If 50% of your clients over the age of 50 lost their job tomorrow, how might their Monte Carlo simulations for sustainable retirement income look?

How much more risk would their investment portfolio be forced to take?

What level of downsizing are they likely to have to accept?

This is not some crazy “what could possibly go wrong” scenario planning brought on by the COVID-19 pandemic; these are facts published in a research report back in 2018 by the Urban Institute.

And the statistics in the report “How Secure is Employment at Older Ages?” are sobering:

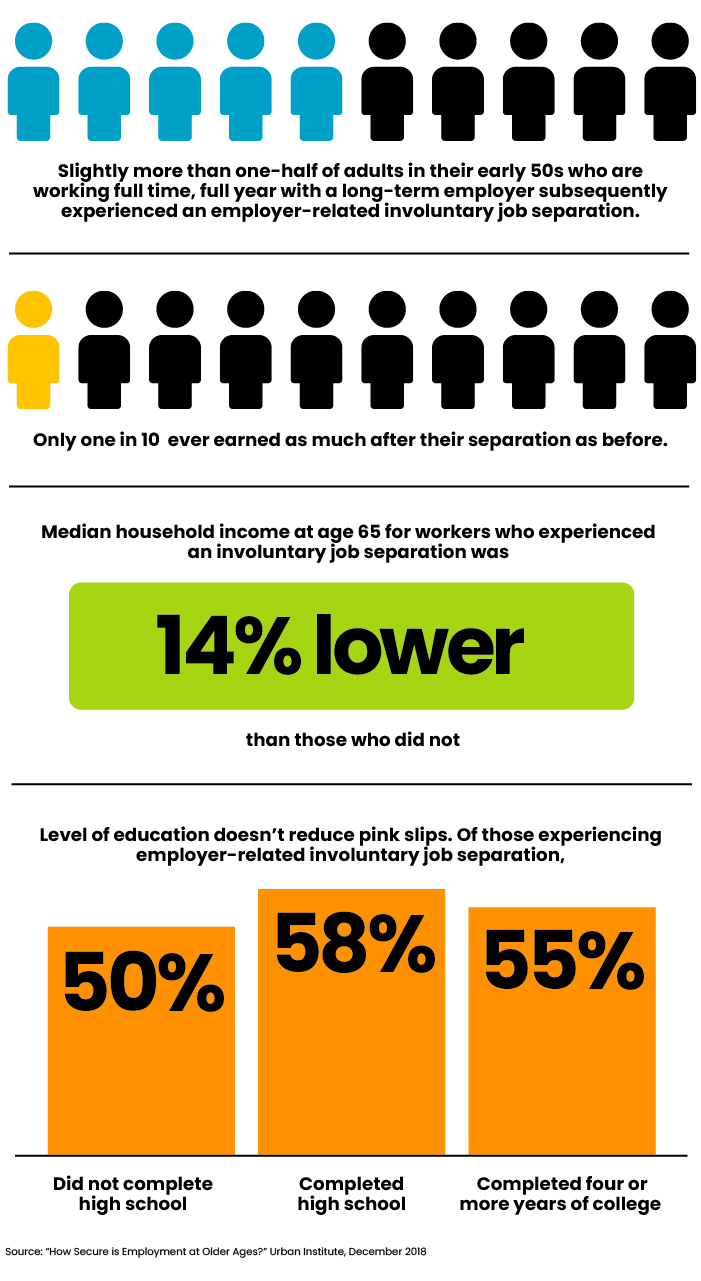

• Slightly more than one-half of adults in their early 50s who are working full time, full year with a long-term employer subsequently experienced an employer-related involuntary job separation.

•Only one in 10 of these involuntarily separated workers ever earned as much after their separation as before.

• Median household income fell 42% following an employer-related involuntary job separation, and median household income at age 65 for workers who experienced an involuntary separation was 14% lower than for those who did not.

“The steady earnings that many people count on in their 50s and 60s to build their retirement savings and ensure some financial security in later life can vanish, unending retirement expectations and creating economic hardship,” the report concluded.

“The steady earnings that many people count on in their 50s and 60s to build their retirement savings and ensure some financial security in later life can vanish, unending retirement expectations and creating economic hardship,” the report concluded.

Is the answer to recommend our clients invest in more education mid-to-late career?

Is getting a degree — or in some cases, an advanced degree — within 15 to 20 years of retirement a good financial move?

This 2018 study suggests education did extraordinarily little to protect workers from these types of employer-related job separations. It found that 50% of full-time, full-year workers in their early 50s who were employed in a long-term job and did not finish high school subsequently experienced an employer-related involuntary job separation. This compares with 58% of their counterparts who graduated high school and 55% of those who completed four or more years of college.

Be Smart

It is unlikely that doubling down on a degree at this stage of the wealth accumulation game will provide the protection our clients would expect for the time and money invested. Investing significant money in further education and/or borrowing money for this purpose is unlikely to provide the rate of return needed at this critical stage of life.

Going back to school may provide a new direction and purpose, very worthy goals. But if the goal is to find a new job that will be as lucrative as the one that was lost, earning a new degree in one’s 50s is unlikely to help your client achieve it.

So perhaps in our role as the trusted financial guide we need to add this planning scenario to our toolbox. We address premature death, we broach the subject of long-term disability, we recite long-term care statistics … but we rarely paint a picture of significant income loss in the “home stretch” of wealth accumulation.

And as we have learned over the years, we do not want to introduce a problem for which we have no solution. So, this is an exercise that requires a little creativity, some “out-of-the-box” thinking and several ideas that are not licensed and regulated.

Assuming the 2018 study rings true, it is likely our clients will find full-time employment but not at the level of compensation they had grown used to. In fact, it’s likely to be 40% less than they had enjoyed pre-layoff. With this unexpected loss of income in mind, we might find ourselves running the following scenarios with clients:

A Side Hustle to Replace Lost Income

• Netflix will pay a “tagger” $2,600 per month to watch streaming content.

• Drivers are paid an average of $400 per month if they allow their car to serve as a mobile billboard. (Not sure if this can be combined with driving for Lyft or Uber but that kind of double-dipping might just pay off!)

• Food tasters can have products shipped to their homes, or they can volunteer to taste fast food for a period of three months.

• Individuals who engage in public speaking on cruises (leveraging their area of expertise) receive travel for free.

Relocate to an Area with a Significantly Lower Cost of Living

• Downsizing in retirement is routinely discussed but this would entail a much deeper dive into housing, lifestyle cost and taxes in an area that was probably not on the client’s radar.

• International options may offer the best alternatives here. Although this may pose some challenges as it relates to travel and banking, these functions have made incredible progress in the last decade.

Restructuring a Client’s Balance Sheet and Income Streams

• The concept of a “paid off home” in retirement may have to transition to a reverse mortgage in their late 60s or early 70s.

• The idea of starting Social Security at normal retirement age vs. age 70 may come into consideration.

• Defining the “new normal” in terms of sustainable income given the changes to retirement account contributions moving forward will prove invaluable; they will need the guardrails to ensure they don’t take themselves down a path with no opportunity for recovery.

We are leaving too much at risk by not having these conversations with our clients. Perhaps the statistical probability of involuntary job loss among our clients is less than the norm because we are fortunate to serve a smaller, savvier segment of the population. But shouldn’t we be the ones to introduce this risk? Shouldn’t we be the ones to prepare our clients for this possibility — even if it’s unlikely?

We are in a unique position to add further value to our clients over the age of 50 by introducing the possibility of employer-related job separation and exploring a variety of solutions well in advance of an unwelcome surprise.

Beth V. Walker is a wealth advisor with Carson Wealth Management and founder of Center for College Solutions, which is based in Colorado Springs, Colo. She can be reached at bwalker@carsonwealth.com or 719-522-2278.