“The avoidance of taxes is the only intellectual pursuit that carries any reward,” said economist John Maynard Keynes.

As we begin another tax filing season, clients will certainly be looking for ways to avoid their tax obligations by legally reducing them. While clients may have some options to do so for the prior year, now is also the perfect time to start thinking about how to save for the current year.

One topic that clients may consider in their planning for 2022 is the concept of scholarship tax credits. Scholarship tax credit programs are becoming more widely available and as of March 2021, 19 states had a program in place with the intent to allow taxpayers to contribute amounts to organizations that provide scholarships to students from kindergarten to high school. Since then, Ohio has also added a plan.

In some cases, these contributions are deductions from the state return and in other cases they are credits. Credits are more valuable than deductions because they are a dollar-for-dollar reduction of the tax due. Deductions reduce income before the tax due is computed. To take advantage of these credits or deductions, a client needs to contribute to the plan of their state of residence.

How Scholarship Tax Credits Work

Scholarship tax credit programs are designed to allow a taxpayer to direct a portion of their owed state taxes to a scholarship-granting organization. For example, if a client has a state tax bill of $10,000, a credit of $1,000 would reduce this to $9,000 due to the state and the remaining $1,000 would be sent to the scholarship-granting organization. These programs may have a place in your clients’ giving plans if they are looking to redirect a portion of their current giving or are looking for additional giving options.

A key point to bring up regarding these plans is that the client has no input on the school district or students that will benefit from their donation because the funds are given directly to the scholarship granting organization. In all the participating states, the scholarship recipients can use the money for public schools and several states also allow the funds to be applied to private schools.

Arizona launched the first scholarship tax credit program in 1997. More states have rolled out programs in their quest for alternative methods to fund the ever-rising cost of education.

For those wondering about how these programs would fare under judicial review, take heart. The Arizona plan was ruled constitutional by the United States Supreme Court on April 4, 2011, in Arizona Christian School Tuition Organization v. Winn.

A Generous Plan

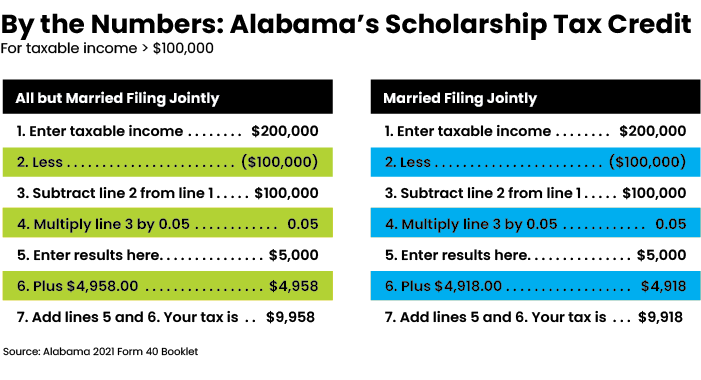

Alabama’s scholarship tax plan, one of the most generous, allows for a credit up to the lesser of $50,000.00 or 50% of the tax liability per return.

As an example, a married couple living in Alabama with a taxable income of $200,000 expects to owe $9,918 in taxes. Qualifying for this credit would allow them to direct $4,959 to a scholarship-granting organization.

Ohio’s plan allows for a $750.00 credit ($1,500.00 for a joint return)] Although it is not as generous as Alabama’s scholarship tax credit program, we are introducing this to our clients in 2022.

Getting Started

As a first step, clients should work with their tax preparers to determine what if any state liability they are likely to have in 2022. The educational tax credit or deduction will not have a financial benefit for clients without a corresponding state amount due. Since these tax benefits are recognized on a calendar year basis, the opportunity to do this for 2021 has passed, but it’s never too early to start looking at the current tax year. The process to claim the credit or deduction will depend on the state but is typically done by making an election on the state tax return.

Alabama taxpayers must first request permission online to claim the tax credit. Taxpayers must register to set up an account at My Alabama Taxes for approval, follow a short series of steps to reserve their credit, and provide supporting documentation for certain credits.

On the other hand, Ohio only requires that the election be made on the return. Of course, documentation should be maintained that the donation was properly completed to an eligible organization To qualify for this credit, you must make a monetary donation to an eligible scholarship granting organization (SGO). The credit equals the lesser of $750 or the total amount you donated to SGOs during the tax year.

Taking the time to get proactive about tax planning is certain to pay dividends now and in future years. Even if this is not a fit for a particular client, the discussion may provide greater insight into the philanthropic causes that are important to them.

John M. Gehri, CFP, ChFC is an advisor with Harvest Financial Advisors in the Cincinnati/West Chester, Ohio area. John may be reached at john@harvestadvisors.com. This article is for informational purposes only. Any commentary and third-party sources are believed to be reliable but Harvest Financial Advisors cannot guarantee their accuracy.