For charitably minded individuals, cryptocurrency investments—such as Bitcoin and Ethereum—held more than one year may provide a unique opportunity to leverage highly appreciated assets to achieve maximum impact with charitable giving.

Donating long-term held cryptocurrency investments can unlock additional funds for charity in two ways.

First, your clients potentially eliminate the capital gains tax they would incur if they sold the assets themselves and donated the proceeds, which may increase the amount available for charity by up to 20%.

Second, if they itemize deductions on their tax returns instead of taking the standard deduction, they may claim a fair market value charitable deduction for the tax year in which the gift is made and may choose to pass on that savings in the form of more giving.

Donor-advised funds, which are 501(c)(3) public charities, can be a tax-efficient solution for contributions of cryptocurrency, as the funds typically have the resources and expertise for evaluating, receiving, processing, and liquidating non-cash assets.

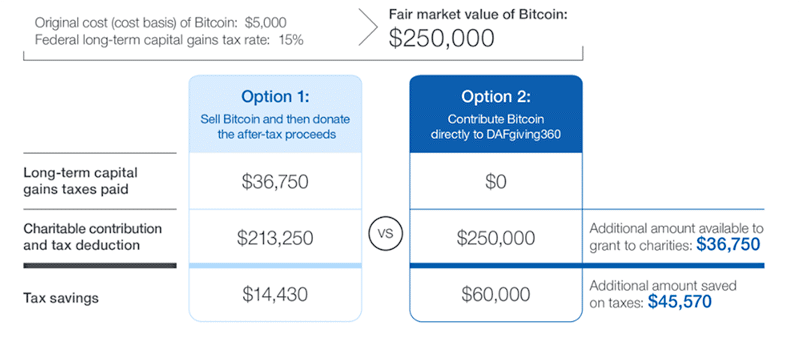

Case study: making a larger gift while increasing tax savings

Alison purchased 10 Bitcoin five years ago at $500 each for a $5,000 cost basis. Five years later, Bitcoin is valued at $25,000 per coin, so the total fair market value of Alison’s 10 Bitcoin investment is $250,000.

Alison could sell her Bitcoin and donate the net cash proceeds to a donor-advised fund or other public charity. In that instance, assuming a 15% federal capital gains tax rate based on her income level, she would realize appreciation of $245,000 and owe an estimated $36,750 in federal capital gains taxes ($245,000 x 15% = $36,750).

In this scenario, as shown in Option 1, after paying the federal capital gains taxes, Alison’s estimated net cash available for charitable giving is $213,250.

Now let’s review Alison’s benefits from gifting those 10 Bitcoin directly to a donor-advised fund or other public charity, as shown in Option 2. In this scenario, Alison can eliminate capital gains tax ($36,750), while potentially claiming a current year income tax deduction for the fair market value ($250,000), assuming she itemizes her deductions.

Additional considerations for your clients donating cryptocurrency

In addition to the potential tax benefits described above, the following considerations may apply.

1. Donate before selling.

To maximize the potential tax benefits described above, your clients can transfer their appreciated cryptocurrency, held for more than one year, directly to a donor-advised fund or other public charity rather than selling the cryptocurrency and donating the cash.

2. Avoid prearranged sales.

Your clients should not enter into any arrangement that would legally compel a donor-advised fund or other public charity to dispose of the cryptocurrency upon receipt. This kind of “prearranged sale” could reduce or eliminate the tax benefits of making the donation. Upon receipt of the cryptocurrency, the donor-advised fund or other public charity controls the asset. For most public charities, the general policy is to promptly sell contributed cryptocurrency, but a charity may reserve the right to sell at any time.

3. Unique tax features may apply to cryptocurrency donations.

A gift of cryptocurrency to a donor-advised fund or other public charity is not recognized by the IRS as a gift of currency or legal tender. For tax purposes, cryptocurrencies are treated as capital assets or income, depending on whether the cryptocurrency was held for investment purposes or received as a form of compensation (e.g., as a mining reward or income received in the form of cryptocurrency).

If the asset was held as an investment for more than one year and your clients itemize deductions, they may deduct the fair market value (as determined by a qualified appraisal) of the gift, up to 30% of their adjusted gross income (AGI) with a five-year carryover.

If the cryptocurrency was held as an investment for one year or less, or was not held for investment (i.e., ordinary income asset, such as where cryptocurrency was mined or received in exchange for services rendered), and your clients itemize deductions, they may deduct the lesser of cost basis or fair market value at the time of contribution, up to 50% of their AGI with a five-year carryover of the excess.

To substantiate your clients’ charitable income tax deduction, they are required to complete Form 8283 and obtain a qualified appraisal from a qualified appraiser for contributions of cryptocurrency valued at more than $5,000.

Interested in learning more?

• The Charitable Strategies Group at DAFgiving360 is a team of professionals with specialized knowledge about non-cash asset contributions to charities. Our team stands ready to support you and your clients, from initial consultation through asset evaluation, receipt, processing, and sale. We strive to provide unbiased guidance and frequent communication at every step of the process to help you and your clients make informed decisions and stay aware of the time required for their transactions.

• For more information about the advantages of contributing appreciated non-cash assets, you can read an overview article or call us at 800-746-6216.

• If you would like to learn more about donor-advised fund (DAF) accounts with DAFgiving360, click here.