Editor’s note: Christopher Baccella is a longtime columnist with Rethinking65. Read more of his articles here.

Christopher Baccella

In my last article, I discussed three types of bond portfolios — bullets, barbells and ladders — as well as the importance of maintaining liquidity in money markets and/or mutual funds. As we near year-end, I’ve begun to review my clients’ IRAs for required minimum distributions (RMDs). While many of my clients take their RMDs over the course of the year, either through monthly or periodic distributions, I have a few clients who choose to take their RMD in a lump sum around year-end.

For those clients, I have often found it beneficial to target maturities in late November or early December when filling out their bond ladder. By funding their RMD with a maturing bond, I may have exposed the client to less interest rate risk and less market risk. By timing maturities around year-end, I’m also less likely to repurpose those funds elsewhere (i.e., by buying a stock, mutual fund or long-dated bond). In other words, I can help eliminate the need to liquidate an asset at the wrong time.

Of course, when using this RMD strategy, an advisor needs to stay abreast of economic trends and market movements. And an important one at the moment is this: Interest rates have been on a wild ride.

Yo-yo Yields

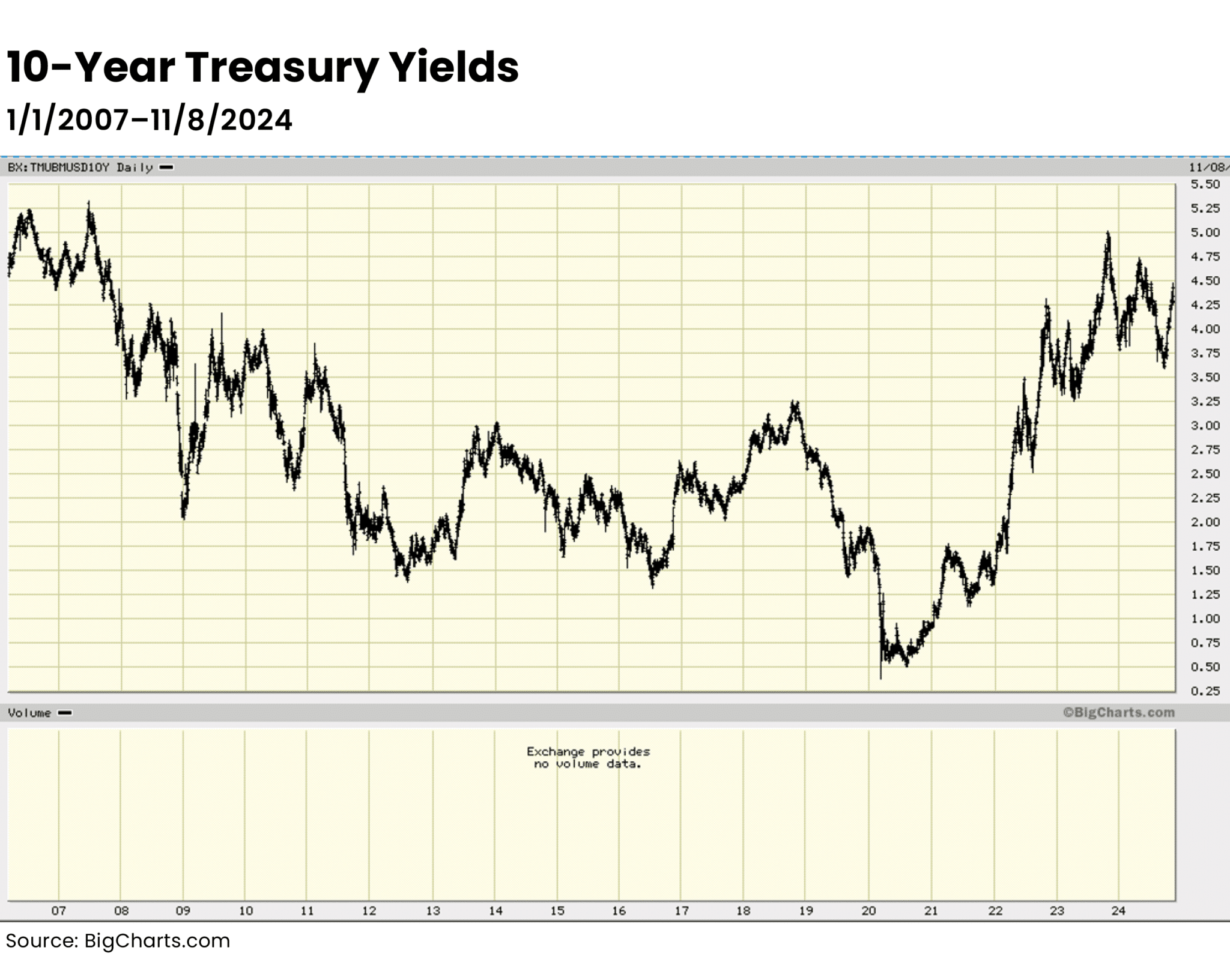

For example, 10-year Treasury yields peaked at nearly 5.0% in October 2023, then fell 125 basis points over the next two months before rising again. Rates began to trudge higher over the next nine months, peaking at 4.75% before falling once again, this time going as low at 3.6%.

Interestingly, 10-year yields bottomed right around the time of the Federal Reserve’s interest rate cut of 50 bps, so the bond market basically front-ran the Fed. Perhaps counterintuitively, yields have moved higher since the Fed’s cut. We are seeing “buy on the rumor, sell on the news” play out in the bond market.

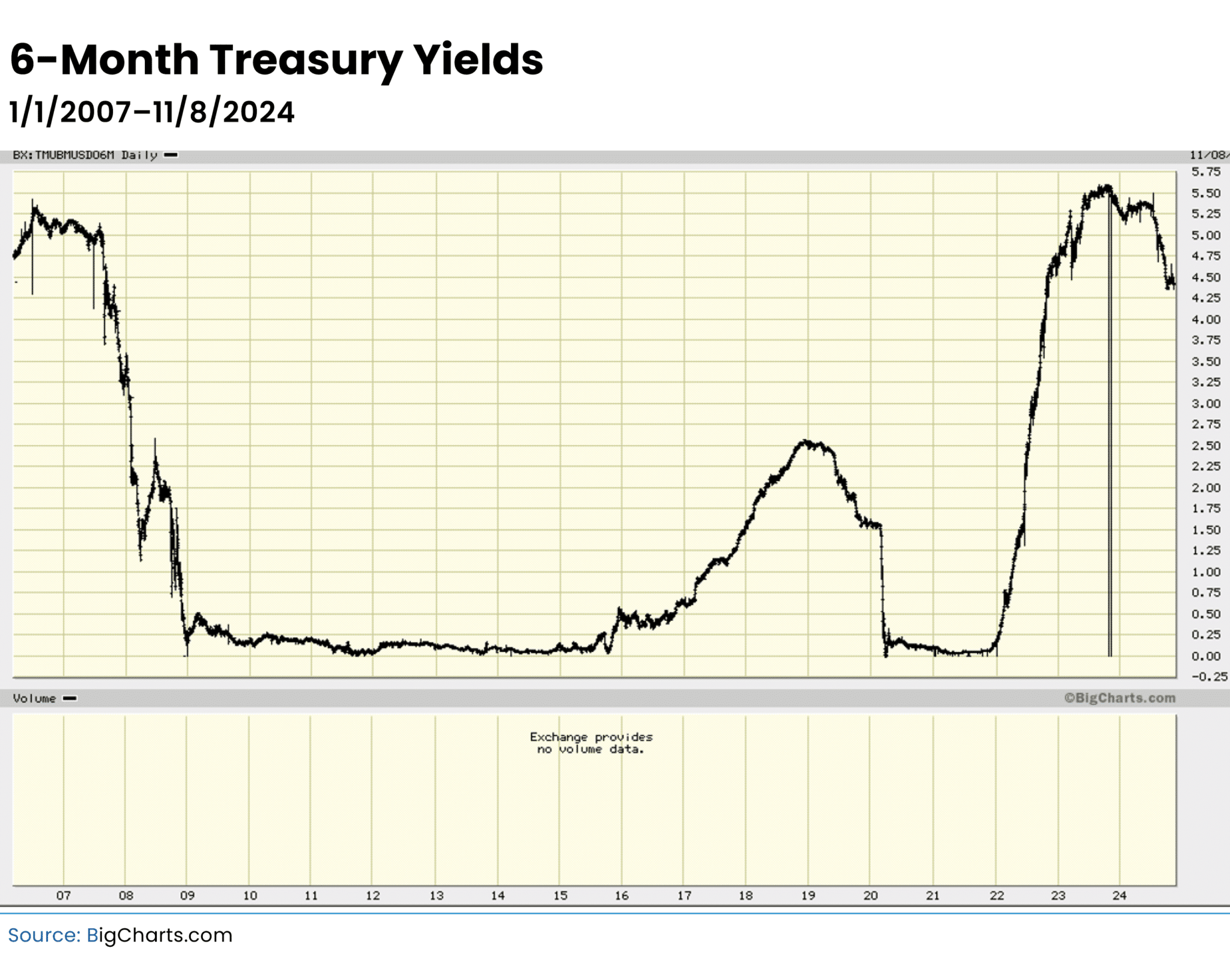

Meanwhile, shorter-term rates have followed a more consistent pattern. After peaking at nearly 5.6%, 6-month T-bill yields have fallen to about 4.4%, which is still near the high end in recent memory.

While falling yields have caused money market yields to slip from their highs, clients can still generate significant returns on their uninvested cash. Short-term rates, although off their peak, are at levels last seen in 2007 — nearly 20 years ago (see chart below).

Bonds Still Offer Attractive Yields

We are not attempting to draw a comparison between today’s environment and 2007. Our goal here is to point out that interest rates are still near relative highs versus recent history and can offer attractive yields to investors.

Remember to pay attention to the call features on new fixed income purchases, as many new issues are callable after a year or two. Investors may want to use bullets (non-callable bonds) to “lock in” today’s rate, at least for a portion of their portfolio.

When looking at charts, I generally tend to focus on a shorter time frame. However, I have recently seen articles comment on the current volatility in the bond market. While today’s bond market is unquestionably volatile, I think a historical perspective is necessary because it reminds us that, to some degree, volatility is part of the nature of the bond market.

As a reminder, the Fed tightened its benchmark fed funds rate by 525 bps — a level of tightening not seen since the 1980s. As I have commented many times in these columns, markets often get ahead of themselves trying to game the next move. This environment is no different.

Christopher Baccella, CFA®, a wealth advisor with Mariner, develops personalized wealth management solutions to help wealth management clients achieve their goals and grow and protect their wealth. He also provides investment management services to institutional clients. Chris has over 16 years of experience in the wealth management industry. He can be reached at chris.baccella@marinerwealthadvisors.com. Click here for disclosures.