As advisors, we often find ourselves in a “gatekeeper” role — reigning in expectations or doling out permission slips as it relates to our client’s financial wellbeing. The sacred trust we cultivate as we peel back the layers of emotion behind the fears and hopes expressed around the concept of wealth put us in a unique position to help clients balance their current lifestyle wants with the desire to provide a meaningful legacy for their children and grandchildren.

But finding that balance is a delicate matter.

Warren Buffett famously said you should “give your kids enough money so that they would feel they could do anything, but not so much that they could do nothing.”

Far too often, parents save and invest and “live smaller” with the idea that they will leave a meaningful inheritance for their children — failing to experience their generosity in action or to see their values reflected in the lives of the next generation.

Why not enjoy the satisfaction that comes from seeing the benefits of the wealth created and passed along? Why not pay for an extended family vacation, enjoying each other’s company and letting someone else clean up afterwards?

Clients’ adult children rarely want the paid-off house; they want or need the money stored in the equity of that residence where so many memories were shared. Far too often, inherited funds are immediately used to pay down debt as the initial instinct may well be to eliminate the cash flow pressure monthly liability payments represent.

Which brings us to the idea of helping adult children pay off student loan debt.

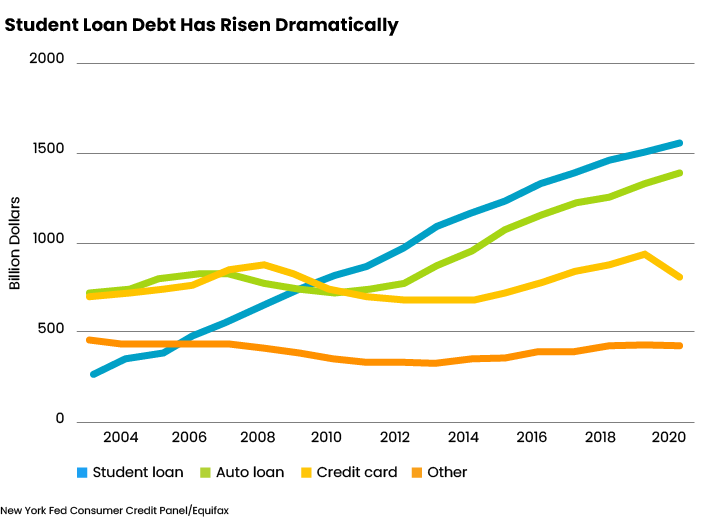

As the cost of college has escalated to unfathomable levels over the last 25 years, so has the burden of paying off the loans used for those degrees. Student loan debt has risen dramatically in comparison to other forms of borrowing in our consumer culture.

If — and only if — a client can afford to gift money to adult children, providing funds specifically targeted toward paying off student loans offers a meaningful way to share wealth along the way.

It’s a classic win-win scenario in that it allows the parents to reinforce the importance of education (assuming that is a core value) while reducing the financial pressure for the next generation at a time when they are often juggling their own efforts to balance current lifestyle, future retirement and educating their own kids.

Helping adult children or grandchildren pay off their student loans can also help them improve their credit scores by allowing them to meet every payment deadline, reduce other liability balances (e.g. credit card or auto loans) and increase their credit capacity. This can potentially put them in a better position to finance their first home (better rates and a bigger down payment) or borrow money to start or expand a business or professional practice.

Conventional gifting strategies result in an annual check, allowing the recipient to determine how to use the money. Imagine a more targeted approach that earmarks funds specifically for education-related debt.

Here are just a few ideas for how this could be applied:

• A “matching” program. Your clients offer to “match” the current loan payments being made by their adult children or adult grandchildren (up to $30,000, assuming a married couple — the IRS’s 2021 gift exclusion) to retire the debt sooner. It would make sense to “formalize” this by having some sort of document that allows your client to “match” the amount being used to pay down debt as a way of tracking and memorializing the gifting being done.

• A “pay-it-forward” program. Your clients make the monthly student loan payments, and the next generation funds an education savings account (529 plan, cash value life insurance, other investment, etc.) for their younger children (our client’s grandchildren).

• An “early inheritance” program. Your clients leverage home equity to retire student loan debt (using a conventional mortgage, reverse mortgage or home equity line of credit), in essence providing use of an intended inheritance tied to home equity prior to death.

• A targeted “RMD” program. Your clients, typically reinvesting their required minimum distributions into taxable investment accounts growing inside their estate, can direct those required distributions toward student loan debt for their adult children. Under the Secure Act, RMDs can now be started at the later age of 72, and that money can be used however account holders choose. However, I would only pay down student loan debt with RMDs that seniors are being forced to take solely for tax purposes and would reinvest in non-retirement taxable accounts — not distributions that they actually need and want.

Advisors should take the time to educate clients about what an “early inheritance” program can entail. For example, a home equity loan would require a monthly interest payment so it’s a function of cash flow — and a client might not be comfortable not paying principal and shrinking the loan. An alternative would be a small mortgage, leveraging home equity for the purpose of retiring student loan debt in an affordable, tax-deductible gifting manner. This could allow your client to pay both principal and interest on the loan each month and a get a tax deduction for the interest paid along the way.

The New Legacy Lens

Stepping back to survey the landscape of the next generation and their planning needs, in the context of the legacy lens of our current clients, we simply must include student loan debt.

Because of the way the Department of Education handles Direct Student Loans, most students finish their bachelor’s degree having borrowed $27,000 ($5,500 freshman year, $6,500 sophomore year, $7,500 junior year and $7,500 senior year). The clock starts ticking on the unsubsidized loans while the student is in college but the repayments don’t begin until six months after they graduate – assuming they don’t defer due to graduate school. So imagine a recent college grad with a bachelor’s degree starting out with just under $30,000 in student loan debt. The 10-year repayment plan would run approximately $272 per month for 10 years.

Receiving some of their inheritance now could be a lot more helpful to your clients’ kids.

If parents can help an adult child pay off a loan early, it can also sharply reduce the total loan repayment amount by reducing the interest expense. Using our example, an extra $100 per month would mean the difference between paying off that undergraduate loan debt 16 months earlier. This would free up cash flow for the adult children to begin saving for the down payment on a house or building emergency reserves.

College costs aren’t going down anytime soon so student loan debt is likely to be a planning challenge for decades to come. Why not make lemonade out of these lemons and give our clients permission to see the impact of their hard-earned wealth while they are living?

That said, it would be prudent to anticipate the Biden Administration will provide some debt relief for student loans — current rumors indicate between $10,000 to $50,000 per student. So advisors should not get too aggressive with having parents pay off their children’s student loan debt without taking those levels into consideration and/or waiting until the dust settles to determine what’s left to be paid off.

Beth V. Walker is a wealth advisor with Carson Wealth Management and founder of Center for College Solutions, which is based in Colorado Springs, Colo. She can be reached at bwalker@carsonwealth.com or 719-522-2278.