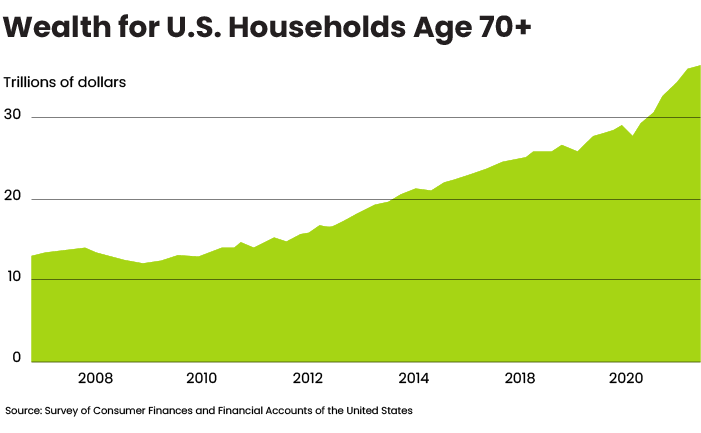

People are living longer today and, according to Federal Reserve data, baby boomers age 70-plus have more than $35 trillion in assets. If your practice is focused on a small number of clients with substantial levels of assets, you likely have many clients who are older. Many see the benefits of working with financial advisors. How can you help them besides the standard ways you help all your clients?

You want to develop a strong bond and become their trusted advisor, not just a service provider. Assuming you have clients in their 70s and older, there are many ways you can strengthen the relationship. Some might sound like stereotypes about older people, but these strategies make an impact.

Here are 15 suggestions:

Know their preferred communication channel. This is important for all clients. Older clients generally are very comfortable with the phone. Email and surface mail too. Find the channel that gets the fastest response. It’s often the phone.

Call them often. It’s been said that people equate good service with six or more interactions annually. Try for at least monthly contacts. Always have something to say. If the market is volatile, calm them.

Focus on the long term. We are all going to die at some point in time. On the plus side, I like observing that the human body is one of the only things on Earth that can run for 100-plus years on its original parts! Except in certain situations, as long as their mind is intact, they can keep going for a long time. Relatives might be hinting they should throw things out, downsize and prepare to exit. Not you! Let’s assume they will be around a long time until someone tells them otherwise.

Explain things simply. We speak in financial jargon. We assume everyone understands it. They don’t. People also forget. I liked to use the strategy, “I realize you know how municipal bonds work, but since we are talking about one, let’s review the details…” They might say, “Yes, I know, but I appreciate the recap.”

Paper thank you notes. Previous generations wrote thank you notes. They were taught from an early age. Your parents might have taught you. If your clients have you over for dinner, send them a thank you note. It’s a sign of respect. Here’s an unexpected opportunity: If they refer a friend, send them a note thanking them for the introduction. (No need to mention if they became a client.) Your strategy is simple: If you reward behavior, it gets repeated.

They like paper statements. Maybe paper confirms too. It helps the environment to do all reporting online, yet, for many of them, “Out of sight means out of mind.” They should at least review their monthly statement in printed form. Imagine if the market hits an air pocket. If they didn’t get a printed statement, you didn’t call them and they weren’t in the habit of accessing their accounts online, you can imagine the blame game that would follow.

Send birthday and anniversary cards. They like getting mail. They grumble that their nieces and nephews don’t send thank you notes when they send checks. Their own kids sometimes forget to call. If you remember, it makes a big impact.

Listen. When you call, try not to only allocate a couple of minutes for the call. Many older people like to talk. Draw them out. What are their fears, worries and concerns? Some older people are terrified they will run out of money, even if their present assets could last them several lifetimes. When you know their concerns, you can reassure them.

Talk about bargains. They love them. Regardless of wealth, they want to save money. Because their parents or grandparents lived during the Great Depression, they were taught thrift at an early age. They love to get a good deal. Pass along ones you have found.

Encourage them to get out. Remember the pandemic lockdown? We were told to stay at home except to buy groceries or visit the pharmacy. Well, many older people live that way 365 days a year. They should be attending religious services, seeing friends, eating out and planning vacations. They shouldn’t be sitting at home (sometimes in the dark) just watching TV.

Meet over meals. You periodically review their portfolio with them. Make it an event. Go out for lunch or dinner. Many older people cook less and less at home, preferring to dine out. It’s an enjoyable activity for them. Friends have told us that “the kitchen is for resale purposes only.”

Suggest vacations. Baby boomers are the target market for the travel industry. Cruise lines are used to hosting people with limited mobility. Passengers still have a great time. They see new faces and make new friends. Assuming they can afford it, encourage them to plan vacations. It gives them something to look forward to, even if they can’t travel right now with Covid concerns and restrictions.

Meet their children. These are also known as heirs. Although they might be waiting for a windfall, they often don’t want the responsibilities of looking after their parents. They may see the valuable service you are providing, being a primary point of contact. They will sense your concern. Knowing the children should also help retain the assets (or some) when the heirs eventually inherit.

Look for changes in behavior. Have they become withdrawn? Are they losing interest? Not telling jokes anymore? Staying home all the time? Wearing the same clothing? You are limited in what you can do, but try drawing them back into the real world, reconnect with their children or seek medical attention.

Are they missing? Your greatest fear is you can’t reach them. There might be a logical reason they are off the radar for a day or two. They might be staying over with their children. But if they are missing for a longer period, be concerned. While respecting confidentiality, many firms have a procedure in place where it’s OK for the advisor to call trusted preidentified contacts to ask about the client’s whereabouts. Stopping by and knocking on their door is another strategy after you’ve tried the primary communication channels.

Although these strategies reference older clients, many also apply to clients regardless of age. You are treating clients as people. You are showing you care about them and are investing in the relationship.

Bryce Sanders is president of Perceptive Business Solutions Inc. He provides HNW client acquisition training for the financial services industry. His book, “Captivating the Wealthy Investor,” is available on Amazon.