The Merriam Webster Dictionary defines longevity as “a long duration of individual life.” Due to improved living conditions and medical advancements, the average American’s longevity has increased from 45 years in 1900 to over 75 years today. Keep in mind, this 30-year increase is from birth. According to the U.S. Census bureau, a 65-year-old couple has a 50% probability of at least one them living to 90 years old! Today, researchers are developing drugs and other treatments that will not only increase human lifespans to well over 100 years, but also increase the physical and mental health of those lucky centenarians! Who wouldn’t want to live past 100 if they could be healthy, active, and sharp?

This does raise an important question, “Will my retirement savings support me over a retirement that may last 40 or more years?” Longevity is sometimes called the “Great Risk Multiplier” because, along with your savings having to provide income over more years, that income must also:

• keep up with inflation, which increases inflation risk; and

• have the ability to grow, which increases market risk.

In addition, increased medical and assisted living expenses later in retirement may put income even more at risk! In multiple surveys, today’s retirees are more concerned about living too long than they are about dying too soon. When I first began working with retirees in 1984, their concerns were reversed.

The best way to understand how longevity can affect a retiree’s income is to create some sample income plans that illustrate different longevity assumptions. To do this, let’s look at how a technology I co-developed called IncomeConductor® can quickly and easily illustrate the impact longevity has on a client’s retirement income. The beauty of IncomeConductor is that advisors can create a plan in minutes, then test out various scenarios with their clients in real time.

Let’s look at a sample client, Shirley. Shirley is a healthy, single, 65-year-old who has no children and wants to retire. She has managed to save $1 million and her Social Security benefit is estimated to be $2,500 per month if she claims at age 65. She would like to know how much total monthly income she can get from her $1 million in savings and Social Security, and since she has no heirs or favorite charities, she isn’t concerned about having any money left when she dies.

Shirley, like many retirees, is uncomfortable having all her savings invested in the market. She likes having at least a five-year buffer in her investment strategy that would create an account that would protect five years of income. This account would be safe with no market risk.

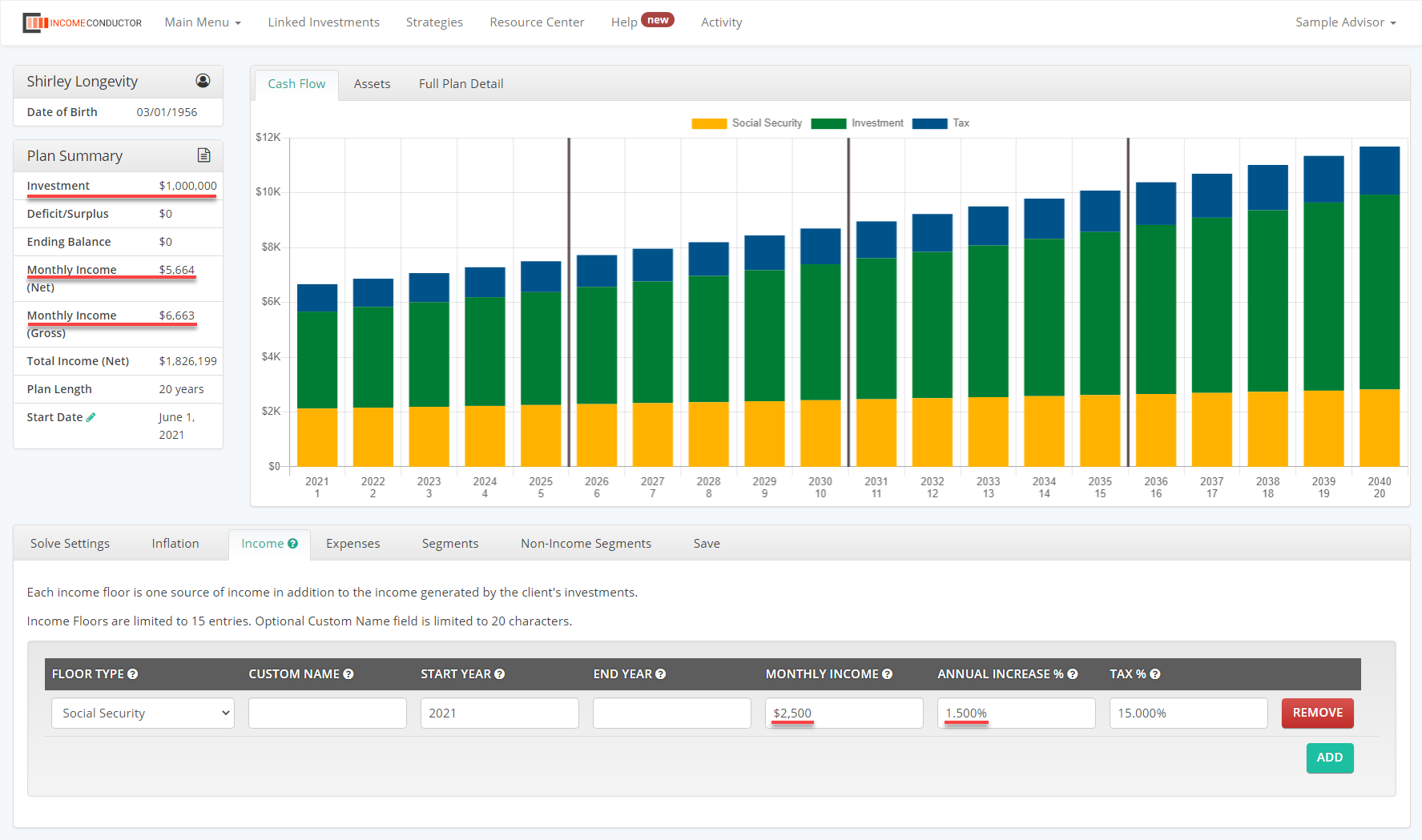

For Longevity Scenario 1, we will use Shirley’s actuarially calculated life expectancy of 20 years and solve the plan using her total investment amount of $1 million along with her $2,500 monthly Social Security benefit. It turns out Shirley could receive a beginning gross income of $6,663/month, which would provide $5,664/month net of taxes. Our plan assumes an overall 3% annual inflation rate on her total income and a conservative 1.5% annual cost of living increase (COLA) on Social Security.

This is good news since $5,600 is almost exactly what Shirley’s current expenses are, although she is disappointed that it wouldn’t allow her to enjoy the extra travel she wanted to do during the first five years of retirement. She is also worried about living past age 85 and running out of money since many family members lived well into their nineties.

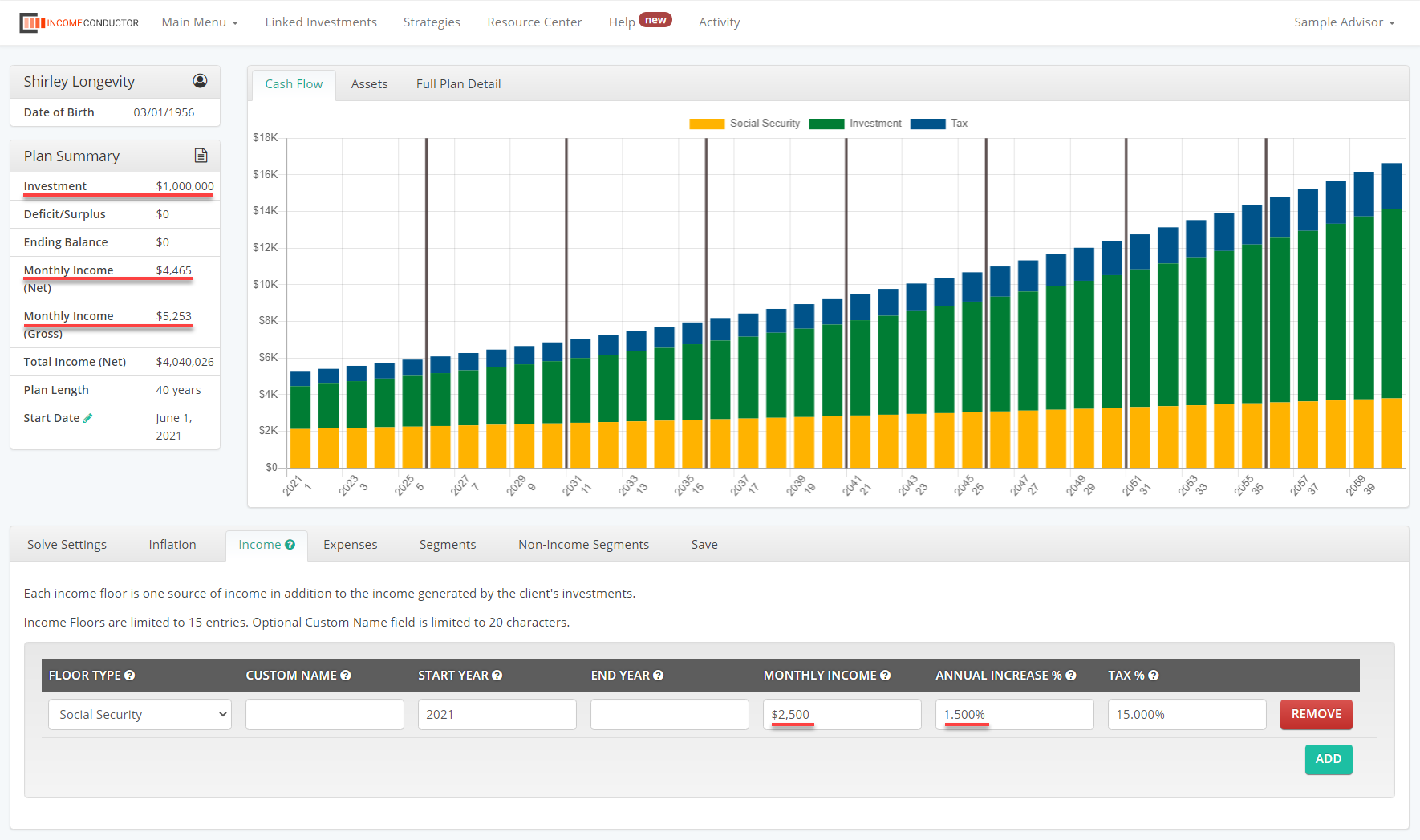

In Longevity Scenario 2 we go to the extreme of assuming Shirley lives 40 years to the age of 105. To do this, all we need to do is change the plan length from 20 to 40 years, using the same $1 million investment amount and still claiming Social Security at age 65.

Although Shirley is assured that she won’t run out of money over those 40 years, her beginning monthly income would be reduced to $4,500/month This 20% reduction ($1,100/month) is not viable since she needs the entire $5,600/month.

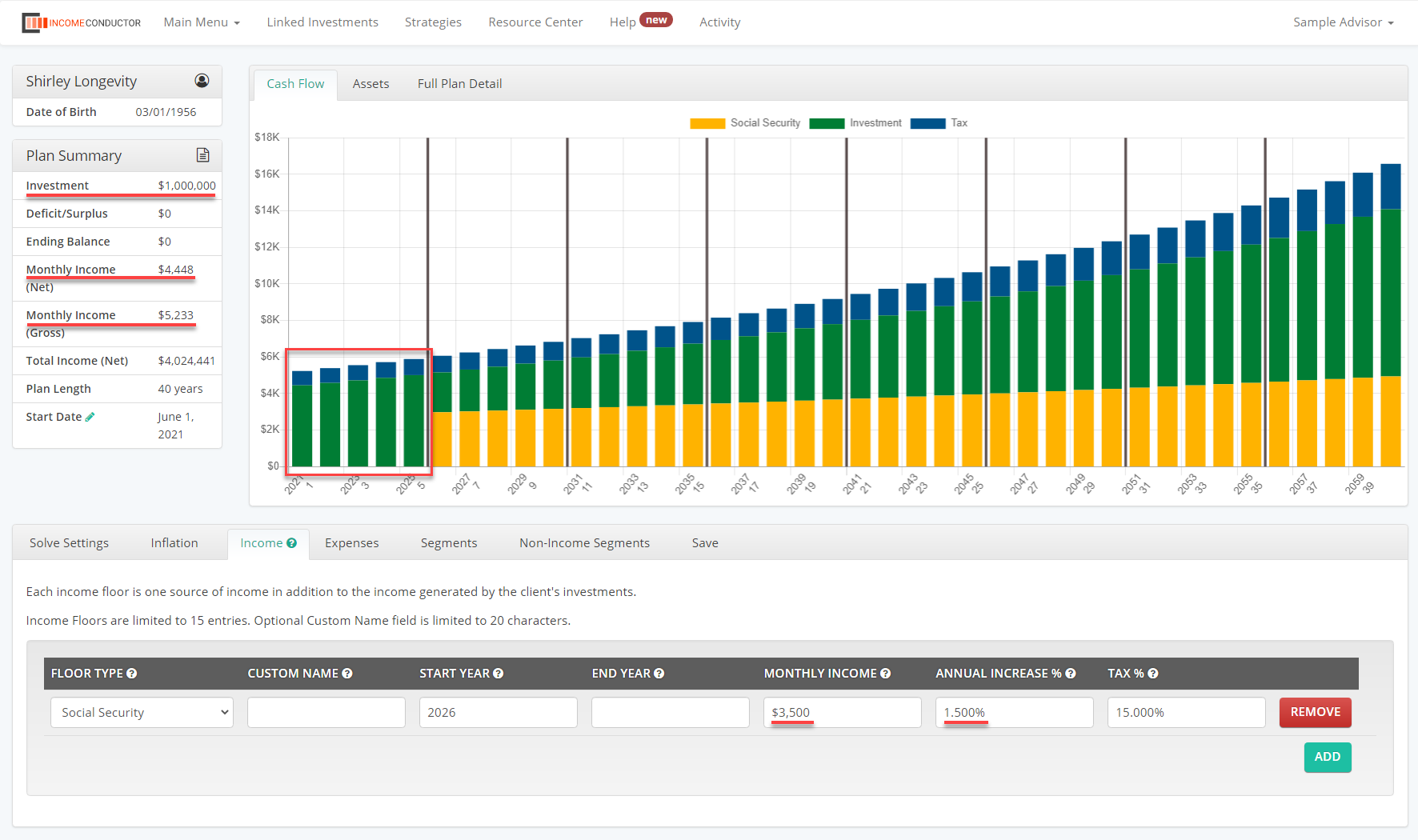

Shirley wonders if she could get more income if she waited to claim Social Security until she was age 70. It only takes a second to change the claim date to age 70 and benefit amount to $3,500/month in IncomeConductor. Surprisingly, this change made little difference in her beginning income.

This is because she would have to deposit significantly more of her assets into her five-year buffer account to bridge her to age 70. This buffer account is assumed to be earning a low rate of return. The loss of market opportunity on that additional amount offsets the value of the higher Social Security benefit at age 70.

In Longevity Scenario 3 let’s take a closer look at Shirley’s actual budget. When prior generations had shorter lifespans and only needed 15 years of income from their savings, growing the entire monthly income goal by the same inflation assumption was acceptable. Research by the MIT AgeLab and other groups now shows that today’s retirees go through multiple phases during retirement and their expenses may vary greatly from phase to phase and all expenses don’t increase at the same inflation rate.

Shirley’s starting $5,600 monthly budget consists of:

• $1,100 for mortgage principal and interest (which will be paid off in 5 years)

• $300 for Medicare, her Medicare supplement and other miscellaneous health expenses, and

• $4,200 for core expenses (i.e., utilities, food, clothing, etc.)

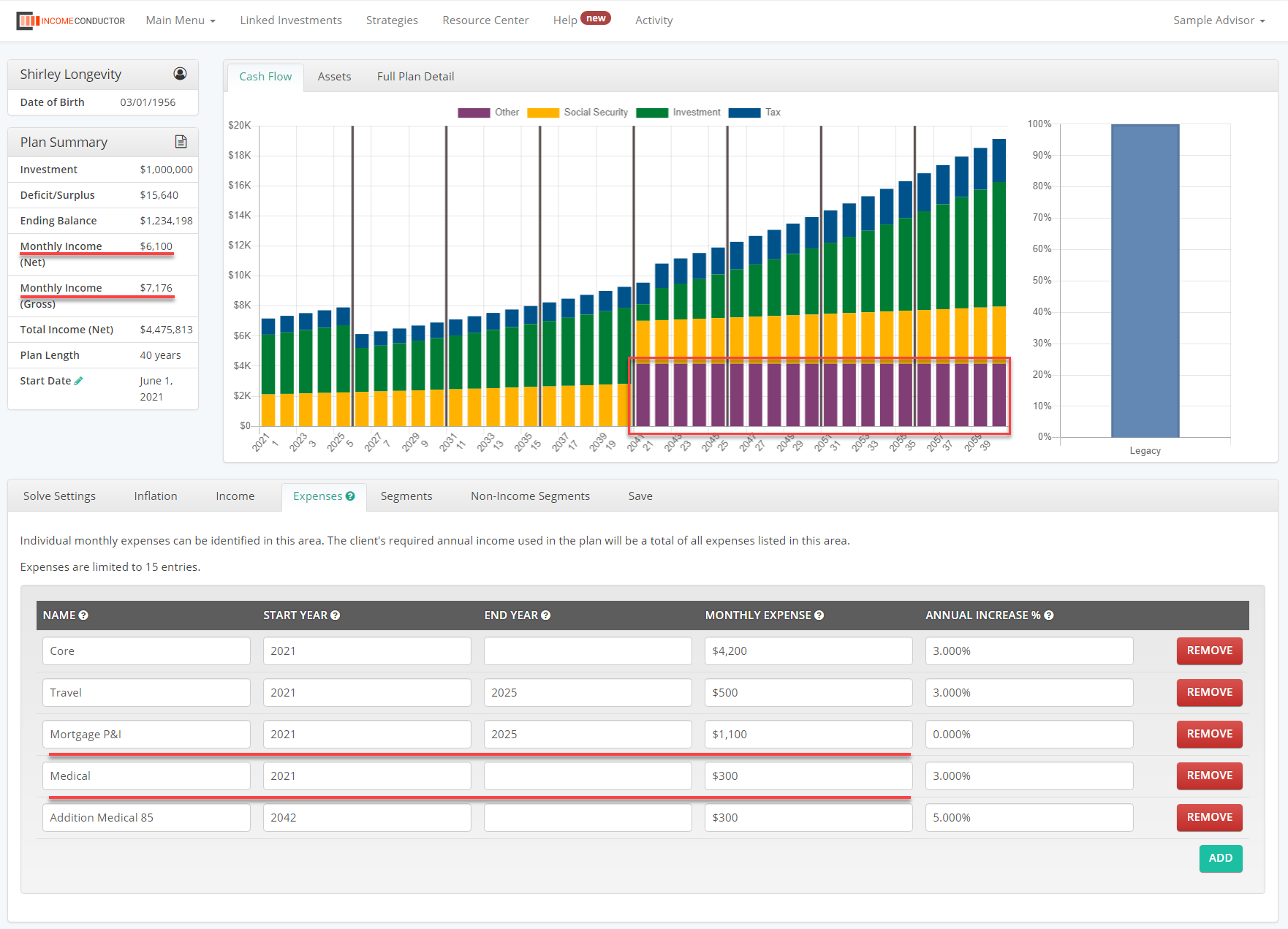

On the surface, it looks like the $1,100 monthly mortgage payment may be the problem. We can quickly run a scenario where she could eliminate the house payment by doing a reverse mortgage at age 65. In this scenario the reverse mortgage amount would only be the money needed to pay off the mortgage.

Although this approach lowered her expenses to the previously calculated beginning income calculated in Longevity Scenario 2, it still did not provide Shirley the extra travel money she was hoping for and it does not consider the possibility of increased medical expenses later in life.

Let’s take a closer look at her individual expenses:

1. The $1,100 monthly mortgage payment will end in five years and would not be subject to inflation.

2. Even though Shirley’s health is good now, she should at least double her medical out-of-pocket expenses at age 85 when her health could decline. I assumed this additional expense would be $300/month (in present value dollars) but increases at 5% instead of 3%. The bulk of her initial $300/month is the cost of her Medicare Plus Supplement, which should only increase at inflation since she is not subject to IRMAA and should remain in the “hold harmless” category. Obviously, her supplement is not tied to inflation but would increase as she ages and for other reasons.

3. Shirley doesn’t see herself living in her current home beyond age 85. She would like to transition to a retirement community but does not want to go to facility that would require her to purchase her unit. She has relatives that are happy in the type of facility that allows residents to lease on a month-to-month basis.

In the final scenario we agreed on these assumptions:

1. Shirley’s house is paid off in 5 years.

2. At age 85 her medical budget doubles and the additional expense increases at 5%.

3. At age 85 she sells her current residence for a value that is equal to it just keeping up with inflation for 20 years and can convert those proceeds to an income that would pay her 5% of the investment. This assumes her $675,000 home grows to $1,200,000 in 20 years and would provide her income of about $5,000/month starting then. She could also explore a reverse mortgage at age 85 if that could provide her even more monthly income depending on how that product works 20 years from now.

After making these customizations to her plan, Shirley can now have $6,100/month after taxes for the first five years of retirement, which will give her the extra travel money she was hoping for. She would have a value at the end of her 40-year plan of about $1,500,000 (which includes the balance of her original $1 million, plus the remaining proceeds from the sale of her home after taking her $5,000/month income). This ending balance gives her the assurance that, if she eventually needs a much higher level of medical care, she can afford the additional expense.

Summary

During my 30+ years of specializing in retirement income planning, I found that this level of planning is exactly what retirees want. They also want their plan to be collaborative and understand that, along the way, the economy changes, tax laws change and, most importantly, their needs will change. No matter how accurate we try to be in our initial assumptions, these assumptions will need to be adjusted in the long term.

By using IncomeConductor, advisors and their clients can create a “baseline” plan that includes multiple life events. Using IncomeConductor’s segmented methodology, advisors can easily illustrate the impact of changes along the way and give their retired clients information that is much more meaningful than just a new “probability of success” based on Monte Carlo simulations. Although Monte Carlo testing is a great compliance tool that documents that advisors have communicated investment risk and volatility, it falls short of what retirees want. Of course, they want to know if their investment portfolio has a good probability of supporting their income needs and will last as long as they live but being told there is some probability of them going broke does not provide them with the confidence to retire and enjoy the wealth they have worked so hard to accumulate.

Additionally, advisors tend to spend too much time focusing on investment risk and taxes and not enough time discussing and managing other significant risks like inflation, long term care, “out of pocket” medical expenses, and behavioral risk. I always told my clients that, given enough time, their portfolios will recover from “bad” markets, but their portfolios will never recover from “bad” behavior.

Even though the markets have always returned losses, I’ve never seen a doctor, hospital or care facility return the losses those expenses cause to an investment portfolio. Certain investment principles can be the same during accumulation and distribution, but the needs of clients during distribution are significantly different than their needs during accumulation.

With IncomeConductor you can easily and intuitively “stress test” a client’s retirement income plan against investment risk, inflation risk, longevity risk and long term care risk. With IncomeConductor’s “plan editor” you can visually illustrate each of these risks in person or virtually within minutes. This collaborative technology results in giving your retiring clients what they want…..A WRITTEN PLAN that can easily be monitored, managed and adjusted along the way.

Phil Lubinski, CFP, is a co-founder of WealthConductor, LLC and the Co-developer of the IncomeConductor retirement income technology. Phil has spent the past 35+ years working with retirees. He is considered the “Father of Segmentation” and not only built a successful practice specializing in retirement income planning, but also managed a very large OSJ in Denver that has branded themselves as retirement income specialists. He’s been recognized as an industry expert in retirement income planning and a contributing editor to many publications including Kiplinger, Money Magazine and Forbes.