We are all well accustomed to that bi-weekly direct deposit, and when that tap dries up, anxiety sets in quickly. As we move towards retirement, we are faced with a plethora of questions, but none more critical perhaps than, “How will I get paid?!?”

The time-tested answer was always fixed-income securities. Lock in a few points of low-risk income, add that to Social Security, and ride off (in a golf cart) into the sunset! However, with interest rates at all-time lows, retirees are forced to look elsewhere to shore up their cash flows. The problem herein is that when stretching for higher yields, many are adding risk to their portfolio.

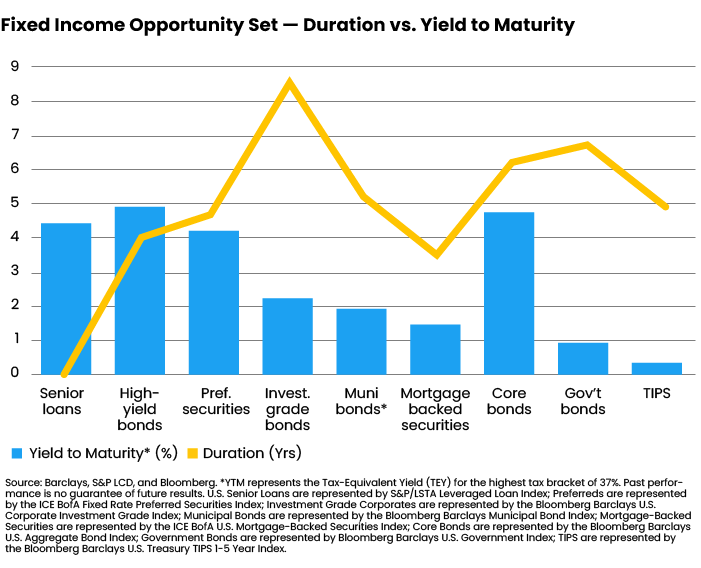

While trainers remind us that stretching is good, in this case, it forces investors to buy lower quality or riskier investments to produce the required income. Whether it be credit, duration, tax, or rate risk, if we don’t fully understand these risks, they will likely lead to disaster. The chart below evaluates some of the factors in play — the full analysis is a challenging endeavor.

Finding Fixed-Income Alternatives

A few years ago, we noticed this trend and searched far and wide for a solution to provide income to our clients while mitigating all risk factors. We reviewed many products, from publicly traded REITs and MLPs to more esoteric private lending and structured products. All had their merits, but just about all ultimately lacked the “piece de resistance”: high income, tax efficiency, controllable risk.

We recognized that direct, private, commercial real estate (CRE) could provide all those things, and we began putting together private partnerships to buy and manage attractive properties. By cutting out the middlemen, we reduce fees, increase yield, actively manage taxation, and anticipate/control risk.

Real estate is also somewhat inflation resistant. As the value of the mighty dollar goes down, the price of land goes up. So do the costs of raw materials with which to build new structures. Add to this a standard lease structure with annual rent increases, and you have a valuable asset.

The Special “CRE” Sauce

Real estate, in general, tends to appreciate in inflationary environments. We’ve had over a decade now of economic stimulus programs that have driven the cost of raw materials through the roof in recent times.

When deciding on an investment strategy for clients, don’t forget the time-tested adage in real estate: “Location, location, location.” We generally stick to Class A properties in strategic suburban markets. Fewer people want to commute to cities, and companies get more space in the suburbs for a similar or lower cost. There are eight different types of CRE (multi-family, office, industrial, retail, hotels/hospitality, mixed-use, land and special purpose). We prefer office properties because the rate of return (aka “cap rates”) is wider, leases are generally longer, and there is less tenant turnover.

Subscribe (Minimal 2024)

"*" indicates required fields

Another attractive trait of a CRE investment is that leases are higher in the capital stack than corporate or municipal bonds (“munis”), making them a more secure investment. In addition, they trade at wider spreads. For example, the corporate headquarters of a major hospital group is providing 8% cash-on-cash vs. their munis, which pay maybe 1.5% for ten years.

As with any real estate investment, it’s essential to conduct thorough due diligence before purchasing the asset. We always hire engineering firms to complete cost segregation studies upon acquiring new assets. These reports evaluate all aspects of the property and assign depreciation schedules by asset. For example, the parking lot surface may have a 10-year life while the roof could have 25-year life. So, instead of using the standard 39-year straight-line method for commercial property, we’re able to be both aggressive and tax-efficient. Cost segregation studies can also eliminate investors’ alternative minimum tax (AMT) and depreciation recapture by justifying accelerated depreciation.

Suitability + Structure

We offer private partnerships (typical LP/GP) for each asset that offers equity participation and debt. The latter is subordinate notes with fixed coupons and a stated maturity. The notes were primarily designed for retirement accounts, allowing IRA investors to access these deals without the risk of unrelated business taxable income (UBTI).

As the general partner, we can determine the payout structure and offer a cash-on-cash biannual payment. Meanwhile, investors are still accruing reserves and amortizing the mortgage Property value appreciation is usually not predicted in our model because we want to preserve total return even if property value stays stable.

These private investments are for accredited investors only. Liquidity is a risk because these investments typically don’t have a defined timeline. Clients must be prepared to tuck these funds away for a minimum of seven to 10 years.

As a fiduciary, we need to understand the risks and align them based on a client’s risk profile. By acting as the general partner/property manager, it’s easier for us to mitigate most risks. We even take our clients out on property site visits through the due diligence process to help build trust. If your organization is unwilling to structure these private partnerships, an advisor could consider introducing other deal sponsors with whom you’ve established rapport.

And while investors must maintain a long timeline when entering these investments, timing is everything. In today’s world, when you’re going to get 1.5% on a Treasury bond for 10 years, why not have a chance to get more with the same duration?

Stuart Caplan is the Chief Investment Officer of Apex Financial Advisors, Inc. (“Apex”) and Principal of AFA Real Estate Partners (“AFA”), located in Yardley, PA. APEX is a multi-family office offering comprehensive tax, estate, retirement, and investment planning solutions-all in one office. AFA, a privately held real estate investment and operating company, focuses on long-term, direct real estate investments.