No one should be surprised at the rising inflation we’re seeing. History supports what has led to our current state of affairs: low interest rates, stimulus money with no offsetting increase in production, and labor shortages, to name a few. But for many advisory clients, inflation isn’t causing quite as much of a drag as many think.

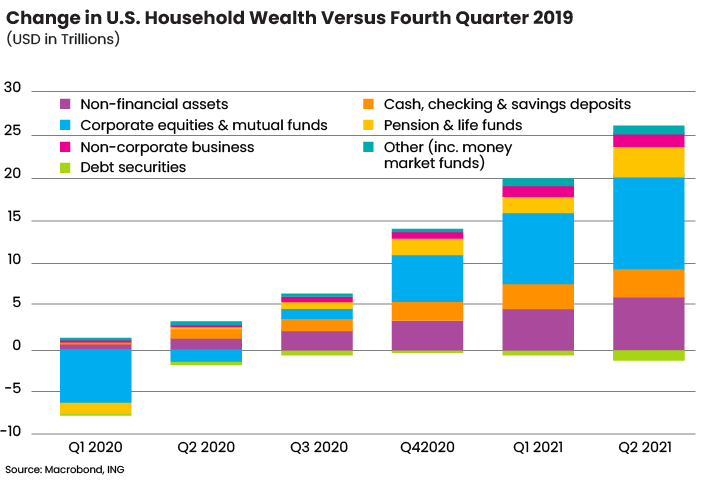

Although the COVID-19 pandemic has caused personal and economic devastation, U.S. household wealth has ballooned by nearly $30 trillion since the end of 2019 (see figure below). Consumers are the driving force of the global economy, and U.S. household balance sheets are uncharacteristically strong following several years of portfolio asset appreciation, lower costs, and stimulus checks.

Not surprisingly, higher income and already wealthy households experienced most of the increases in wealth since they were already heavily invested in the winning asset classes. Corporate equities and mutual funds were the biggest contributors to the gains since they surged after unprecedented Federal Reserve and government stimulus. Pension and life insurance funds benefited for the same reasons while the value of debt securities fell.

But even if the higher prices your clients are paying for meat at the grocery store or gasoline at the pump are putting only a small dent in their budgets, everything feels much more expensive. Relatively minor price increases could still be a major blow to their psyches in the face of the pandemic.

For clients on a fixed income, even small increases can seem particularly onerous. Unless they sell their home at the top of the market and move somewhere cheaper, they aren’t getting a larger paycheck (aside from the most recent Social Security increase).

Standing in line at the store today, the gentleman behind me shared a sad personal story. Right before the pandemic, he and his partner purchased an art gallery store. With 18 months of virtually zero clientele, he was forced to sell almost everything he had to stay afloat: including using his retirement savings. The gallery was eventually forced to close, and now he stores the contents in one room of a mobile home. Fine art is simply not one of those necessities in high demand right now.

Helping Clients Adjust

A rising income sounds like a nice thing to have, but in reality, it’s more of a must-have with inflation chipping away at consumers’ spending power. Real inflation is here, and it’s anyone’s guess how long it will stick around. As financial advisors, we need to consider ways to make sure our clients’ financial plans meet their needs and, if not, consider making necessary adjustments to ensure that their spending power lasts. If we’re paying attention instead of being complacent, we should only have to tweak rather than redo a plan.

Most of the inflation pressure has been driven by subcategories associated with the reopening of the economy (such as fuel and energy) and those affected by supply chain problems (such as autos and consumer staples). If you have built your clients’ long-term plan assumptions slightly above the Fed’s target rate of inflation (2%), the plan should be able to weather the expansion and contraction of a normal business cycle. A conservative approach would be to increase the potential cost of healthcare and education by a higher percentage.

Because inflation causes money to lose value over time, hedging against it is an important part of any sound investment strategy. Continuing to recommend your clients stick with a diversified portfolio with a variety of asset types will help offset inflation and ensure that the overall growth of the portfolio can outpace the pressure in the long term.

Getting Back to the Basics

Many Americans may not recall how high gas prices were between 2008 and 2014. It was during that time that consumers decided to modify their behaviors. Instead of leaving the house three times a day, making various stops at the store, dropping children off at school, and heading back out for sporting events, they strategically planned how one might accomplish all they needed with just one trip. Even if it meant sitting in the car until it was time for the next event.

That may be what is necessary once again. Taking a closer look at where our money is going and how we can stretch the almighty dollar never hurts. Here are some short-term ideas and good talking points that you can also suggest to clients so they feel there are things they can do immediately to take control and have more money in their pockets.

Mortgage refinancing is still up for grabs if one has not already done so (maybe due to unemployment at the time or the debt-to-equity ratio was too high).

Get back to carpooling, especially with the strain of the public transportation and school bus driver labor shortage. Carpooling can also save money on gas.

Consider downloading that grocery app for special deals and frequent buyer coupons.

Re-evaluate the tax withholdings on your income to make sure you are not over withholding and allowing the government to use your money tax free.

Tap into those health savings accounts to provide some temporary relief.

Evaluate the costs of your credit cards.

Cut down on those multiple streaming services by choosing the one that you most frequently use.

As history continues to repeat itself, the supply and demand imbalances will eventually work themselves out and the rate of inflation will level off. Innovation has for decades been a considerable deflationary force and this time is no different. Although the post-pandemic surge in pent-up demand for goods may be behind us, higher levels of U.S. household wealth and income will continue to provide significant support to the economy.

In the past, what mattered most was not what the economy or the markets did, but what you and your clients did. When acting on a long-term plan rather than reacting to current events, positive outcomes followed. For now, we need to assess where inflation hurts the most and develop a way for our clients who are suffering to fight back.

Catherine M. Seeber, CFP, CeFT, is passionate about blending both financial and nonfinancial needs and desires of her clients to make the most of their resources, time, talent and energy as they transition through life. Cathy is a vice president and financial advisor with CAPTRUST.