Retirees and near-retirees are particularly vulnerable to inflation. As prices rise around us, we are spending considerable time digging into the past for lessons we might glean about the future.

Decades have elapsed since the U.S. experienced a serious bout of inflation. Recent data has shown that inflation seems to be picking up again. Several critical commodities have increased in price by double digits — some even by triple digits. Services prices are rising, and companies are hiking starting wages and paying signing bonuses to attract employees.

Whether these trends culminate in widespread, expected price increases that endure — which defines inflation — is the question of the day. Some clues could be unearthed by looking back more than 40 years.

Most economists remain indefinite about what caused inflation in the 1970s. The oft-repeated saying attributed to Milton Freidman, “Inflation is always a monetary phenomenon,” does not completely explain the situation. (We also note that several observers are concluding that vast fiscal stimulus and loose monetary policy cause inflation, which is not the same as acknowledging that inflation can arise after stimulus — a nuanced point but an important one which led many investors to draw the wrong conclusion after the monetary bump in 2008/2009.)

High tax rates encouraged owners of capital to pursue tax avoidance rather than development of production capacity.

Baby boomers coming of age increased demand for homes, cars, apparel, and so forth.

The oil shock generated by OPEC.

Wage negotiations that institutionalized wage increases for years.

Fiscal stimulus beginning in the 1960s and accelerating during the Vietnam War.

Unexpectednessand Rhymes

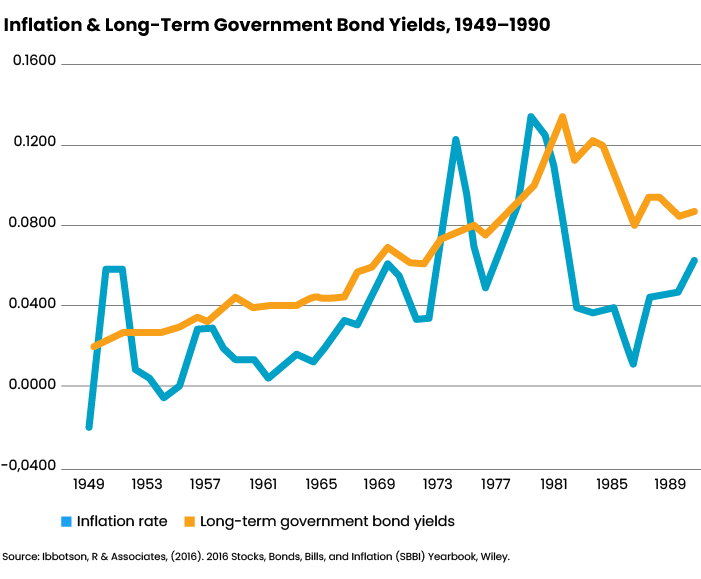

A hallmark of the experience back then was its unexpectedness. Having never dealt with such rapid price increases before, markets, citizens and politicians were taken by surprise. The bond market was slow to adjust. Below we show one year CPI versus the long government bond yield. Rates lagged the worst of inflation, dishing out negative real returns for a number of years. Note also that after inflation rates fell, it took the bond market some time to “believe” the trend.

Economists are accustomed to situations that “rhyme” rather than exactly replicate. The current situation rhymes with the 1970s, though the details are different:

Globalization is waning, if not by policy then by maturation. Wages are rising in emerging markets, and finding large untapped pools of cheap labor is more difficult.

Aging populations are proliferating around the world, another potential catalyst in the shift from capital ascendancy to labor ascendancy.

The effects of environmental, social and government initiatives are inflationary. Energy costs will rise, not fall; better pay and benefits will feed through to higher end prices; and even complying with sustainability reporting takes staff and time. (While we are on this topic, coping with the destruction that climate change is wreaking is also inflationary as insurance and mitigation costs rise.)

Millennials are the new baby boomers, hitting the market with a bulge of demand.

Fiscal and monetary stimulus is most certainly on the rise.

Despite these ominous trends, an inflection from low to high inflation will only emerge if existing production capacity can’t accommodate the marginal change provided by each of these inputs. Still, with warnings about “five years to ramp up chip production” and resistance to expansion in mining and lumber milling, for instance, the signs point to a tougher inflation environment for a few years.

Critical Questions

How might the bond market react, then, if inflation does take hold? Bond investors are in fact reacting exactly as seen in the 1970s: With a lag.

Most contemporary bond traders were not old enough to invest back then, so the “unexpectedness” of inflation today is an echo of 50 years ago, marked by disbelief during the outset of higher prices and a willingness to hew to the idea that this is “transitory.” Furthermore, the Fed has exerted some control over the government yield curve, suppressing price discovery, which is similar to the period after World War II when the U.S. government aimed to boost our recovery.

What should bond investors do about impending inflation? A critical consideration is that during the 1970s, finding assets that performed well during surging inflation was nearly impossible. Certainly that basket did not include stocks, bonds or cash. Investing during these periods really requires attempting to minimize loss of purchasing power and positioning for beyond the inflationary period.

Finding Income

We think selectively pursuing the entire corporate bond spectrum — high quality to low quality, including premium bonds (any bond selling over par) — offers an opportunity to hedge against inflation. Yes, spreads are miserable. However, price discovery is somewhat better here than in the government sector; corporations may retain pricing power that will partially protect them from inflationary bouts; and a political emphasis on jobs is protective of the business cycle to the extent that it is controllable at all.

Moral hazard has in fact become a tail wind. We have entered an economic and social phase in which recessions that wreck our job market are less and less acceptable. Business failures in the COVID recession were fewer than expected thanks to government loans.

Finally, the return to long corporates (Ibbotson & Associates, SBBI) during the inflationary period from 1949 through 1989 was substantially in excess of returns from long government bonds: Corporate bonds sported an advantage of roughly 33 percentage points over long government bonds, even before then-Fed Chair Paul Volcker stepped in to manage the situation.

What About Risk?

I can hear readers asking about risk. But risk exists in high quality bonds as well, especially if the Fed maintains control of the yield curve to suppress real returns. And if it does not, investors are uniquely exposed without the yield premium provided by corporates. Other researchers have shown that TIPS are not particularly useful during inflation. Furthermore, we are not recommending washing all government bonds out of portfolios, but we favor corporates.

Investors can reallocate to corporates to increase cash flow while locking in gains from government issues that have appreciated. The strategy may in fact work well even if inflation remains tame, thanks to the incremental return that corporates offer today.