Editor’s Note: For decades, George Kinder, founder of the Kinder Institute for Life Planning, has focused on life planning, which he says “connects the dots between our financial realities and the life we long to live.” He recently spoke with Rethinking65.

Jerilyn Klein: You originally forged a successful career as a financial planner and tax advisor. How did you first get interested in life planning?

George Kinder: I never felt that taxes or financial planning was what I was born to do, but I had to make a living. What interested me more were questions of meaning, nuances of relationships, and the nature of civilization itself. I entered Harvard as a math major and left as an English major. I won the bronze medal on the CPA exam when I took it almost 50 years ago, but not because it was a passion of mine. My passion was freedom for myself. When I saw clients who were losing a lot of that spark, that inspiration, that energy, that excitement about life, and feeling that instead they had to pay the bills, I wanted to figure out how I could also deliver more freedom into their lives. Money was clearly a piece of that. As a financial advisor, I could bring financial skills to the areas I think we’re all passionate about: To live a life with meaning, to live a life of freedom, and to live a life of purpose.

Klein: Did you set out to start a movement?

Kinder: I don’t know that I started off with that. But I realized there were a whole bunch of people like me that also weren’t living as who they really wanted to be, in some way. And I began to realize more and more it was a community I wanted to serve and nobody was serving it. It was natural in a way to begin to be a leader in that movement, to draw attention to that movement and ultimately to draw attention to it all over the world.

Klein: This “community” you wanted to serve — were you thinking about advisors’ clients or advisors?

Kinder: Initially it was advisors’ clients. I didn’t really realize it was advisors until I was asked to give a speech at one of the national conferences. I was just stunned by how many advisors came up to me and were really moved by what I had said. I was talking really about a freedom-based, inspirational-based approach to financial planning that had a really deep listening and a tremendously fiduciary relationship with the client. By the way, I don’t believe that financial planning is fully fiduciary without doing a really thorough life-planning approach.

Then I founded with Dick Wagner the Nazrudin Project that became a place where I thought, engaged and taught with financial advisors, and kind of built a community over about 13 years before I began Kinder Institute.

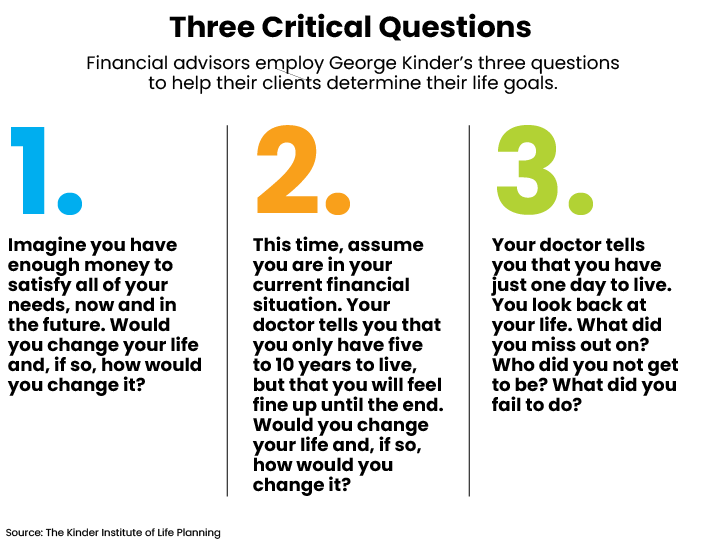

Klein: You’ve been posing three well-known questions for many years to help people determine their goals [See infographic below]. Have the responses changed over the years as baby boomers have aged, and has the pandemic significantly altered the responses?

Kinder: The questions, finetuned over a 15- to 20-year timeframe, ask us about layers of meaning in our life. The responses in general have been relatively similar over time. As we age, there is often a recognition that we’re ready for retirement. Retirement really is an old-fashioned notion based on the days of working in one job for a lifetime and accumulating funds for retirement. There are still people who do that. But I think the important question is, how do we live lives of freedom and great meaning throughout our lives? We only live once.

Kinder: The questions, finetuned over a 15- to 20-year timeframe, ask us about layers of meaning in our life. The responses in general have been relatively similar over time. As we age, there is often a recognition that we’re ready for retirement. Retirement really is an old-fashioned notion based on the days of working in one job for a lifetime and accumulating funds for retirement. There are still people who do that. But I think the important question is, how do we live lives of freedom and great meaning throughout our lives? We only live once.

So back to your question. As baby boomers have aged and as the pandemic has matured, people feel closer to legacy questions. Especially with the pandemic, they feel more tender and more vulnerable, perhaps more fragile, because of the closeness of death or chronic fatigue. Right now, people are very eager to get out and do things. More are leaving their jobs and not going back. I think this is partly a function of being able to work from home and seeing they can have more freedom, but mostly from COVID. What it means is, the whole population is much more open to these three questions, because legacy is more important, meaning is more important, and freedom is more important than they’ve ever felt in their life before.

Klein: What are the most notable recent studies related to life planning that advisors should be aware of?

Kinder: I rarely find anything of value in the studies and there’s a lot of reasons for that. I think people ought to look at who is funding that research; much is product oriented. The one study that was extraordinary to me is the happiness study that was done years ago by Daniel Gilbert and Matthew Killingsworth of Harvard — “A Wandering Mind Is Not a Happy Mind.” They found that if you’re really here in the present moment, you’re much more likely to be happy. Even if you’re lying on a chaise lounge at the beach with family, you’re much less likely to be happy if you’re distracted or the mind is wandering. One of the things that happens in life planning is we actually bring people to things that they’re really excited about being with in every moment of their life.

Klein: You’ve trained more than 3,000 professionals in 30 countries in the field of financial life planning. Have you observed a shift in the financial planners who are interested in this discipline, in terms of their types of practices and their goals? If so, what do you think is fueling this? And what can U.S.-based planners learn from other financial professionals around the world?

Kinder: It’s certainly becoming more mainstream, just simply because there are more people who are doing it. What was interesting to me, as we went from country to country, was that in almost every country, the first response was, “Well, you can do this kind of stuff in America because America has this therapy thing, this counseling thing, but you could never do it here.” They didn’t realize that we have red states as well as blue states, and we’ve got a John Wayne culture as well as the therapy culture.

The truth is that everywhere in the world, people long to put their money life together with their aspirations to deliver themselves into as much freedom as they possibly can. Consumers don’t know where to look, and that’s why the life-planning community has survived and thrived. Life planners are building books of business because — with fiduciary skills around investments and everything — they’re delivering people into the lives of meaning that the clients want. But there is still some resistance.

Klein: Resistance from whom?

Kinder: Every culture that I’m aware of, and this is disturbing, is dominated by product companies. The fiduciary standard is something I’ve thought about ever since I realized this was an issue, probably in 1980. It really says something that almost 40 years since the beginning of NAPFA and 50 years since the beginning of the CFP we still can’t get a fiduciary standard to be kind of de rigueur everywhere. So, I am optimistic, but only because the genuine fiduciary approach works for clients, and others won’t. But the problem is the marketing money and the political money is all on the other side.

Klein: How has your own outlook on life planning evolved as you’ve gotten older? And may I ask your age?

Kinder: I’m 73, but the average age of my staff and my trainers is probably in their 40s. As I’ve aged and gained perspective, I’m looking at life planning in broader ways. In the early days, I was thinking about consumers, financial services. Now I’ve been passionate about life planning civilization.

I’ve led workshops in Hong Kong, Mumbai, Tokyo, Singapore, Africa and all over Europe on what I call golden civilization work [improving civilization through conversation and collaboration]. We think the world is polarized, but it’s not really. Everybody wants kindness. Nobody wants corruption. Nobody really wants war, everybody wants freedom. Everybody wants sustainable. So, the polarization has other kinds of roots to it and other kinds of drivers than what is natural inside of human beings and our aspirations.

In addition, life planning delivers people entrepreneurial energy and enormous vigor because they’re free now to do what they’ve always wanted to do. One of our major mistakes is that we think of entrepreneurial endeavor as being merely something that is allocated or designed or allowed through our business schools, or through hedge funds or venture capital. But entrepreneurial endeavor is each person’s birthright, basically.

One more thing and then I will have longwindedly answered your question: There is a very simple solution to the problem that the world has, and it is “fiduciary.” If our corporations, nonprofits and governments had a responsibility to be fiduciaries — not merely to all people, but also to democracy and to the planet — I think virtually all of the problems of the world would fade away. Think about how much money banks have lent to polluters since the first Earth Day, back in the early 1970s, or how much big money has funded politicians.

Klein: You said entrepreneurial endeavors are each individual’s birthright. How can financial advisors help clients so they can actually live this birthright, or execute it, if they would like to?

Kinder: The first phase of our EVOKE model, Exploration, is all about listening, trust and relationships. The first thing that advisors have to do, because we’re one of the least trusted professions in the world, is to establish a relationship that is profoundly trustworthy — so that the client not only sees it but also feels it in the first meeting.

In the beginning, do you sit there and ask them about their portfolio and ask them about retirement? I would say, no. What you do is you simply ask why they’ve come in to see you. And then you pause — and when they answer, thank them and pause again. What you’re doing is inviting them to wander into the realms that are really important to them, at their own pace. Don’t push them into those realms, or pick up on one of their themes about finance and run with it. If you do it once you can still rescue the meeting; if you do it twice the client’s going to assume, quite rightly, that it’s your meeting, not theirs. And this first meeting has to be theirs, if you want a fiduciary relationship with clients.

We’re establishing the fiduciary relationship by showing the client that we really care about them, not about our product. We care about who they are and who they want to be. They know that we’re experts in products; we don’t need to push that forward. We want to hear their story, not in the context of what we’re selling or what our spreadsheets say. Later on, we’ll bring in the financial pieces and show them that, in fact, our expertise in retirement or our expertise in portfolio construction will really serve them well.

Klein: Do clients always want to talk? Don’t they want to hear how an advisor can help them?

Kinder: It’s a combination of both. If a client is coming to see you — let’s say they’re driving in or maybe they’re on Zoom — they’ve been thinking about this meeting and also thinking about what they really want to share with you. And they’re aware that most advisors won’t want to listen to what they really want to share. So, they’re a little nervous and shy, and maybe scared about sharing some of those things that will cut close to the bone about their emotions, relationship issues or aspirations. If you facilitate this meeting well, by really being a good listener, by caring for them, people will open up and share things that might not have come out otherwise. You’re going to have a much more fine-tuned financial plan. Plus, you’re going to have clients for life.

Klein: Even with established clients, advisors may worry about digging too deeply into their personal lives. Do you think it’s because of social etiquette or because many are more numbers oriented? How can they strike a balance between being helpful and what may be misinterpreted as nosy?

Kinder: Certainly, all of that can have a play, but I think the main answer is advisors aren’t trained and they project a lot from a psychological standpoint onto the client. And your second question, I don’t teach digging deeply — I don’t believe in it. I don’t do therapy; I don’t believe in that. I don’t believe in financial therapy. I am a great listener; I train people to be great listeners. I train people to be empathic listeners and inspired listeners who catch the inspiration of the client.

We train people simply to be there — not thinking about playing golf or the restaurant around the corner. This is where mindfulness comes in. We train people to be more emotional intelligent, to be more aware of their layers of anxiety or frustration, and to be at ease with them, so that the client then feels that comfort and is going to be much more willing to share.

I’m never nosy. Instead, it’s, “So what brings you here? Oh, wow. Oh my god. Fantastic. Oh, I’m so sorry to hear. Uh, gosh, that must be really tough.” There are huge pauses in all of this. Clients may feel a brief moment of discomfort but as they realize that that pause is there for someone who is really empathically connected to them, they become more and more comfortable of moving through that discomfort and sharing what they really want to share with you, what they really aspire to.

Because clients know the money should be tied to the fact that they want to play jazz piano on Wednesday nights in the club and they haven’t been able to figure out how to do that. Or they want to spend time with their 6-year- old son because they already feel that he is disengaged from them. Or they want to repair their relationship with their spouse. They want to share these things. But if we don’t feel comfortable in the process, if we feel awkward, if we don’t understand what the process is and how to do it, they’re going to feel that awkwardness and it’s not going to work. So, the answer to your question is really get trained primarily in listening skills.

Klein: How much should advisors divulge about their own lives, if anything? Is that a personal preference?

Kinder: I would caution you on the side of not doing it for the following reason. You share that you love golf, and the person who’s there can’t stand the game. You share that you have daughters, and the person that’s come in has a son. You share that you went to Italy and you love wine; the person that has come in is in AA. You’ve got all kinds of dangers going on as your share because they will project onto you that you’re not capable of listening around some of the things that are most important to them.

In the old days, it was: Make friends with them, go out to lunch, share who you are, and all that kind of stuff. But it will shut down the clients’ ability to actually share who they are. The meeting is for them. As you get to know them, you can bring in a little bit at the end.

In the first hour to an hour-and-a-half of a typical one-and-a-half to two-hour meeting, my guess is the client would have talked 90% to 95% of that time, and I would talk 5% to 10% of the time. One of the most common responses I would get at the end of the meeting would be, “George, that was one of the most incredible conversations I’ve ever had.” And the truth is, we didn’t have a conversation. They talked — that’s what makes it an incredible conversation. People want to talk about what is most meaningful for them. And this is an opportunity for them because it’s putting their money to work for those things that mean the most for them.

Klein: What are the risks — to clients and to advisors — if advisors don’t embrace a financial life-planning model?

Kinder: You don’t listen, you don’t give the space to the client to reveal, you don’t create that comfort space. The tragedy is for clients, but for advisor’s it’s more superficial. Clients aren’t going to trust them so they’re more likely to leave them. The client is less likely to invest fully in what they suggest, and less likely to trust the advisor’s recommendation around risk. There’s great danger that the advisor will invest inappropriately for the client, not really knowing who the client really wants to be.

Klein: You mentioned mindfulness. How do you practice being mindful, and how can advisors learn be more mindful?

Kinder: I’d say take a mindfulness course and establish a practice of mindfulness of at least 20 minutes a day. I practice for several hours a day and have for 50 years. You can’t do too much of it; it’s an incredible thing. The primary activity is you let go of your distractions and thoughts; you simply return to the physical sensations of breathing at the belly or at nostrils. That’s the simplest description.

When a client comes into our office, usually we clear our desks a bit; we need to clear our minds. Before a client meeting, take a few minutes and come back to the present moment, come back to the breath. What’s happening is you’re letting go of your preoccupations — all the things I, me and mine that we get hooked around. You’re practicing being “here” more, and when the client comes in, you’re more likely to be there for them, and they’ll see that and experience that. There’s emotional intelligence that reaches beyond what we say.

Klein: You grew up in coal country. Did anything from your youth also spark your interest in life planning?

Kinder: Absolutely, I owe a tremendous amount to the area that I grew up in. I lived along the Ohio River on the West Virginia border in areas that had the worst effects of the Great Depression and where the Rust Belt ate away at the society in profound ways. The people were absolutely wonderful, they were what we called salt of the earth. They had basic values and were virtuous, generous with their time, patient. They cared for their kids, they cared for the planet, they cared for the community. I can go into a place where the red and the blue convene together and they come out with the same vision of a golden civilization. I think what I learned was that people are basically good all over the world and all over the country. And that’s a wonderful thing. It’s time for us to get together again.

Klein: It’s good to end on that positive note. Thanks, George, I really enjoyed our conversation today.

Kinder: Jeri, wonderful speaking with you. Good luck with all this and I’m so excited about your venture Rethinking65; I think it’s wonderful.