“The most important job is to strike the appropriate balance between offense and defense.” — Howard Marks

Market downturns are inevitable and, unfortunately, we can’t control when they will happen. So when planning for retirement, how can your clients avoid the negative consequences of an untimely downturn?

In today’s volatile market, it’s essential to consider the headwinds you have in managing sequence of returns and how you might think about addressing it — particularly for clients approaching or entering retirement today. As life expectancies for women and men continue to grow (84.5 and 82, respectively, in 2020), planning for sequence-of-return risk becomes even more important as the years in retirement are extended.

As you plan for both asset growth and a distribution strategy for clients, mitigating risk and increasing flexibility are the most common planning themes to address sequence risk.

Let’s dive into a few of the strategies for mitigating sequence-of-return risk and why they may or may not make sense for your clients in today’s market environment. I’ll also introduce a solution you may not have considered before – owning volatility.

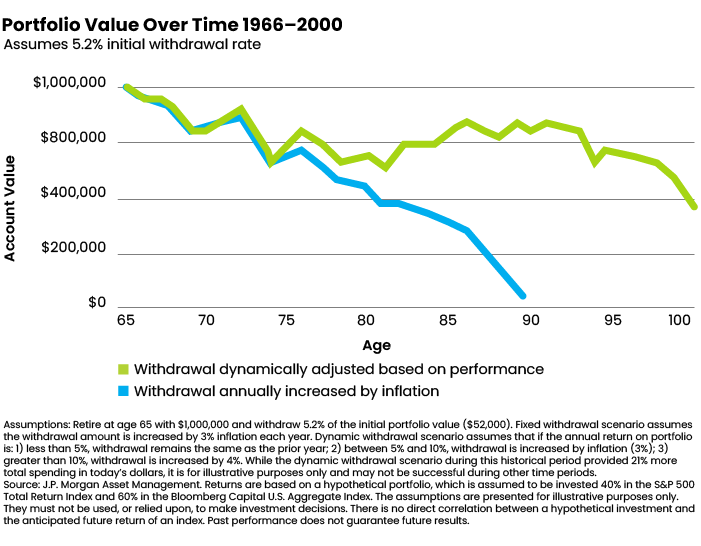

The 4% Withdrawal Rule

In 1994, William Bengen introduced the widely adopted 4% rule for withdrawing from a 50/50 (stocks/bonds) retirement portfolio that allows for inflation adjustments each year. Bengen’s research illustrates that clients should have a high probability of retirement success over a 30-year period leveraging the 4% rule. Notably, his research analyzes performance data from 1926-1976. The distribution strategy does not take into consideration asset location (and related tax implications), “longer” time horizons, and realized returns each year to determine client income.

Recently, there’s been much debate about the rule. Even Bengen himself is concerned how inflation will continue to affect the optimal withdrawal rate and keeps updating the rule. In December 2021, he said he updated it to 4.7% and that he hopes that holds. But according to an April 19, 2022, article in the Wall Street Journal, the father of the 4% rule now recommends a less aggressive withdrawal rate, at least until it’s more clear whether the current surge in prices will result in more long-lasting inflation. Bengen, a retired financial planner, says new retirees might want to start with a withdrawal rate around 4.4%.

With that said, here are two points to consider when determining a distribution strategy:

- Asset Location. Plan for taxes! The soon-to-be retiree may not have a ton of options to bucket their savings in taxable vs. tax-free accounts. Asset location provides your clients more flexibility in which bucket they take income from. In addition to the savings vehicle, having the right investments in the right account types is crucial. In a bear market, the idea of having to sell equities in an IRA to meet RMDs can very easily lead to a poor outcome.

- Dynamic Spending. Plans should adjust distributions based on both inflation and portfolio returns. As demonstrated in the method below, it’s important to maintain flexible spending habits based on the performance of one’s portfolio, not just inflation.

Correlation and Allocation to Low-Volatility Assets

Correlation and Allocation to Low-Volatility Assets

Harry Markowitz’s 1952 research on portfolio selection discusses how portfolio risk is not simply the sum of each individual component. It depends on how each component correlates and interacts with each other. This focus on correlation, along with allocations to low-volatility assets, are typically the headliner strategies to reduce sequence risk.

Each strategy below may fit into the correlation or low-volatility asset category, although they may not be right for all traditional wealth management clients:

- Heavy fixed-income allocations.

- Cash-reserve bucketing.

- Rental properties.

- Annuities.

- Cash-value life insurance.

- Tactical portfolio strategies.

- Home equity line of credit.

- Structured products.

Again, many of these strategies are not a fit for the average person because of liquidity issues, expenses, complexity, limited resources, etc. In fact, the most common method for reducing volatility and correlation goals is to increase bond exposure.

Increasing Allocation to Fixed Income

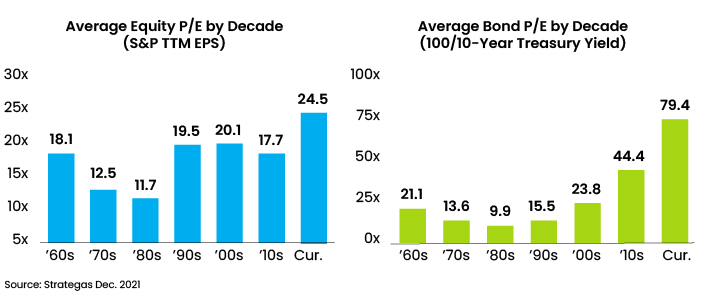

In a traditional portfolio, stocks can provide capital appreciation and dividends, while bonds have historically offered income and stability. However, if 2022’s markets thus far show us anything, the market environment we are walking into is potentially very different from what we experienced the last 30 to 40 years. For one, valuations remain at record highs. Just look at the price-to-earnings (P/E) ratio from both an equity and bondholder’s perspective. As illustrated in the chart below, average prices are the highest level in over 50 years.

In addition to high valuations, we are facing historically tight credit spreads, abysmally low interest rates and inflationary pressure with a less accommodative Fed. With these unique headwinds in the market, advisors need to start thinking differently about addressing risk for clients heading into retirement. Long story short, allocating to fixed income — an asset with low volatility at the expense of negative real returns — is not the solution for client portfolios.

Considering Market Volatility an Opportunity

“Risk isn’t what you think is going to happen, it’s what hurts if it does happen.” — David Dredge, Convex Strategies

Given the shortfalls in many strategies, how can we construct portfolios that find adequate return while keeping risk in line?

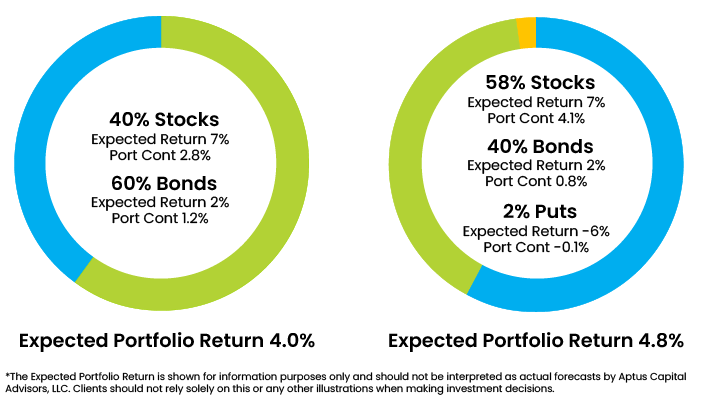

In our opinion, the most powerful lever we can pull to manage risk and maintain returns in today’s market is altering allocations away from bonds. This may seem counterintuitive to the conversation of how to manage risk, but we simply believe there is a better way.

Allocating to assets with correlation benefits is important but having 60% of your life savings in an asset class with minimal income today, a limited buoy based on the current rate environment, and no ability to grow just doesn’t make sense to us.

If you could allocate less than 5% to an asset (which we would argue has better correlation benefits and gives you the freedom to own more equites), would you consider it?

“Allocating to assets with correlation benefits is important but having 60% of your life savings in an asset class with minimal income today, a limited buoy based on the current rate environment, and no ability to grow just doesn’t make sense to us.”

The solution is to own volatility by having some downside protection. What do we mean by that? Owning index puts, VIX options, and even owning individual call options allow portfolios to have unique exposures to manage risk through negative markets. The good news about adding volatility as an asset class is that the natural convexity does not require a significant allocation for it to pay dividends to your clients. In other words, we think even having 2% to 3% in ownership of volatility can significantly impact the risk profile of your total portfolio.

Expected returns in a rising market will be negative for a traditional hedge, but the potential asymmetric payoff when a drawdown occurs is where you get your value. When investors expect stock prices to make a significant move – up or down – they typically purchase more options to protect themselves against those movements. In an environment where you expect a big near-term price drop, it is reasonable to expect demand to surge for put options, driving the price of those options up. This strategy gives you an additional asset class to mitigate sequence-of-return risk, while giving your clients the freedom to own more stocks to address any growth goals.

The Perfect Plan Concept

Andrew Lo and Stephen Forester’s recent book, “In Pursuit of the Perfect Portfolio,” includes profiles of some of the most prominent financial minds, including Harry Markowitz, Jack Bogle, Bob Shiller and Bill Sharpe. After talking to so many important financial leaders, the authors describe “the perfect portfolio” as one that will adapt to both individual changes in circumstances as well as to market conditions. In my mind, these comments could not be more accurate as you plan for sequence-of-return risk with your clients in today’s market.

The idea of being willing to adapt to the different market cycles is a huge tool to help with achieving adequate returns while not taking on risk your clients cannot handle. Options-based strategies can meet your clients’ return and risk challenges and do so in a fully-liquid, easy-to-implement manner. Full disclosure: All options strategies are not created equal.

The concept of the perfect portfolio translates to managing your distribution strategy as well. Adapt to modern studies such as Jonathan Guyton, William Klinger and Michael Kitces and remain flexible in your spending plan based on how your clients’ assets are growing. This makes a lot of sense in our book.

And remember to challenge the norm in this environment. Allocating 60% to an asset class that is battling hurricane-force winds is not the adaptation to markets that I think these prominent financial minds would envision as being the perfect way to address sequence-of-return risk.

James Yahoudy, CFP, is the director of Partnerships and Consulting at Aptus Capital Advisors, where he strategically works with advisors to support their investment offerings and related communication for clients. He has worked as a financial planner and with advisors since 2010.