[Editor’s Note: This is the author’s first article in a six-part series for Rethinking65 on working with widows.]

The death of a spouse is one of the most stressful events one can experience in life. Widowhood is such an intense transitional experience that widows need strong support. But often, married friends become distant, other friends are uncomfortable, and family members live far away, leaving the widow alone and solely responsible for all financial matters. At the same time, studies show that stress can impact a widow’s confidence and overall decision-making, intensifying the financial pressures associated with this traumatic event.

Even without stress, some women may not be fully prepared to make financial decisions. Despite the many achievements women can be proud of, women are often not as confident and secure about money.

In fact, research shows women tend to be less knowledgeable and less confident with money than men. Perhaps this is because many women do not participate in household financial decision-making even when couples verbally commit to both being involved. Household decisions on retirement age, where to live and how much to spend on significant purchases often relate to the husband’s retirement date. Even charitable giving tends to favor the husband’s preferences.

Of course, these generalizations result from studies of large numbers of women and not individual situations. There are many exceptions to these oversimplifications, but gender differences still exist, leaving some widows vulnerable when their chief financial decision-maker is no longer available.

This combination of less knowledge, lower confidence and unbearable stress, is detrimental to a widow’s financial well-being. You, as her advisor, can be her most important support. When women receive support and guidance from someone they trust, they are statistically more loyal, more likely to promote you, and more likely to tell their family and friends about you. Helping widows navigate this life-changing transition may require extra time, thought and patience. Still, it can result in cultivating a rewarding relationship with a client who will never leave you.

Why Women?

Women live longer than men, so widowhood is more common among older women compared with older men. According to the most recent U.S. Census, there are over 14 million widows in the U.S., with 1 million added each year. Widowed female seniors outnumber widowed males by more than 4 to 1. Some have referred to this as a “widows’ tsunami,” a fast-growing demographic that we should not ignore. Widowhood is more common than people think, leaving an overwhelming number of women on their own.

Why is Financial Advice Different for Widows?

Financial advisors find widowhood a unique circumstance to advise on because situational factors take precedence over “technical” financial solutions. Financial advisors need to consider the psychological side of decision-making during this stressful time, even if the advisor does not feel adequately prepared. Advisors must recognize the effect of grief on a widow’s ability to cope.

Overall, life transitions arouse grief, and in widowhood, this grief is intense. Nancy Schlossberg, an expert in adult transitions, defines a transition as “any event, or non-event, which results in changed relationships, routines, assumptions, and roles.” A shift can only exist if the person experiencing it considers it to be a transition.

Think about the grief we all shared these past couple of years due to the pandemic. Many people felt emotionally drained, disoriented, overwhelmed, lonely, angry, frightened, helpless and disconnected. We felt this way as we entered a transitional state where our relationships, routines, assumptions and roles changed, and our future became unclear. A widow also feels these emotions that effect her moods, behaviors and relationships.

“Nancy Schlossberg defines a transition as “any event, or non-event, which results in changed relationships, routines, assumptions, and roles.”

It also affects how she makes decisions since her body is in a state of survival. Stress causes her neocortex, her thinking brain, to shut down. The result is that her limbic system, responsible for emotions and the reptilian complex responsible for instinctual behaviors, takes over decision making. While grieving, a widow may lose her reasoning skills and becomes incapable of thinking things through rationally. As her advisor, it is important to be aware of her state to protect her from irrevocable decisions and shield her from deliberating non-urgent decisions that intensify stress.

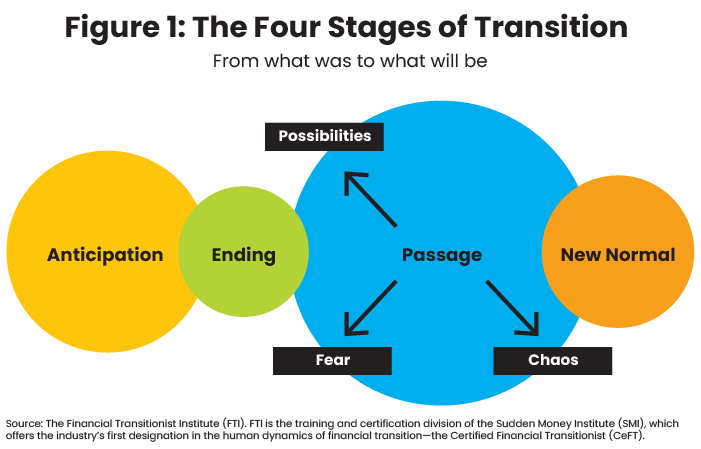

Four Stages of Widowhood

There is significant literature and exploration related to transition theory by Dr. Schlossberg and others. A transition is an event resulting in a change in assumptions about oneself and the world; it requires a corresponding change in one’s behavior and relationships. How one perceives and copes with the transition will dictate the intensity of the shift. The Financial Transitionist Institute (FTI), the training and certification division of the Sudden Money Institute) has summarized much of the academic literature on transition theory and has conceptualized the following four stages in a framework to manage the process (Figure 1).

When we think about the pandemic transition, we didn’t have much time in the anticipation stage, and often widows don’t experience this stage either — they go immediately into ending phase. With this pandemic, we immediately felt uncertainty, loss, grief, fear, denial and hostility — emotions associated with the ending stage. Today we have seemed to have passed through the pandemic ending phase, as the vaccine has become widely available, although leaving this stage has been difficult. At best, we are beginning to move into the passage stage where the crisis feels like it may be over, and we are beginning to incorporate more permanent adjustments in our lives. We will be in the new normal when our future is clear, and we are sure about how our new world will look. At that time, the pandemic will be a faint memory.

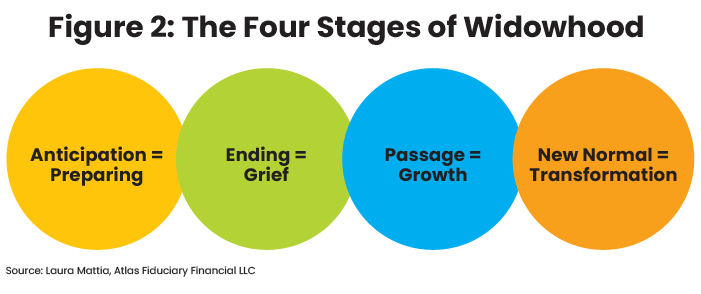

I am drawing this parallel so advisors can understand the widow’s experience. But while we are experiencing this pandemic transition as a society, the widow’s experience is private and lonely. If we have been having difficulty, one can only imagine how difficult it must be for a widow. Understanding and empathizing with her experience is the first step to helping her. The widows financial transition stages are Preparation, Grief, Growth and Transformation (Figure 2).

Sensitivity to the Widows Experience

When I met Lillian, she told me that she had lost her husband and needed help managing her investments. She was not interested in comprehensive financial planning, even though I assured her it would not cost extra. She was adamantly against it. I did not push, assuming I would build trust as we worked together. We could go deeper into her financial life later. I did not realize the recency of her loss — her husband passed away a month before. No wonder she was not interested; she was in shock.

I realized over time that a comprehensive plan would have been overwhelming for Lillian. A modified discovery process would have identified her immediate concerns, and I could have helped her with those. Since I was not sensitive enough to alter my financial planning approach, I lost the opportunity to help her.

The grieving stage can last a long time. A widow can be in that emotional, numb state — “in a fog” — for a year or two, or longer. During this time, she is cognitively disconnected and might even seem flighty or impulsive. The most important thing you can do as her advisor is listen to her and hear her story.

She may want to talk about her husband and tell you stories that seem irrelevant but will help you understand her concerns, her emotional state and how you can help her. You should expect and prepare for tears and other emotions. While you listen to her, you can identify immediate and future needs, but more importantly, build rapport. Please do not gloss over this initial listening stage, which goes beyond financial data gathering. Remember, to empower widows financially, you need to understand where she is today to help her on her financial journey.

Laura Mattia Ph.D., MBA, CFP, is the CEO and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla.