Editor’s note: This is the author’s fifth article in asix-part seriesfor Rethinking65 on working with widows.

Laura Mattia

The third stage in a widow’s financial journey is called the passage or growth stage. In this phase, the widow adjusts to new conditions, designs her new life and explores possibilities. The widow is beginning to find joy in her life again. She is adjusting to her new situation.

While she will continue to grieve, her cognitive functions are returning and she is better prepared to make lasting decisions. It is now time to begin having more in-depth discussions about her finances and address the items she had identified on her Now, Next, Later roadmap for Later.

Selling the House

Often a top-of-mind question is whether to sell the house. She is now in a better mindset to make this decision. Some widows feel a move could provide an easier path to creating a new life. Others want to move closer to their children or grandchildren. Still, others are afraid to move because they fear more change.

It could be helpful to explore her feelings associated with selling the house to ensure this option has been thoroughly examined. Assuming the move seems appropriate, there are a few areas where you can help.

To start, you can help her obtain a clear title in her name by officially transferring his interest. Most couples own their house, joint tenancy, and although the title automatically transfers to the surviving spouse, filing an affidavit with an original copy of the death certificate will ensure a smooth sales process.

Additionally, you can help calculate the proceeds from the anticipated sale. She will need to know what to expect as she contemplates how much to spend on a future home. Costs to be subtracted from the sale price include real estate agent fees, cost of staging the home, repairs to sell the house, seller concessions, closing costs, paying off the mortgage and capital gains taxes.

Capital gains are generally recognized when a sale from a property is above the purchase price plus improvements, but exceptions apply. Whether she will pay capital gains taxes depends upon how much she can exclude and whether she will receive a partial or full (if they reside in a community-property state) step-up in the basis of the property at the time of death.

Exclusion Amount

If there are significant gains embedded in the house, the widow may be able to exclude $500,000 of home-sale profits from taxes if she sells the house within two years of her spouse’s death. Additional eligibility requirements include that she is not remarried at the time of sale and neither she nor her late spouse took the exclusion on another home sold less than two years before the sale. She also must meet the two-year ownership and residence requirements (including her late spouse’s times of ownership and residence). If more than two years have passed since her spouse died, no more than $250,000 of the profit is tax-free.

Step-up

However, the taxable gain may be smaller than the widow might think since the husband’s share of the property is stepped-up to the date-of-death value. In community property states, the surviving spouse enjoys a step-up in basis to both ownership portions of the property, so a surviving spouse will not incur any capital gains taxes if she decides to sell. Here’s an example of how that would work:

Florida residents Sally and John purchased a house 10 years ago for $500,000. After John passes away, Sally decides she would like to sell the house. For simplicity, we won’t include any other costs. On the date of John’s death, the home was worth $1 million. The new basis for Sally is half of the original basis plus half of the home’s value at the date of death, which totals $750,000. Even if Sally doesn’t sell the house until year three, when she no longer qualifies for the couple’s exclusion, she will owe no tax because the single’s exclusion covers the entire gain of $250,000.

As a widow’s advisor, it is essential to know that the step-up applies to other inherited property such as financial assets where the surviving spouse receives a step-up in basis. She may not understand the nuance of the decisions impacting her tax liability, so you, her trusted advisor, can help her understand the tax consequences of selling property and the timing of the sale.

Federal Taxes

While capital gains taxes related to selling the house require consideration, other tax issues should also be discussed. For example, she may need your help understanding how she will file her tax return. Marital status is determined on the last day of the tax year (Dec. 31), but the married filing jointly status can be used even if the date of death was Jan. 1.

For the following two years, she may be allowed to use the “qualified widow” status, entitling her to the same tax rates and standard deductions as the married filing jointly category. To qualify, she must remain unmarried; pay more than half the cost of keeping up a home; and claim a child, stepchild or adopted child as her dependent. After two years, she may file as head of household, but this is not as beneficial as the qualified widow status.

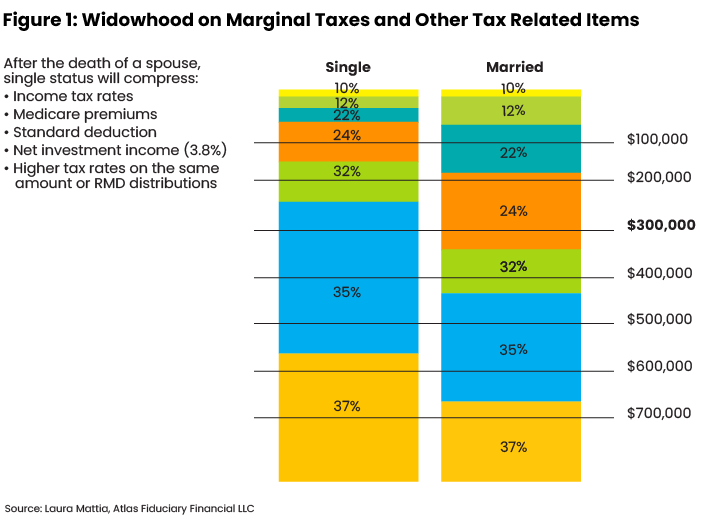

Once she no longer qualifies for special filing, the single status may result in a higher tax rate, a loss of certain tax breaks and a smaller standard deduction. Figure 1 shows how a married filing jointly couple with taxable income of $300,000 would move from a 24% marginal tax bracket to a 35% marginal tax bracket after a surviving spouse is required to file single.

These changes can also impact the amount she will be charged for Medicare Part B and Part D (IRMAA) and even affect her Social Security benefits tax. While you can help her take advantage of the allowances created to ease the tax burden for widows, some widows are not eligible for qualifying widow or head of household categories. Instead, you may want to prepare her by explaining how her new single status will affect her tax situation.

Social Security

Let’s look at a second example:

Hank passed away last year, and now Margie, as the surviving spouse, is required to file single tax status. Before Hank’s death, Hank and Margie filed using married filing jointly status each year. Between their Social Security benefits and Hank’s pension, their AGI was $103,800, and they were in the 12% marginal tax bracket (see table below). Margie is now receiving Hank’s Social Security. Fortunately, Hank had selected 100% joint and survivor for his pension payout, but without the second Social Security check, her AGI has gone down by 33% to $69,800. Her household expenses did not decline 33%, so she is now finding making ends meet more difficult. She was also surprised to find that her marginal tax bracket has increased to 22% even though her income has gone down.

Rolling Over His 401(k)

While it is tempting to roll the deceased spouse’s 401(k) to your client’s IRA, it might not be what is in her best interest. If she is younger than 59½ and could potentially need access to the money, she might want to leave the money in the plan so she can take withdrawals when needed without an early 10% penalty, although she still will pay ordinary income taxes.

If the plan has low-cost and diverse options, this could be the best strategy. But if the 401(k) plan is inferior, she could establish an inherited IRA, allowing withdrawals without the penalty for accessing the money early. However, if you are confident she will not need access to the funds or she is older than 59½, she could roll the money into her own IRA. Doing this will allow her to take required minimum distributions (RMDs) based upon her age, maximizing tax-deferred growth potential. Sometimes the best overall solution is not obvious, so you can help her think this through.

Update Assets

As you help your widowed client organize her assets, determine what titling and beneficiaries need to be changed. If you have not already done so, work with your client to create a list of all financial institutions and investment management firms holding accounts solely in her name, solely in her late spouse’s name, and in joint accounts so she can call and have the deceased spouse’s name removed. In most states, joint accounts are considered rights of survivorship, so this should not be an issue.

All the work discussed in this article and the previous four articles is essential to progress her to and through the passage/growth stage, so she is prepared for transformation into the new normal. The goal is for her to put her finances in order so she can envision her future with clarity. Only then will it make sense to create a complete comprehensive financial plan.

Laura Mattia Ph.D., MBA, CFP, is the CEO and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla. [HYPERLINK Atlas Fiduciary Financial LLC: https://atlasfiduciary.com/]