Retirement is one of life’s most significant journeys, and like any important journey, careful planning is key to making the most of it.

While many advisors focus only on the financial aspects of retirement, it’s equally crucial to plan for the non-financial dimensions. Crafting a fulfilling and meaningful retirement requires time, effort and intentionality. Your client benefits from the investment by being able to see a clear path to a great retirement and it provides you with input to their financial plan and budget.

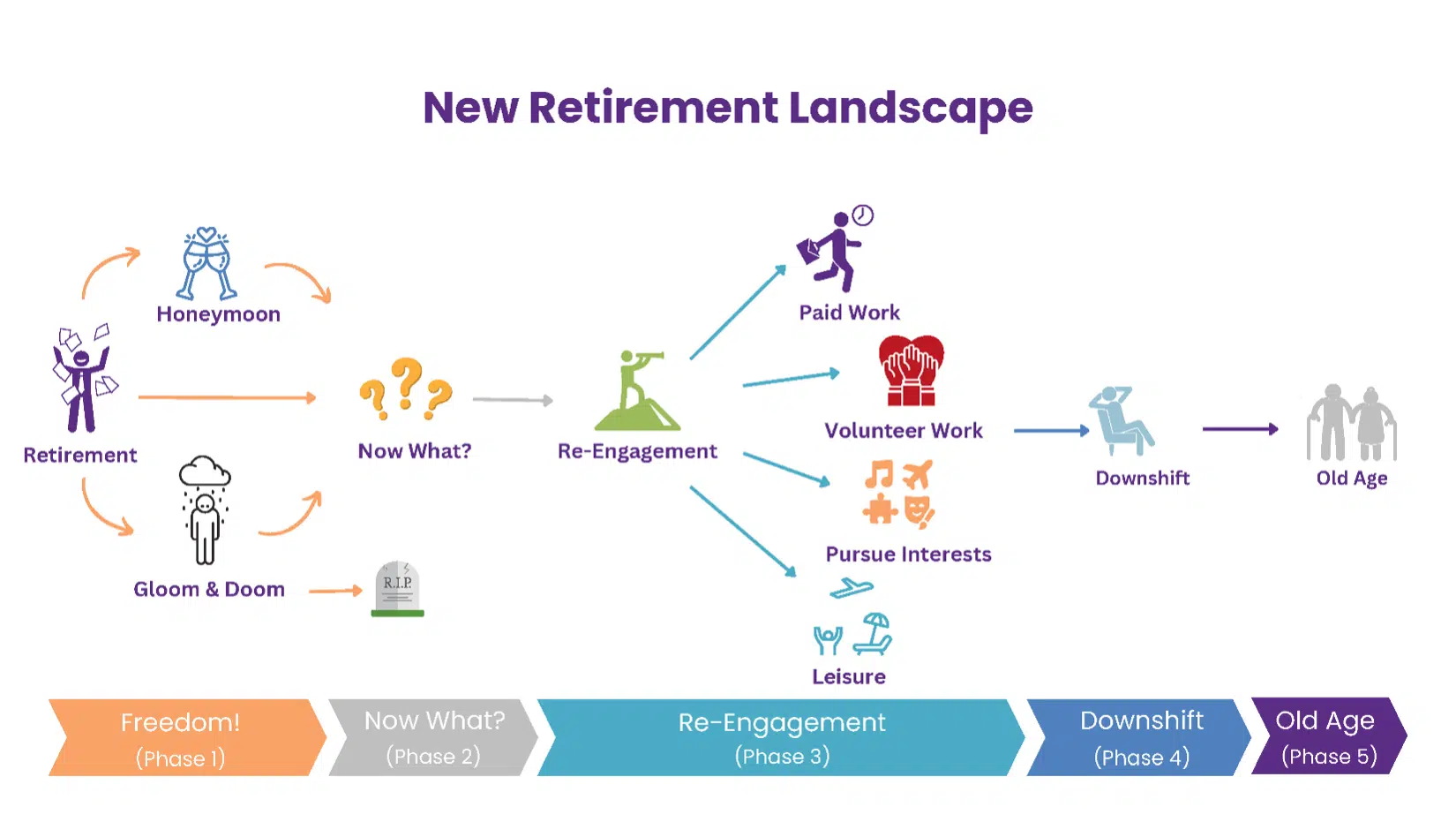

To start, it’s essential for your clients to create a vision for their retirement. In the past, the concept of retirement was often seen in two simple phases: Pre-Retirement and A Life of Leisure. However, today’s retirement landscape has evolved dramatically. Now, it encompasses five distinct, though not always clear-cut, phases. Understanding these phases provides a framework to help people better prepare for what lies ahead.

Source: Marianne Oehser

Phase 1: Freedom!

Retirement day arrives, bringing a significant life change. At this moment, three paths typically emerge: a “retirement honeymoon,” slipping into gloom-and-doom, or diving straight into re-engagement.

Retirement Honeymoon

Most people choose the honeymoon path, where the newfound freedom from schedules and stress feels exhilarating. It’s a time to enjoy long-awaited activities like travel or simply relax and recharge from years of stress.

This is the time when your clients make most of their bucket list purchases — dream trips and toys like RVs and boats. When your client is within a year of retiring, ask them about their retirement dreams and plans. If they don’t have a written lifestyle plan, encourage them to create one and review it with you so you are aware of the financial implications and can factor them into their financial plan.

This phase helps many unwind and regain energy before planning their next steps. However, the honeymoon will eventually end, often bringing questions like, “What now?”

Gloom-and-Doom

For some, especially those forced into retirement before they are ready, gloom-and-doom sets in. Retirement can feel like the start of decline, leading to inactivity, depression and health issues. Yet, even in this phase, there’s a choice. However, it may require professional help to climb out of it.

Watch for signs of depression in your client, especially newly retired ones. Ask them questions about what they are doing and how they are filling their day. Here are some red flags you may hear or observe:

Appearing sad, empty or hopeless.

Lacking enthusiasm for hobbies, activities or social events particularly ones they previously enjoyed.

Isolating themselves at home or neglecting personal hygiene.

Sleeping excessively or having difficulty falling asleep. .

Mentioning thoughts of death or suicide, or making suicidal statements

If you see any red flags, reach out to your client’s spouse or family member and share your concern.

With support and a shift in mindset, it’s possible to move toward a more fulfilling and positive path.

Straight into Re-engagement

Others skip the break altogether and instead dive straight into new ventures. Though re-engagement can be energizing, many eventually realize they need a sabbatical to rest and recharge before truly embracing retirement.

If you see one of your clients charging headlong into their next venture, suggest that they may want to factor in some downtime to recharge their batteries before they embark on their new adventure.

Phase 2: What Now?

Most people make the unrealistic assumption that retirement will be a 30-year vacation. In reality the honeymoon phase typically lasts between six months and 18 months. As it fades or your client steps off the gloom-and-doom trail, they enter the “what now?” transition. This phase is a time of uncertainty as they move from what was familiar to something new.

Transitions usually involve three overlapping aspects:

Letting Go is about releasing the past, both the good and the bad, to open up space for the future. Holding on can hinder progress and cloud new opportunities.

Time of Discovery is often uncomfortable but crucial. It’s a chance for your client to reflect on who they are now, their values, and what gives their life purpose. This is an ideal moment to start designing their Happiness Portfolio® — a plan for the non-financial aspects of their new life.

New Beginnings bring clarity. Like stepping out of fog into sunlight, you’ll eventually see a clearer path ahead.

We will all likely go through multiple transitions in retirement but understanding them helps us navigate each one with confidence, making each phase of life fulfilling.

The best way you, as an advisor, can support your clients as they go through a transition is to point them to resources. This can include articles, books and YouTube videos about transitions and how to effectively deal with the uncertainty. You will help increase their awareness that what they are going through is normal and it will end.This is also a time when a retirement coach can be especially helpful.

Phase 3 – Re-Engagement

Now it’s time to truly embrace their new life! Re-engagement means living an active, fulfilling life at one’s own pace, engaging in activities that bring joy and purpose. Your client’s energy is still high enough, and life feels exciting and rewarding.

This can be the most enjoyable and longest phase of one’s retirement journey.

But thriving in retirement requires more than financial security: Your clients also need a lifestyle plan for investing their precious resource — time. Again, this is what we refer to as the Happiness Portfolio®.

It should address their vision and action plan for eight non-financial areas of their life: Professional, Personal Relationship, Family and Friends, Giving Back, Health and Wellness, Self-Development, Leisure, and Spiritual and Emotional Well-being.

As your clients think through what they want each of these areas to be like, dreams and desires emerge that should be factored into their financial plan and their budget. Encourage your clients to create a lifestyle plan and share it with you so you can update their financial plan.

When your client knows that the events or activities they desire have been financially planned for, it frees them to spend the money rather than worrying if they can afford it. It is very sad when people miss making memories because they think they can’t afford to do something that in fact they can afford.

Phase 4: Downshift

Downshifting is a natural phase where you slow down a bit but don’t stop altogether. It’s about finding joy in a slower pace of life and balancing “doing” with “being.”

A friend, David, experienced this shift after years of high-energy activities. He felt guilty at first, thinking he was being lazy. But once he embraced his desire for more contemplation and a slower pace, he found a new sense of fulfillment. Downshifting allows you to savor life, much like taking the scenic route instead of racing ahead.

Dr. Donna Daisy, author of “Why Wait? Be Happy Now,” embraced this phase of her life, saying, “I don’t need to prove myself or achieve anything.” She highlights the importance of mindful thinking and focusing on the present moment.

In this phase, your client may have less energy but can still enjoy life in a meaningful way. It’s a good time to reflect on their legacy, whether through memoirs, journals, or simply sharing life lessons with loved ones. One way to encourage your clients to reflect on their legacy is by giving them a small journal to record their memories.

Downshifting isn’t about doing less; it’s about appreciating life at a more relaxed pace.

Downshifting isn’t about doing less; it’s about appreciating life at a more relaxed pace.

Phase 5: Old Age

Ideally, we all reach old age with manageable health and a peaceful life. Dr. Roger Landry’s book “Live Long, Die Short” emphasizes that we don’t have to accept the stereotype of aging as a long, slow decline. Instead, we can maintain our health and live vibrantly, shortening the period of decline.

Dr. Landry’s book talks about the MacArthur Foundation study called Successful Aging which found that 70% of physical aging and 50% of mental aging are due to lifestyle choices.

You can support your clients at every step of their journey by continuing to ask them what they are doing to maintain their physical and mental health. We all sometimes need nudges to sharpen our focus on these critical areas.

This is also the time of life when the need for more physical assistance may be necessary. Most financial plans already address this potential need. This is just a reminder to be sure all your financial plans have this component.

Being sure that your clients have a specific and written lifestyle plan for their retirement journey is important to both of you. Iit’s your client’s guide to living well and “dying short” — and it gives you valuable information you need for their financial plan.

Marianne Oehser is the author of “Your Happiness Portfolio® for Retirement: It’s Not About the Money,” and co-founder of Next Chapter Lifestyle Advisors. Marianne and her partner, Susan Latremoille, empower financial advisors to help their clients thrive in their post-career by having a clear lifestyle plan to complement their financial plan. To learn more, contact Marianne at Marianne@NextChapterLifestyleAdvisors.com or visit NextChapterLifestyleAdvisors.com.