Investors are shocked that the so-called 60/40 portfolio failed to provide protection from the bear market in stocks this year. Many thought stock and bond prices always move in opposite directions, which was the foundation of their diversification strategy. Today the average 60/40 portfolio is down 18.63% compared with an 18.6% decline in the S&P 500, so this belief was wrong. The combination of rising interest rates and the threat of a recession has hammered both stock and bonds.

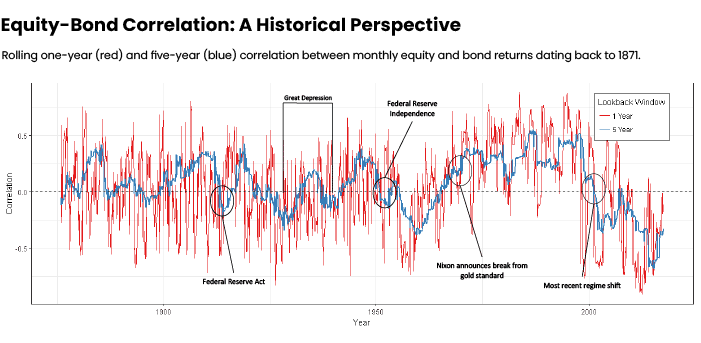

While the equity-bond correlation has been negative since the early 2000s, this negative correlation is far from enduring. Before 2000, the last time the correlation was negative was from 1950 to 1965.

Fan and Mitchel (2017) computed the rolling 1-year and 5-year correlation between equity and bond returns showing the dynamic nature of correlation cycles. During the initial periods of growth and inflation through the 1980s, the correlation between equities and bonds was positive (over a 5-year rolling window). This correlation peaked in 1997 but remaining positive until the early 2000s. It then turned negative, hitting the lowest 5-year correlation in 2015 and rising rapidly.

It is easy to conclude that inflation or monetary policy expectations drive correlations, but it is more complicated. It is due to a multitude of economic factors. Another study by Shen and Weisberger (2021) posits correlations are associated with interest rate volatility, the co-movement of economic growth and interest rates, and the co-movement of equity and bond risk premia. However, even if we could fully identify the drivers of correlation, forecasting what the Fed will do and how the economy will respond remains challenging. This is why we cannot count on bonds as the sole source of diversification.

The most common way to measure the relative movements between stocks and bonds is through a statistic known as the Pearson correlation. Correlation measures the tendency of different investments to move up or down at the same time. When measuring correlation, a zero reading indicates that assets are moving with no apparent relationship, while a correlation of one means gains or losses occur in perfect unison. Positive readings mean direct correlations. Negative readings are known as having inverse correlations.

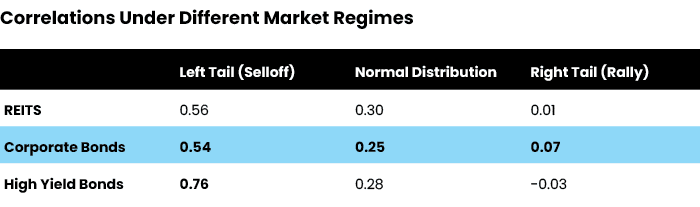

But because investment returns are not normally distributed, correlations used to model interrelationships between asset classes are unstable. They do not correctly model the nonlinear behavior that leads to increases in exposure to downside or shortfall risk. Even using all the historical data available, correlations can change dramatically during different market regimes.

Corporate bonds, for example, have low correlations with stocks during market rallies but high correlations with stocks during market selloffs. The table below illustrates large-cap stocks’ interrelationships with REITS and bonds under different market regimes, illustrating how correlations can be misleading.

Measuring relationships when creating a portfolio

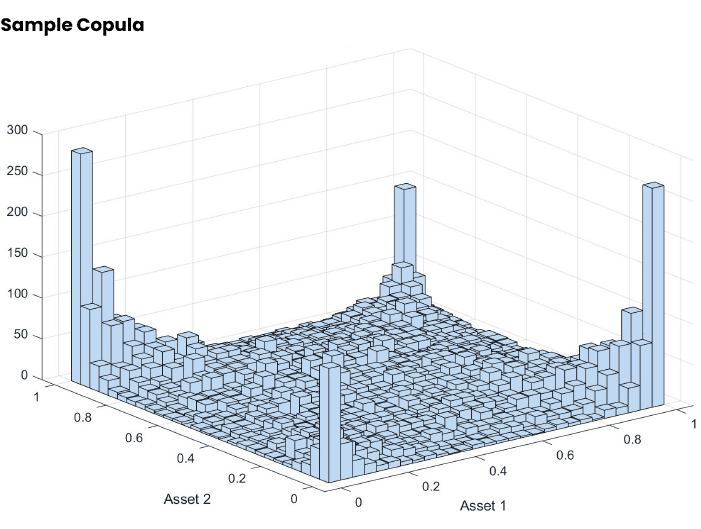

There are several ways to model interrelationships when these relationships are not static. The method we use at At Atlas Fiduciary Financial is a complex mathematical construct called a Copula.

Copulas replace the single-point correlation with a mathematical probability distribution that can take on complex shapes. They are much better at modeling nonlinear relationships and can incorporate unsymmetrical correlations and extreme events. Here is a sample Copula:

How does this help us create a truly diversified portfolio?

Modern Portfolio Theory works when you understand statistics and can identify enough asset classes with different sources of risk, with some negatively correlated in any given period. Combining those assets in a portfolio improves its “efficiency” — the ratio of risk and return. Therefore, we use various asset classes in all of our client’s portfolios, including the alternative asset class.

Liquid Alternative asset class strategies

While there are other asset classes we use to diversify adequately, the alternative asset class contains unique investments that fall outside the traditional asset classes commonly accessed by most investors. Alternatives are an excellent way to diversify your portfolio with their low correlation to traditional asset classes. These hedge fund-type strategies are not actual hedge funds since they trade publicly. Ideally, a professional portfolio manager would select and monitor these funds since they require specific knowledge.

Liquid alternatives consist of hedge fund-type strategies. Though we classify this as an asset class, it combines various strategies. We use three or four, which we will describe below. The purpose of this category is to provide growth that is somewhere between the long-term return of bonds and stocks but with volatility that is more like a bond. We have seen these holdings hold up reasonably well during this and past market downturns. The strategies include:

Long/Short Equity

The manager invests in the stock market by holding individual stocks, and then attempts to make their fund less sensitive to market declines by selling stock short. Selling short is selling stock one does not own.The manager borrows the shares from a third party, typically a brokerage firm. They will have to ‘pay” back the loan by replacing the borrowed shares.Let’s say the manager believes the stock price will drop and sells the stock at $50/share. If the stock drops to $40, they can purchase it and return the shares, netting $10 per share. They can profit even if the market as a whole or an individual stock drops.

This is also a way for a manager to use all their research; they may identify companies they think will perform nicely and companies that will perform poorly and can profit from either.

Market Neutral

This strategy is related to long/short, except it tends to balance the long positions with the short positions to thoroughly dampen volatility. The biggest benefit comes from investing the free cash that results from selling stock short. When the fund manager borrows shares, they may only have to commit 10% of the value of the shares to the lender. Therefore when the manager sells the shares, they can hold the other 90% and invest it. Typically, they may invest it in Treasurys or some other short-term investment. Market Neutral will have the most bond-like performance of these strategies.

Convertible Arbitrage

This strategy is related to convertible bonds and to the market-neutral strategy. Here the manager buys a convertible bond and simultaniouly sells short the company’s stock. They are attempting to profit from price inefficiencies for the convertible bond in relation to the underlying stock. This potential opportunity exists due to the potential mispricing of the credit component, the income component, the equity component, and the volatility component of the convertible bond. This is a very intensive process, and the management team we have been using focuses on small and midcap bonds that are not yet rated.

Merger Arbitrage

This strategy involves profiting from company takeovers and mergers. When someone announces a takeover, the purchase price is usually significantly higher than the market price. Almost immediately, the target’s stock price jumps and, in most cases, to within 10% or so of the takeover price. It does not rise to the exact price level due to the uncertainty associated with mergers, and there may be regulatory issues, etc. Also, the stock price of the company that is the acquirer typically drops. As the takeover date approaches, the target’s stock gradually rises to meet the takeover price while the acquirer’s stock usually falls. In this strategy, the manager profits by buying the target’s stock and selling the acquirer’s stock short.

The Challenge

While alternatives can offer another source of portfolio diversification and lower overall risk to protect a portfolio, it is important to monitor them closely and choose ones with the lowest possible expense ratio. Here at Atlas, we watch these choices carefully and routinely compare them to the universe of available options. As alternative investments become a larger part of the investing landscape and more available to different investors, they’re increasingly important to know about and consider in a dynamic investment climate.

Laura Mattia, PhD, MBA, CFP, is the CEO and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla.