Many women face financial and retirement stress from the gender pay gap, caregiving responsibilities, and long lives. But a fourth threat is discussed less often: chronic illnesses that disproportionately affect them.

Of course, U.S. women and men get many of the same diseases, with heart disease being the leading cause of death for both. Still, women are affected more often than men by debilitating autoimmune disorders and chronic diseases — including multiple sclerosis, lupus, migraines, depression and Alzheimer’s. In the U.S., 1 in 8 women develop breast cancer over their lifetime. Women also can face gynecological cancers and pregnancy complications that can trigger chronic conditions.

Yet women often fail to factor into their financial plans diseases they have or have a genetic predisposition for. Some feel uncomfortable discussing this with their advisors. And many advisors are unaware of the magnitude of the women’s health gap.

“When discussing the challenges in women’s health, a common rejoinder is that women, on average, live longer than men. But this neglects the fact that women spend 25% more of their lives in debilitating health,” states the recent report “Closing the Women’s Health Gap: A $1 Trillion Opportunity to Improve Lives and Economies.”

On average, women spend nine years in poor health, according to the report, published in January by the World Economic Forum in collaboration with the McKinsey Health Institute.

Narrowing the women’s health gap would reduce the time women spend in poor health by about two-thirds and allow 3.9 billion women to live “healthier, higher-quality lives,” the researchers found. It would also “allow at least $1 trillion to be pumped annually into economic productivity as a result of fewer early deaths and health conditions, extended economic and societal capacity to contribute, and increased productivity,” says the report.

A Dangerous Intersection

“Women are indeed more likely to face health issues that intersect with financial challenges,” Kaylee Ranck, PhD, director of college research for The American College of Financial Services, tells Rethinking65. These issues “often have direct and significant impacts on their financial stability and work capacity.”

“The cost of women leaving the workforce for a year due to health-related reasons extends far beyond the immediate loss of income and cost of health-related expenses,” she says. It can also reduce their Social Security benefits, pension or 401(k) accruals and employer matches, and compounding opportunities.

All of this is “exacerbating the gender retirement gap,” says Ranck, who is also affiliated with The American College Center for Women in Financial Services.

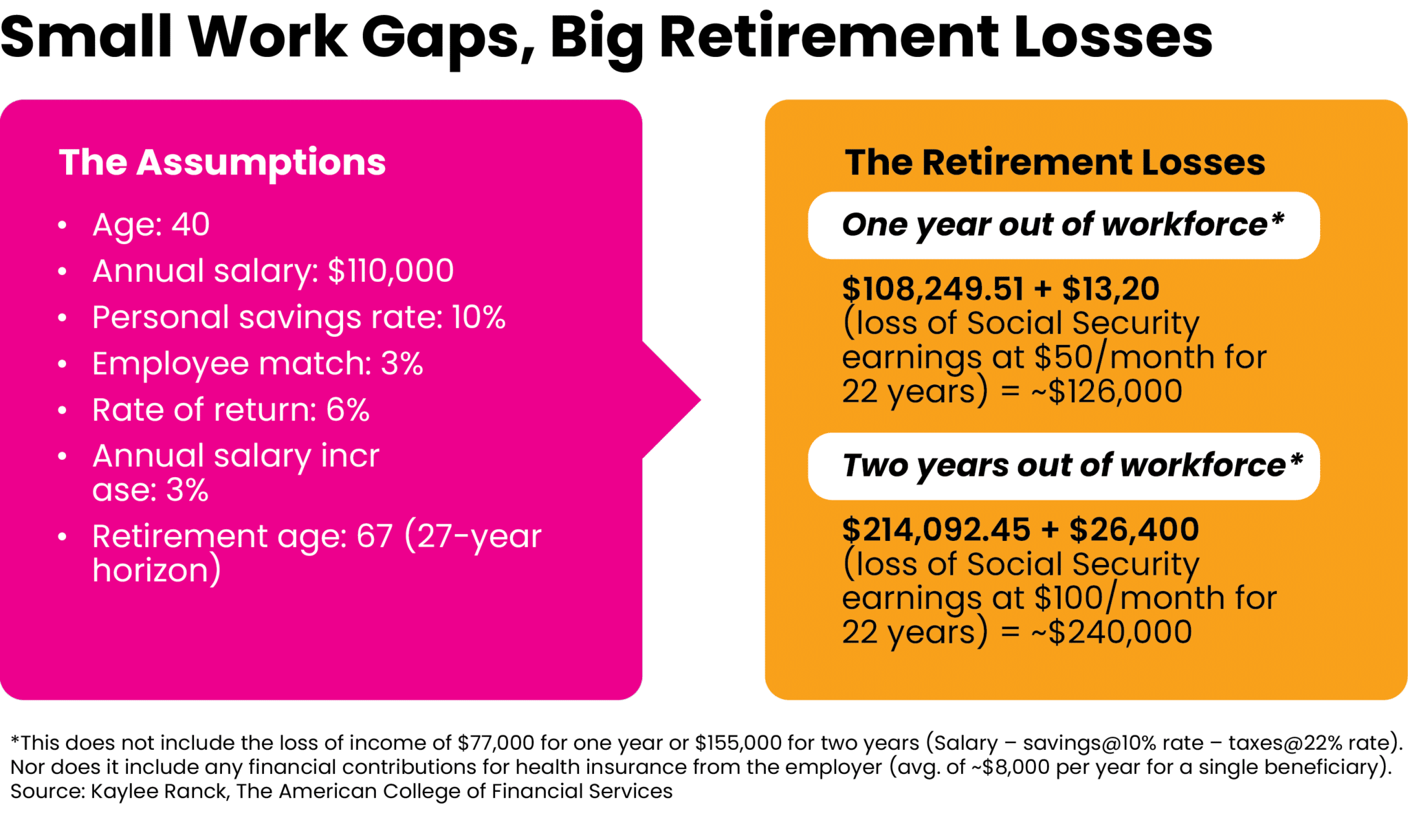

For example, let’s say a woman earning an annual salary of $110,000 and receiving a 3% employer match on a 401(k) plan takes a year off at age 40. Assuming her personal savings rate is 10% and investments compound at an annual 6% rate, this will result in a loss of $126,000 in retirement, Ranck says. If she takes two years off, that loss increases to $240,000. And this doesn’t even take into account her lost wages or her costs incurred from a lapse in employer-sponsored insurance. [See chart for more details.]

More Pain Points

Ranck notes that women are 80% more likely than men to be impoverished in retirement, partly due to career breaks for health issues or caregiving. They’re more likely than men to have a chronic health condition (38% vs. 30%), she says, citing data from the Kaiser Family Foundation. Autoimmune disorders [Ranck notes there are more than 80] are more prevalent in women and can be more debilitating for them, such as rheumatoid arthritis.

Chronic health conditions “often require long-term management and can lead to sporadic periods of ill health or flare-ups, necessitating time off work for medical appointments, treatment or rest,” says Ranck. Medication, healthcare services and assistive devices can be expensive, too.

“Depression and anxiety disorders, which are reported to be more prevalent in women, can lead to absenteeism or presenteeism (being present at work but operating at a lower capacity), directly affecting productivity and career progression,” says Ranck. Meanwhile, stigma about mental health may discourage some women from seeking available workplace accommodation or benefits that could mitigate their costs, she says.

Striking a Balance

While it’s impossible to eliminate many of the burdens accompanying medical problems, planning can help female clients manage them better, advisors tell us.

“Longer diseases can create more financial havoc,” says Karen Altfest, PhD, CFP, a principal advisor at Altfest Personal Wealth Management in New York City. “Yet we don’t always know the course of a disease, and many clients and spouses aren’t earning salaries by the time they contract a serious disease.”

Because of this, “it’s best to always prepare for what may happen someday, and more of my women clients are aware of that now than previously,” she says.

In addition to saving early, joining a retirement plan and doing tax planning, preparing also involves getting the proper insurance coverage, contributing to an emergency fund, and drawing up a will and other necessary estate documents, she says.

“[Genetic] tests can help you know what may be coming down the road (also what you may not have to worry about,” adds Altfest. “I hope they become more available to people.” Yet she also discourages overpreparing for a possible health bomb.

“One client has been telling me about a family disease she may get, for 20 years. As a result, she has become very cautious in her lifestyle choice,” says Altfest. Instead, “I believe you can be mindful of family medical history, yet live the life you want. If you need to slow down at some point, you will know when that becomes necessary.”

Good Planning is Diagnosis Agnostic

Altfest doesn’t give medical advice and “many clients don’t tell me what illness they have or how serious it is — just that they’ve been in the hospital and will be better soon,” she says. “However, finances don’t distinguish among diseases so financial advice doesn’t react more to one illness than another.” Good planning should help take the edge off most maladies.

Many of her clients have been able to work from home while recuperating from illnesses, thanks to the pandemic-induced changes in the workplace, she says. But not all clients are that lucky. One client who developed lupus in her 60s had always been the primary earner until she became ill, says Alfest. The client had also always managed her family’s finances and legal matters.

Now, “the family is taking it day-to-day. I have been in frequent contact with her husband and have helped him think through housing issues, retirement and investment choices (most if which interested his wife more),” says Altfest. “He fluctuates between planning a future with his wife (who is now in a coma) and expecting the worst.”

Fortunately, this woman has a long-term-care policy and received guidance from an attorney in her faraway state whom Altfest put her in touch with years ago.

When Alzheimer’s Comes Calling

Another one of Altfest’s clients, an older woman who had been living independently, developed dementia and could no longer be alone. “She had no family, but at my urging two years earlier had created a will, a power of attorney, and chosen an eventual executor,” says Altfest. “She would not have been able to do those things during her illness and might have had the court appoint a guardian for her.”

The client eventually needed a home-health aide, which her $200,000-plus annually and “her POA began to sell her personal effects to pay her costs,” says Altfest. But when her care needs increased and she needed two aides to live at home, that was financially prohibitive. Nor was her senior residence happy to have her remain there. Ultimately, “she spent her final months in a care facility (where she had said she did not want to go to),” said Altfest. But without planning, her final years could’ve been worse.

Financial advisors can also help educate clients about becoming part of the “sandwich” generation as their parents age [and encounter their own health issues], says Altfest.

Paying the Bills

Cary Carbonaro, CFP, director of the women and wealth division at ACM Wealth, says that the cost of healthcare in retirement can cost women $235,000 to $300,000. “We put a line item in the plan as future health. Sometimes you can earmark it to a health-savings account if they have one,” says the Florida-based advisor.

And sadly, sometimes the medical bills come way too soon in a client’s life.

Carbonaro helped a client with cancer liquidate her after-tax portfolio to raise cash for alternative medical treatments. “We just tried to do it in the most tax-efficient way,” she says. “Unfortunately, my client passed away at a young age, with young children.”

Carbonaro prefers to help clients figure out a way to use their current funds for medical expenses but she never tells them not to use their retirement accounts because “you can’t put a price tag on health,” she says. “I had a client once say to me, ‘I am fighting for my life.’”

Altfest sees borrowing from a retirement plan as “a bright red signal” that investors should avoid, even for health expenses. However, “if that is your only option, make sure it’s temporary,” she says. “Have a plan for repaying that loan so it doesn’t fall through the cracks.”

‘Be the CEO of Your Healthcare’

Carbonaro also encourages women with a family history of disease to “get tested and be the CEO of your healthcare,” she says. “This essentially means taking charge and optimizing your health and wellbeing.”

Some steps she suggests are learning about health-related topics such as nutrition, exercise and mental health; staying informed about the latest research and advancements in healthcare; developing a personalized health plan; scheduling regular health assessments, including screenings for diabetes, hypertension and cancer; maintaining health records to share with medical providers; making healthy lifestyle choices; being an advocate for oneself; and learning about insurance and its costs.

As for client dialogues, Carbonaro uses a low-key approach to get them to open up. “We just ask, ‘How is your health? How was your parent’s health?’” she says.

Stress Testing Unexpected Health Costs

Laura Knolle, MS, CFP, an advisor who works primarily with retirees and widows, builds out a financial plan with a client’s current circumstances and then stress tests it with Monte Carlo modeling. She includes unexpected health costs as one of the variables.

Knolle, of EP Wealth Advisors in Walnut Creek, Calif., has not worked with clients who went through their retirement savings quicker than expected because of illness. But when funds grow scarce, cutting back on discretionary spending, downsizing and using reverse mortgages to access equity in a home are options to consider, she says.

She also recommends reviewing the investment strategy of clients who fall ill. “If there is an increase in cost, it may be time to reduce risk and move to a portfolio that can potentially generate more income,” she says.

Knolle worked with a female client who battled cancer for many years. “Fortunately, with treatments, she was able to continue working until a normal retirement through starting Social Security at the earliest age (62) to help cover her increasing health costs and shorter life expectancy,” she says.

Buttoning Up the Paperwork

Knolle also encourages everyone to have an estate plan in place [including a will, health care directive and power of attorney] regardless of their present health. “Anything can happen at any time,” she says. She also encourages people to get their insurance in order early because after a diagnosis “you may not be insurable, or it becomes cost prohibitive,” she says.

She and her husband, in their mid-40s and mid 50s, respectively, have a hybrid long-term care policy they got when they were younger. “The long-term care portion will cover non-skilled care should one of us need it, with a death benefit to our beneficiaries if we do not use the coverage during our lifetimes,” she says. “As we also both work full time and have children, this policy will allow us pay for outside help versus adding more to our plates and depleting our personal funds” should either spouse pass.

Medicare Considerations

Women [or men] with chronic illnesses need to tread especially carefully when retirement and Medicare are on the horizon, says Joanne Giardini-Russell, owner of Michigan-based Giardini Medicare.

For example, a 65-year-old with lupus and great employer-sponsored insurance doesn’t have to start Medicare, she says. Or if a wife is younger than her husband who is retiring and starting Medicare, she should check if it makes sense to stay on his work plan through Cobra or go to the health insurance marketplace, which can’t deny preexisting conditions, says Giardini-Russell.

She also notes that insurance companies can’t refuse to sell a beneficiary supplemental (Medigap) coverage for a pre-existing condition within six months after signing up for Medicare Part B.

“It’s not super rocket science,” she says, but you have to crunch numbers and meet deadlines.

Varying Impacts

Chronic conditions and other diseases can impact women of all ages — and each stage carries a set of unique problems.

“Younger women may have more time to recover lost earnings and retirement savings, but they also face the challenge of re-establishing their career trajectory,” says Ranck. “Middle-aged women might struggle more with re-entry into the workforce due to age discrimination and skill gaps.” And if early retirement is triggered by health issues, “women may endure a longer period of retirement with a diminished financial cushion,” she says.

Ranck encourages women who’ve had to leave work and want to return to check out career reentry programs. [One source of information is the nonprofit Path Forward.]

Women and their advisors or trusted health insurance brokers should closely review their health benefits and consider whether they need supplemental health coverage, such as critical illness insurance, she says. “Financial advisors should emphasize the importance of obtaining adequate disability coverage, which can provide a continuous stream of income if a woman is unable to work for an extended period,” she adds.

Giardini-Russell notes that women with very short work histories, due to illness or other reasons, may not qualify for Medicare on their own. For example, an unmarried 40-year-old with multiple sclerosis may need to file for coverage on a former spouse’s record if she didn’t work for at least 10 years, she says.

Nest-Egg Opportunity

Ranck encourages all women to take advantage of health savings accounts (HSAs), which allow accountholders to save pre-tax dollars to pay for qualified medical expenses. HSAs “can be particularly advantageous for women, who typically face higher health-related expenses throughout their lives, including regular medical screenings, potential maternity costs, and a longer lifespan that often leads to higher cumulative healthcare costs,” she says.

Unlike with flexible spending accounts (FSAs), unspent funds in HSAs can be rolled over year to year, “making them a strategic tool for building a nest egg for healthcare costs in retirement,” says Ranck. This “not only empowers women to manage their health expenses with pre-tax dollars but also encourages them to be proactive about their health and wellness.”

Not for Women Only

Male advisors also need to be talking about women’s health issues. When Zac Beckerley, CFP, a wealth advisor with Merit Financial Advisors in Frisco, Texas, meets with new clients, he asks if there are any health issues that he needs to be aware about for planning purposes. Typically, he plans for 95-year lives unless a client has a big health issue.

Establishing trusted client-advisor relationships makes personal health conversations easier, regardless of the genders of the advisor and client. When one of Beckerley’s recently divorced clients was diagnosed with cancer, “She called me and said, ‘This is what’s going on,’” he says. “Her mindset changed” and she was more interested in understanding her finances.

The client wanted to make sure her accounts are in order and to know how her money will transfer to her adult children, some of whom she is helping support, if she becomes incapacitated, he says. She made one of her children her power of attorney.

Closing the Gap

We also asked advisors what the government and the medical community should do to better serve women’s health needs.

“Washington can try to bring costs down. Biden has done some of that in drug costs and plans to do more. Obamacare helps many people cover medical costs as well,” says Altfest. “I believe inexpensive tests would be helpful too.”

Knolle would like to see more financial literacy efforts to prepare people for rainy days. “This will ultimately prevent a lot of stress and potentially running out of assets and relying on government programs such as Medicaid,” she says.

The World Economic Forum and McKinsey report outlines what it’ll take to close the women’s health gap and capture that $1 trillion opportunity:

Stepping up women-centric research to fill gaps in under-researched and often undiagnosed conditions and diseases that affect women differently.

Strengthening data collection concerning women’s health burdens and the impact of interventions.

Increasing women-specific care, from prevention to treatment.

Creating incentives for investment in women’s health innovation and developing new financing models.

Implementing policies to support women’s health, at academic institutions and in workplaces.

To truly realize female clients’ needs, advisors must understand what’s missing from women’s healthcare. Although there is much work to be done as the population ages, Altfest remains upbeat: “Each year we have a good handful of healthy people in their nineties as clients.”

Jerilyn Klein is the editorial director of Rethinking65.