Wealth managers often wind down their interactions with clients in their middle and later retirement years, leaving many retirees asset rich and advice poor, says a new report.

That’s a huge, missed opportunity, said Boston Consulting Group in “The Decumulation Dilemma” section of the report, “When Clients Take the Lead,” released June 10.

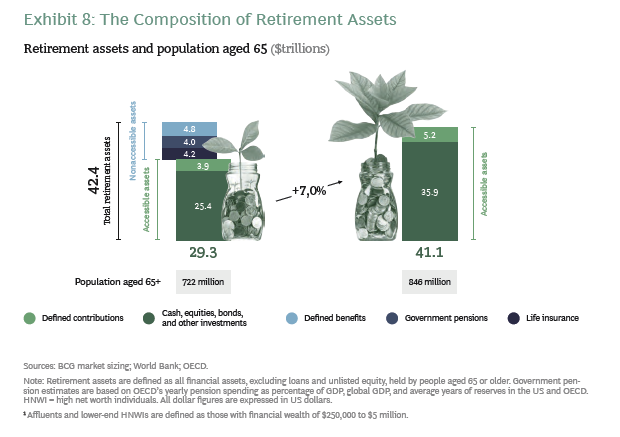

BCG estimates people age 65 and over, numbering 722 million worldwide, hold total retirement assets of $42.4 trillion. About $29.3 trillion of that is “accessible” to wealth managers to provide guidance on. The remainder is held in defined benefit, government pension and life insurance plans. Clients with those plans typically get recurring income and most likely won’t need the help of an advisor to manage the proceeds, explained Anna Zakrzewski, BCG’s global leader of wealth management, in an email.

“However, a client receiving a lump sum from his/her defined contribution plan when reaching retirement will need to define the most appropriate sequencing strategy — a financial concern wealth managers can help to address,” she noted.

Many wealth managers are eager to help set life goals and map withdrawal strategies for new retirees. But afterwards, advisors often feel they’ve resolved those clients’ needs and then interact with them infrequently, if at all, the report says. Wealth managers are leaving aging retirees to manage their finances when their needs are most complex, the report maintains.

The stress is particularly acute for individuals who have accumulated $250,000 to $5 million, BCG says.

“Their wealth gives them options, but it also introduces lots of questions, from tax and estate planning to broader life planning. Often, they have few reliable outlets to consult in trying to gather answers,” the report said. “And those that are available often require chasing down specialists in particular domains, such as accountancy and estate lawyers — a time-consuming and often frustrating exercise.”

What’s Stopping Advisors?

Until now, the report said, many reasons have prevented wealth managers from serving the holistic retirement needs of clients who are gradually drawing down their assets:

• The industry provides financial incentives to keep their clients’ assets growing, even during their withdrawal phase.

• Wealth managers have directed their efforts at wealthier individuals because they generate higher revenues that compensate for the high cost of serving retirement needs.

• The withdrawal phase is complicated. “Not only do retirees’ financial questions tend to be tangled—with asset drawdowns raising tax implications, for example—but their nonfinancial needs can be challenging as well, whether they involve finding a sense of community, pursuing a part-time job, or something else,” the report says.

A New Approach

But imagine how different a retiree would feel if in a follow-up conversation, an advisor used an all-in-one dashboard to provide an overview of her portfolio and walk her through withdrawal scenarios. The digital backbone of this service model would make it easier for financial advisors to update information and profitably support clients in the $250,000 to $5 million range, the report says.

Zakrzewski suggested ways to charge for holistic retirement services including a:

• Recurring fee for a basic retirement package including the common retirement services (e.g., decumulation planning).

• Variable fee when experts must be involved (e.g., planning inheritance).

• Variable fee when clients require services that go beyond the basic retirement package (e.g., having tax schemes from different jurisdictions included in their decumulation scenarios).

Five Steps for Advisors

BCG recommends advisors take five steps to better position themselves to serve retired clients.

1. Offer onsite financial education to employers with retirement plans.

Defined contribution plans like 401(k)s often are impersonal, hand-off experiences for participants. Advisors who offer in-person financial education can build lasting relationships with individuals that go beyond financial management.

2. Empower clients with digital tools.

Even when using a digital platform, advisors should meet in person with clients to get a comprehensive view of their wealth.

“Instead of sending clients a template to complete — or ignore — WMs who sit with their clients and perform the account aggregation in person benefit from five times higher adoption rates.”

3. Provide a team of experts who can answer questions on specialized subjects.

“To effectively serve the holistic needs of retirees, WMs must develop deep expertise in topics spanning from tax advisory to inheritance planning but also covering retirees’ non-financial needs,” Zakrzewski said.

She noted firms that serve ultra-high-net-worth clients can afford to have a dedicated tax expert working with a specific advisor’s clients. Firms working with affluent and high-net-worth clients can foster efficiencies by having one pool of experts for all advisors to access.

“What’s more, expert engagement should always be mediated by the advisor: If clients want to access experts directly, they should pay a premium for it to compensate for the higher costs-to-serve incurred,” she maintained.

4. Change incentives for front-office staff members.

Advisors and others often aren’t rewarded for providing the kinds of advice many retirees would welcome, like advice on spending, finding jobs and staying active.

“For example, drawing down assets might be beneficial to a retiree, but doing so would reduce the assets under management and therefore the wealth manager’s revenues — ultimately harming the scorecard of an advisor,” Zakrzewski said.

Over the long run, keeping score based on more qualitative measures has a lot of benefits. She says such measures will ensure client satisfaction remains high. They’ll also protect the firm’s reputation (no negative word of mouth from retirees to their heirs and network). Employees who provide these kinds of services are opening up opportunities for multigenerational wealth transfer and additional referrals, she said.

“A key prerequisite is that advisors need to be incentivized to spend more time with clients to discuss these issues even if they don’t generate extra revenues from it,” Zakrzewski said.

5. Address a broader set of retirement needs.

Wealth management firms can partner with senior-oriented social clubs, charities or retirement communities to help clients gain a deeper sense of community. (See Rethinking65 article on “solo” seniors.) Specialized counselors can help clients who want jobs. Charitable experts could provide tailored advice on the most relevant groups for donations.

“By helping retirees maintain a sense of purpose, community, and control, WMs can increase client adoption rates and monetize supplemental value at each stage of the retirement journey,” the report says.

Dorothy Hinchcliff is publisher of Rethinking65. Please reach out to her at dhinchcliff@rethinking65.com with your ideas for contributions to www.rethinking65.com.