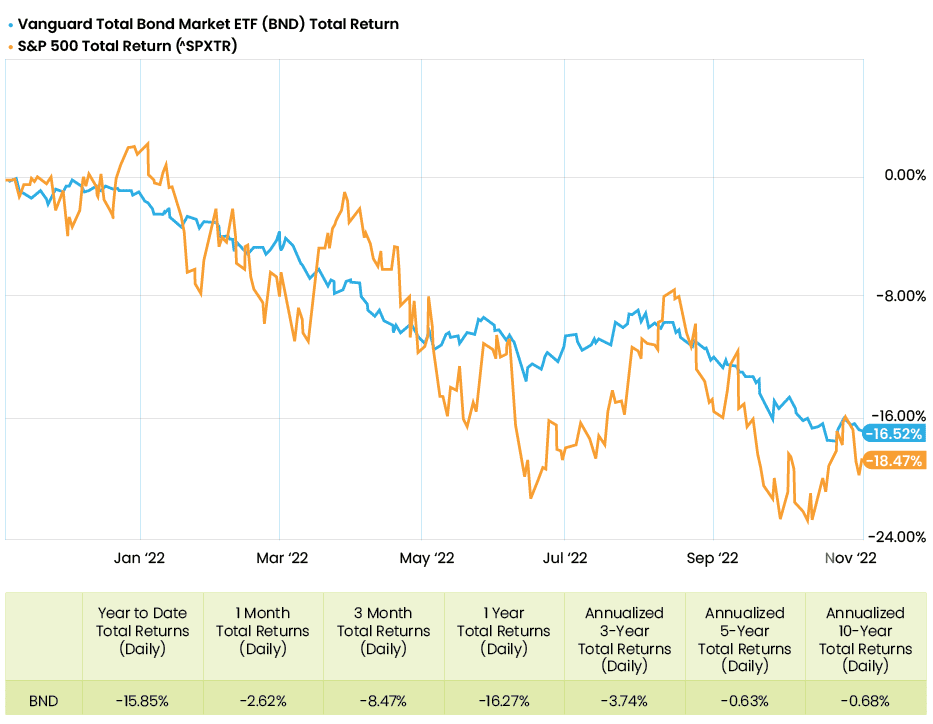

Interest rates have increased dramatically in 2022, leading to significant declines in bond prices. You may be most aware of this if you own a bond mutual fund or ETF. The share price of most have declined, and in many cases, the percentage decline is in the double digits. Here, for example, is the performance of a well-known bond ETF, the Vanguard Total Bond market ETF (Ticker: BND).This ETF tracks the Bloomberg U.S. Aggregate Bond Index by investing in securities within the total U.S. investment-grade bond market.

The total return for that ETF is -14.1% YTD through mid-November 2022 (chart numbers as of October). That is a stunning decline for this asset class — bonds that are supposed to provide stability to one’s portfolio.

Recovering from this decline may take years. At the current yield for the fund slightly over 4%, it will take over three years to break even if there is no further decline or if the fund’s share value does not recover. A problem for bond mutual funds is the redemptions. To raise cash to provide liquidity for the redemptions fund, managers tend to sell the assets that declined the least — usually the highest quality holdings. That could cause the remaining shareholders to own a fund with reduced quality. This means it is more likely the decline will not be offset with a gain anytime soon. ETFs are not subject to this issue because shares are traded to another person instead of being redeemed by the manager.

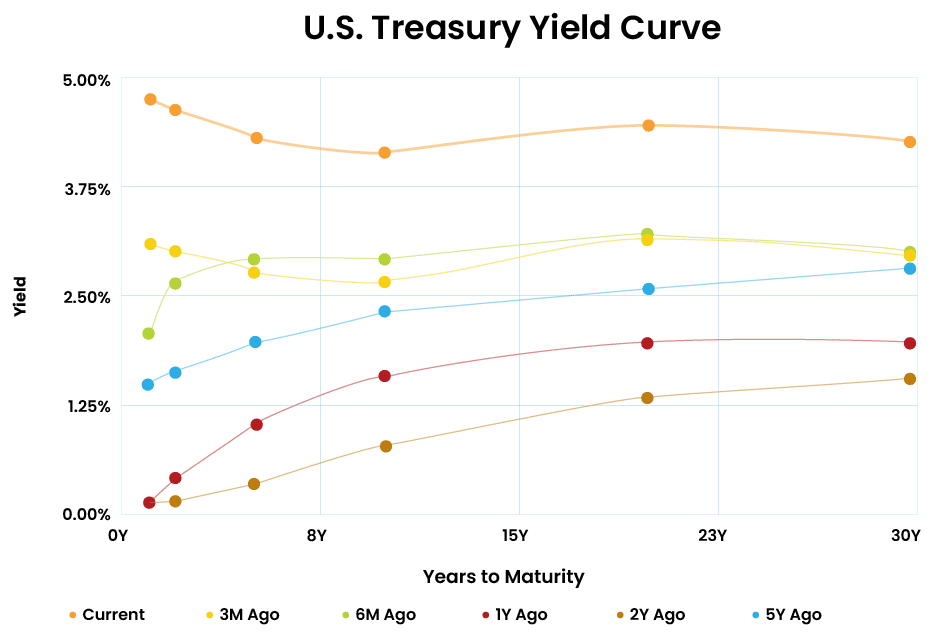

The chart below includes several yield curves showing how rates have changed over the last five years:

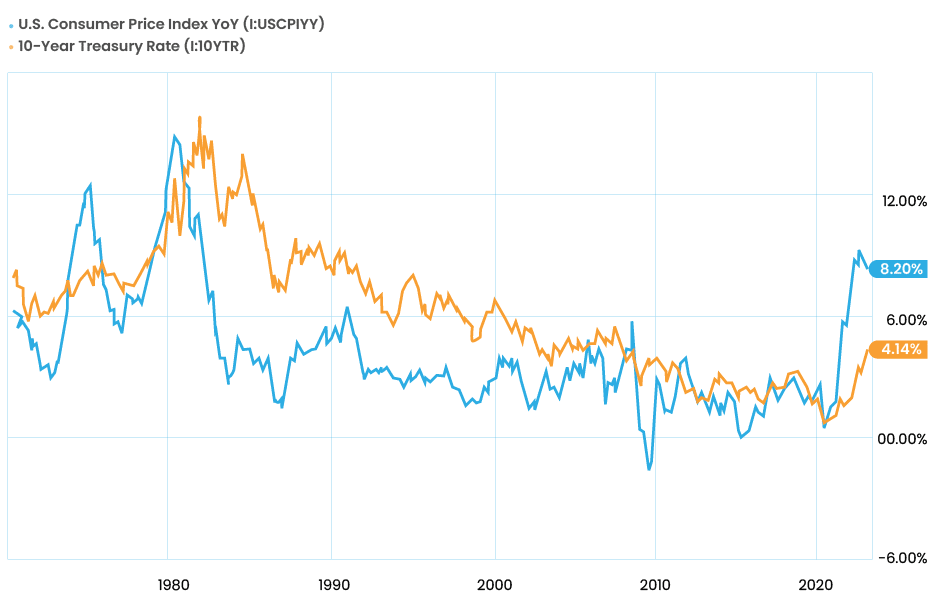

As you can see, rates have increased significantly over the last year due to the Federal Reserve raising the federal funds rate. The current yield curve is “inverted,” and shorter-term rates are now higher than long-term rates. In the past, that was a sign we could be nearing a recession. Unfortunately, rates on Treasurys are not favorable when compared with inflation. The current yield on 10-year Treasurys is about 4% below the current inflation rate.

In the past (at least in the 1970s), there was a lag as the 10-year Treasury gradually caught up and exceeded the inflation rate, providing an actual positive yield. Whether that will happen again is anyone’s guess.

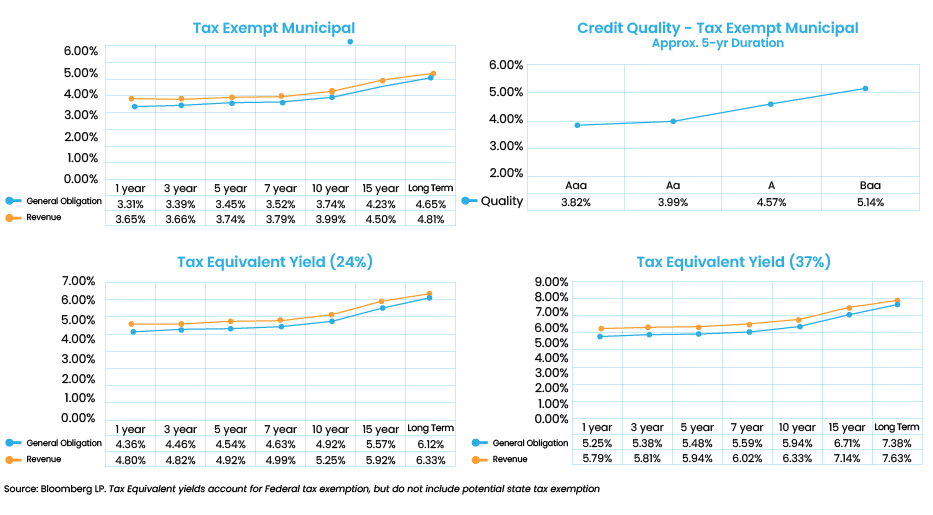

Yields on municipal bonds have also increased significantly over the last year, providing a reasonable rate of return, adjusted for one’s tax bracket, as evidenced by the chart below:

As seen from the graphs, the yield on high-quality municipal bonds is now the taxable equivalent of 4.3% and 5.2%, respectively, if you are in federal marginal tax brackets of 24% or 37%. Those are the highest yields we have seen in years. (To calculate the taxable equivalent yield or TEF, divide the nominal rate by 1 minus your marginal tax bracket.

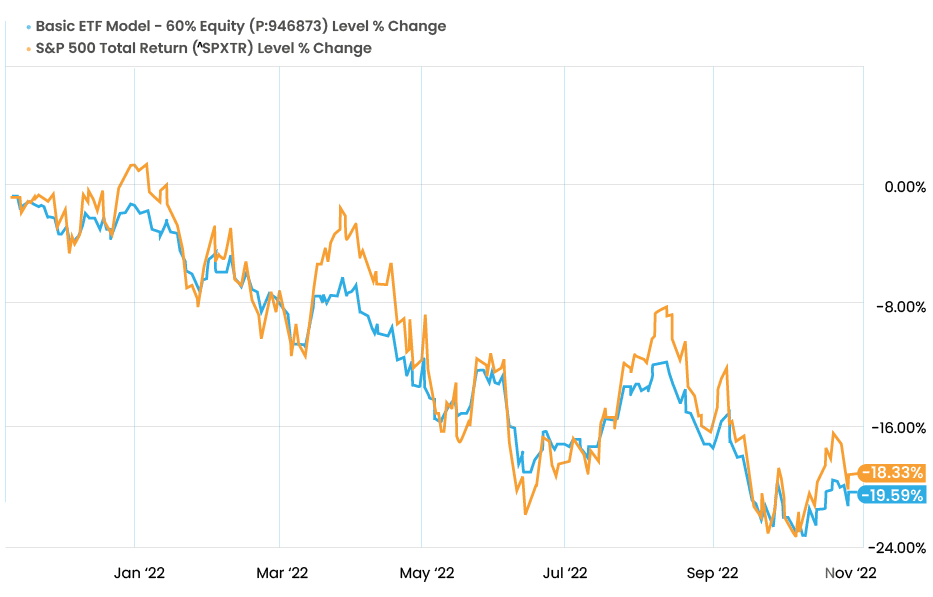

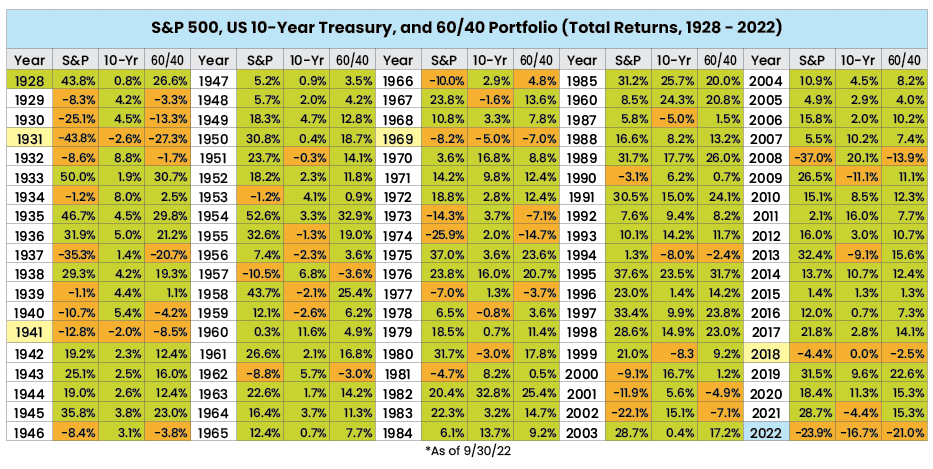

The traditional combination of 60% equity and 40% bonds is a simplistic asset allocation that many non-specialists and even advisors use (despite the supposed superior knowledge of advisors). This combination is experiencing a historically awful year. Here is the performance of an ETF portfolio modeled after that allocation:

The 60/40 asset allocation is now experiencing one of the worst years in history:

In conclusion, bonds will provide a decent yield for the first time in years. Unfortunately, those using bond funds and ETFs to gain exposure to fixed income have a rough road ahead. Although, equity markets tend to recover quickly after significant declines, bond returns are purely based on math: their yield and the level of interest rates in relation to their yield, term to maturity and credit rating. Bond funds and ETFs may take years to recover and may not recover unless interest rates drop. We think this is a good argument for ditching those vehicles and considering owning individual bonds instead. We hope that inflation subsides, but fixed-income yields do remain at reasonable rates.

Stephen Craffen, CFA, CFP,ChFC, CLU, is chief investment officer and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla. He is also a former national chair of NAPFA.