Real estate represents an estimated 30% of this country’s wealth. Yet few financial advisors are comfortable offering the level of analysis and advice on directly held real estate that they offer on investments, taxes and other financial matters. If your work is comprehensive, then directly held real estate investments probably deserve more attention in your advice model. It follows that investment properties are the forgotten asset class in financial services.

The absence of real estate at the financial planning table is a sizable advice gap, but it is understandable. Real estate is not part of the securities or licensing curriculum. The coursework and experience needed to earn a CFP,CIMA or any other financial advisor credential don’t provide any real estate fundamentals, including cash flow and risk management exposure. And nobody seems to notice the absence.

As a CFP and long-time instructor of investment real estate courses for financial professionals, I know many advisors are interested in learning how this asset class works. Through my columns in Rethinking65,, I hope to increase your exposure and interest in helping clients with their questions about investment real estate. My goal is to help you better understand this asset class so you can recognize opportunities and issues that may require input from other experts.

You will find many similarities between giving real estate advice and other kinds of planning advice. It’s largely about understanding a client’s needs and goals.

Income as a Driver

Among the top questions I hear from clients and other financial advisors about existing rental property are, “How can I tell if my property is performing well? Should I keep it or do something different?” Assessing performance and reviewing options can seem like dependent questions. More likely, the performance outcome would trigger a need to review options. Let’s tackle performance now and cover buy-keep-sell possibilities at a later time.

In order to respond to those questions, we need to add structure and make a few assumptions. Let’s assume the client is entering or already in retirement, because Rethinking 65 readers tend to seek greater insight in serving this demographic. Let’s call retirement “financial independence” since it seems to capture the spirit of today’s retirees better.

Let’s also assume that because this is the phase where wealth accumulation winds down and wealth preservation begins, the client wants income from the rental property. Understanding that income is driving the client’s investment goals allows us to put aside other performance measurements such as appreciation. So for now, strategies including buying and holding for growth, land banking and flipping houses matter less.

Tackling the Math

The next question in measuring performance is more complicated because it can get subjective to investors. It’s also a bit of a black box to advisors: How much income should a client expect? Clients generally view this as dollars. Advisors should view this as a percentage of income from equity. Finding the answer to this question can be tricky because it involves managing emotion, performance, and many times, need.

The art and science of this conversation are suitable for a future article. For now, let’s make it simple and assume the client and advisor agree that 7% is a good target income rate. Appreciation may add another 2% to 3% in total annual return.

Let’s make the following assumptions about the client’s existing rental property:

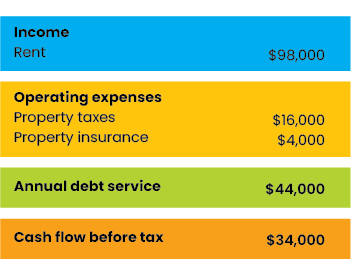

It’s a four-plex in Oakland, Calif., with a current estimated market value of $1,100,000.

It has a $550,000 mortgage, 5.00% interest. Principal and interest payments are amortized over 30 years.

The potential annual rental income is $98,000.

Key Points

Before I begin to lose you with some of these assumptions, let’s cover some important facts:

Mortgage rates on an investment property (non-owner occupied) are higher than the current published rate. And for some property types, the difference can be even greater.

Longer-term loans are recommended today for a long-term real estate hold. That will change as interest rates increase. In addition, for larger commercial properties, 30-year amortization is not available.

The property used for this illustration is like hundreds of other existing client properties we have modeled for cash flow around the country. I rounded the numbers in this exercise to make this more digestible. The difference in outcome by rounding is negligible.

Cash-Flow Basics

Although the analysis seems thin, the formula most clients use to evaluate a rental property is total income minus debt and property taxes, and maybe minus property insurance. It certainly cannot be called “crunching the numbers,” although that is what many intend to do. The rationale appears to be, “I might be missing some numbers. But it can’t be much more.”

If we took this lead, the cash flow expected from this property is as follows.

Many clients, and some advisors, see the $34,000 of positive cash flow and might call this a success. In their minds, this is almost $3,000 per month, free and clear.

When you consider that it takes $550,000 in equity to generate $34,000 in income, you get a better perspective on the capital needed to generate this income. Viewed as yield rather than dollars, it is 6.2% ($34,000/$550,000). When compared to the 7% target yield, it’s close. Your client will remind you about appreciation, which is fair. Although a client cannot pay monthly bills with appreciation, adding 2.0% to 3.0% in appreciation (a 60-year average range) does get the total return to 9.0% to 10.0%.

Putting aside, for now, risks unique to smaller rental properties, the discussion might be over if this math accounts for all the rental property expenses. And in fact, this is where most discussions about directly held real estate investments with clients — and even some advisors — end. The next step is typically to put these numbers into the plan. But wait!

Often-Forgotten Expenses

Just as directly held real estate investments are the forgotten asset class of financial advice, capturing operating expenses in rental property is the forgotten step of a good real estate cash-flow model.

The following expenses are often forgotten in evaluating real estate investments, so let’s assume that’s the case in our four-plex example:

Management fees.

Annual repair and maintenance.

Gardening, pool.

Accounting and legal.

Advertising and leasing.

Maintenance reserve for capital repairs and improvements.

Vacancy, credit loss or concessions.

Many clients find it annoying to consider these expenses; they don’t generally hit their radar. Non-recurring expenses are paid out of pocket and, except for tax prep, aren’t considered in total return. And after the property is purchased, few clients look back at actual income and expenses.

In addition, clients feel they can manage their property or do repairs themselves. Many opt to use internet directories to find and qualify tenants. They also think that recruiting honest, well-intended clients will eliminate their need for legal help.

You see where this is going. These feelings are not realistic.

Remember that we are working with clients who seek financial independence. Spending the balance of their lives with family, traveling, gardening, reading and volunteering is inconsistent with being called to fix toilets, replace fixtures and collect rents. The reality is, at this age, most clients are interested in becoming more passive with their real estate rather than stepping into more responsibility.

If we add the forgotten operating expenses, the cash flow from the four-plex looks like this.

Income of $3,500 before taxes per year is much less reassuring than the $34,000 from the earlier calculation. The yield from the investment capital is 0.60%, an estimated outcome that is inferior to other uses for this equity. Therefore, the Oakland rental property did not meet the client’s expectations.

Some Final Thoughts

Let’s circle back to the original question, “How can I tell if my property is performing well and should I keep it or do something different?” If your client is concerned with income performance and contribution to financial independence, then the property should be owned for cash flow rather than appreciation or personal investor needs.

There is a lot more to discuss about cash flow, and I will do so in an upcoming column. When good cash flow is combined with tax-advantaged income, directly held real estate can be among your clients’ most effective approaches to retirement income.

In the meantime, I invite you to think more about how you currently help clients with their interests in real estate and how you might be able to expand your value proposition. And let Rethinking65 know what you would like to see covered in a future column.

Rich Arzaga, CFP, CCIM, is the Founder and President of The Real Estate Whisperer Financial Education and Coaching. He is a long-time, honored instructor in the UC Berkeley Personal Financial Planning program. He teaches Real Estate Investments for Financial Planners (15 hours of CFP CE) and Insurance for Financial Planners. For questions or suggestions on future articles, contact Rich at linkedin.com/in/richarzaga/.