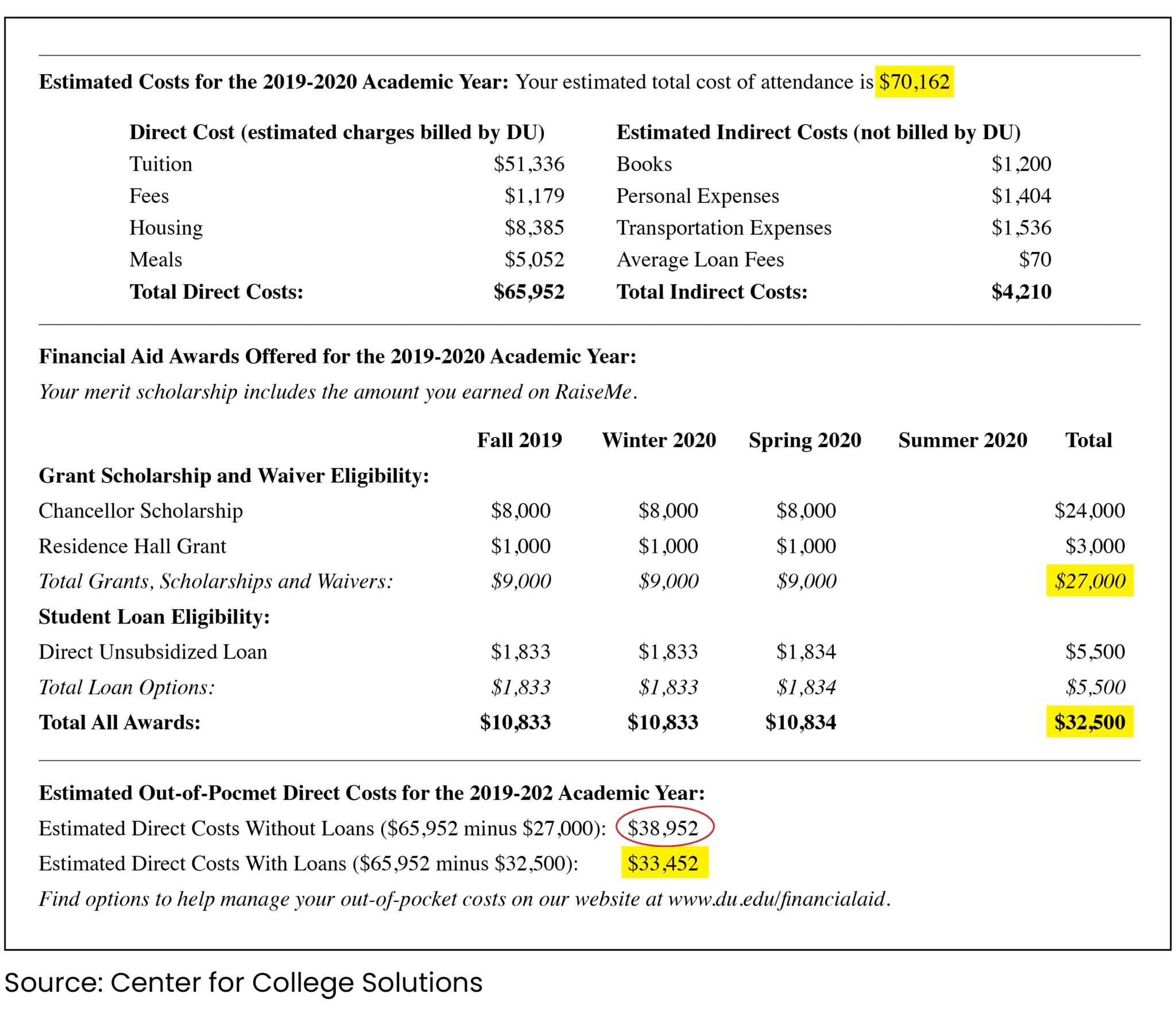

An actual award letter

Here’s an example of an actual award letter that demonstrates the student “earning” $27,000 in scholarships and grants based on their unweighted GPA, standardized test score, and strength of high school coursework.

This award letter, from the University of Denver (DU), demonstrates the pricing power families can bring to bear in the college quest and exemplifies the benefits of understanding how to choose the right schools for application. Between financing and discounts, the student’s cost of college for the academic year was reduced by 50%.

This family understood before the student hit submit on the application that they would be eligible for this type of award package. Add in a few third-party scholarships and tax credits over four years and this part of the formula really delivers on its promise.

No one ever explains this component of the college funding equation to parents — or to students. So, most families suffer “would’ve/could’ve” regret that proves to be very, very costly.

And because not every student can clip the most valuable coupons, this part of the funding strategy can and should impact the actual college education purchased. For example, kids who don’t bring any coupons to the register would end up buying the discount or generic brand of college. Nothing wrong with that; it’ll get the job done.

Other kids who clip several coupons will be in a position to buy the more expensive, recognized brand name product at an affordable price. This is good for them financially, and they’ll have pride of ownership in the purchase.

Final thoughts

Is an Ivy League education worth it? For most of the families we serve, the simple answer is no.

With our guidance and financial guardrails, families can find there are many colleges that will provide an excellent undergraduate experience for a fraction of the cost. We can add value by shrinking the universe of choice, identifying affordable schools that meet the family’s success criteria, and creating a funding plan that delivers a more cash flow efficient and tax efficient payment for college.

Most financial advisors practicing in this niche have relationships with independent education consultants and career/major coaches that partner in developing a total solution for the family — not unlike working with a CPA and estate planning attorney to implement a well-crafted estate planning strategy for your client.

Beth V. Walker is a wealth advisor with Carson Wealth Management and founder of Center for College Solutions, which is based in Colorado Springs, Colo. She is also a member of the SFC Consortium, a group of professionals which helps match families with colleges. She can be reached at bwalker@carsonwealth.com or 719-522-2278.

College costs continue to skyrocket but you wouldn’t know it by looking at the admissions office activity. The most expensive schools continue to receive a record-breaking number of applications, putting these institutions in an enviable position to turn away 90% (or more!) of the students that apply..

College costs continue to skyrocket but you wouldn’t know it by looking at the admissions office activity. The most expensive schools continue to receive a record-breaking number of applications, putting these institutions in an enviable position to turn away 90% (or more!) of the students that apply..