As the most emotional purchase parents will ever make, college is literally the best time for a financial advisor (who knows how to do this right) to be a real hero and save their clients from making financial mistakes from which they may never recover.

As advisors, we know that once this emotionally charged decision is made, someone has to pay for it. Too often, families turn to conventional wisdom to help guide them. Based on the headline news about student loan debt and the ever-rising cost of college, that’s clearly not working.

The problem with conventional wisdom is that it’s so conventional. Which means that, by definition, it’s what everybody else is doing. In the words of the old Apple marketing campaign, it’s time to “Think Different.”

When it comes to funding college, conventional wisdom recommends that a family use the net price calculator on the college website to estimate what that college will cost the family for one year. Sadly, many of those federally mandated calculators are not updated or accurate.

Setting aside the inaccurate estimate for a moment, it’s more important to recognize this is backward problem-solving.

Every family should know their college spending ceiling. Three important questions will reveal the answer:

1. What can we afford?

2. How will we pay for this purchase?

3. What are our best financing options for buying college?

Let’s look at each one in more detail.

1. What can we afford?

Most of us don’t have the tools or training to calculate the consequences of how we buy college. Parents have no idea what impact college funding decisions will have on their current lifestyle, let alone their retirement.

Parents are literally being asked to make a six-figure financial decision with their “parent heart” taking the lead, but without having consumer protection or the involvement of an invested third-party gatekeeper in the decision.

Few families actually know how much it costs to support their lifestyle on a monthly basis. They may have a general idea (net payroll deposit minus mortgage, car payments, groceries, and eating out). But just like getting a root canal, there’s not a lot of enthusiasm for digging into the nitty-gritty details.

College is the perfect catalyst for determining what money is coming in, what money is going out, and how much cash flow can or should be earmarked for higher education. Because of the cost of college today, financing will likely be part of the overall funding strategy. As a result, understanding the cost of borrowing money has to be factored into the equation.

It’s one very important component of a roadmap I’ve developed to help parents and their students masterfully navigate the otherwise complex process of buying college. MAGIC is the acronym I coined to organize all of the components of a successful college project plan. This article focuses on the “M,” or money component, but Academics, Gifts, Integration and Confidence are also part of the plans that I develop with clients.

Buying College Should Be Like Buying A House

When you buy a house, the mortgage lender does a deep dive into your income, savings and investments, and other debt obligations (car loans, credit cards, your own student loans, taxes, etc.). They literally calculate your capacity to pay for the privilege of “renting” their money. Then, they put together a formal “pre-qualification” letter that you can use to actually buy a house.

Knowing your spending ceiling (what you’re pre-qualified for) dictates which zip codes you shop in. You look for homes that meet your success criteria (four bedrooms, finished basement, 3½ bathrooms, corner lot) within those spending guidelines. Buyers are able to separate the “must haves” from the “nice to haves” and make informed decisions about what they’re willing to concede because they know there is a limit to what they can spend.

When you apply the same thinking to college, you need real guardrails and guidelines for making this increasingly expensive purchase. You need to get pre-qualified to buy college, so you’re shopping in the right college zip codes.

Shrinking the universe of choice (currently, over 2,832 schools in the U.S. offer four-year bachelor’s degrees) into affordable zip codes is a great start, relieving much of the overwhelm and decision fatigue associated with the stress and anxiety surrounding the college purchase.

Shocking as it may sound, it turns out that purchasing college is more complicated than buying a house. Why? Because it involves the parent’s income and debt-to-income ratio as well as the student’s academic credit score.

This academic FICO® score will impact the cost of college by influencing grants, scholarships, tuition discounts, and student loan interest.

It’s vital for your clients to understand this: We want to approach college from the perspective of what we can afford, not what the colleges or the Department of Education tell us it will cost. This subtle but important shift in our decision-making framework represents an enormous change in our collective approach to college.

When parents make this transformational paradigm shift of understanding that they are literally buying college, it will save them from spending more than they should or having to live with the damage done by poor decisions made due to ignorance and emotion.

How Will They Pay for this Purchase?

Buying college better requires excellent retirement planning. We tend to be very linear in our approach to finances, dealing with our near-term financial priorities first.

All too often, parents are so focused on saving for college that they’ve lost sight of their need to get on track (or stay on track) for retirement. Parents literally can’t see or understand how the decisions they are making today will impact their lifestyle in 25 years.

This is why families are most vulnerable to making money missteps and financial mistakes that they may never recover from during their kid’s college years. Said another way, conventional wisdom has us funding college backward.

I’ve witnessed the mindset and financial behavioral shifts for families once they’ve taken the time and used the tools to forecast the probable outcomes of several different scenarios. I know that parents can (and do!) make better, more informed decisions about how to go about funding college.

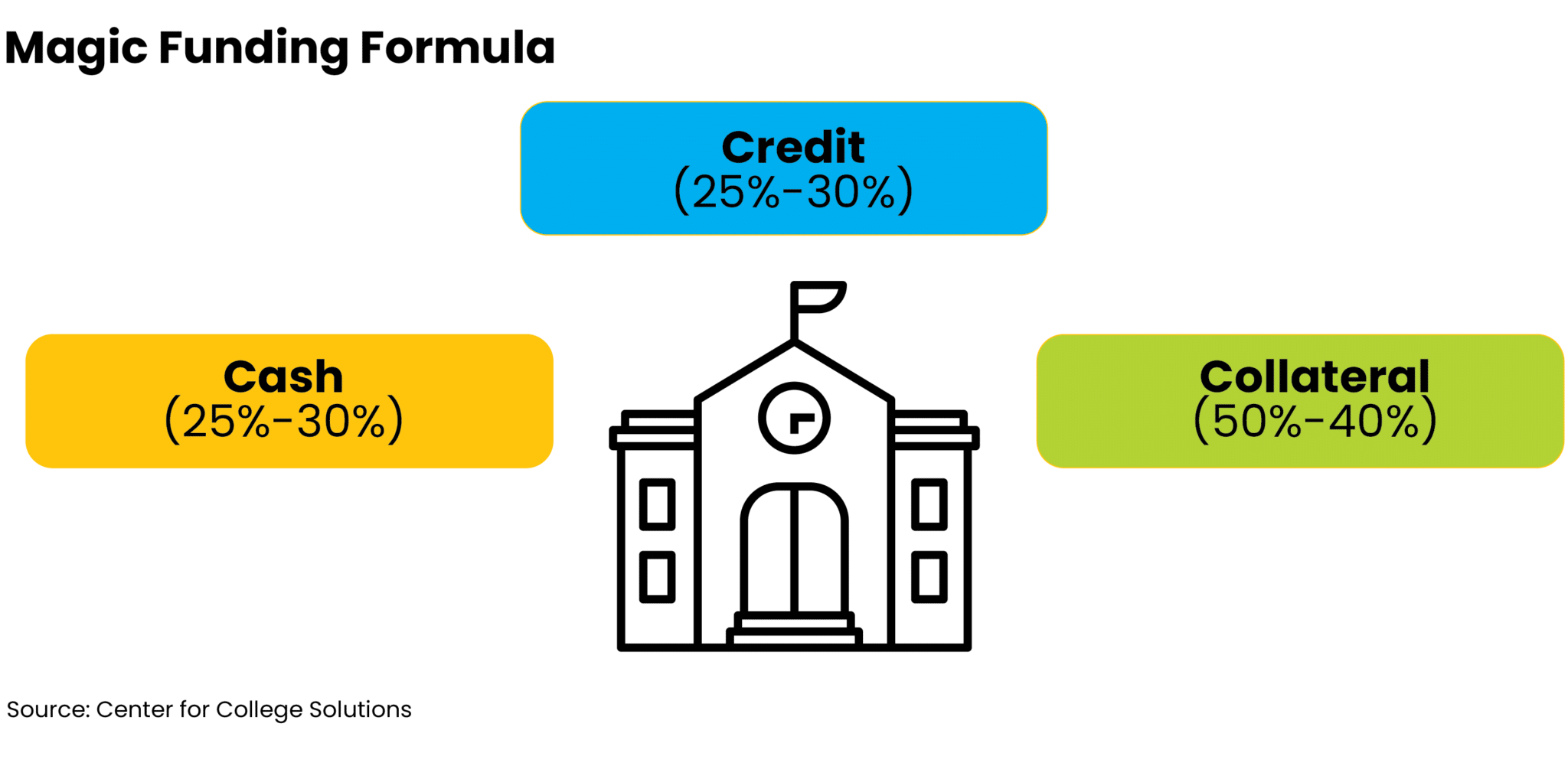

Most households with college-bound students in America would benefit from thinking of college funding as a formula. I use a formula that can be expressed like this: A + B + C = D.

A = Cash (typically 25–30%)

B = Credit (typically 25–30%)

C = Collateral (typically 40–50%)

D = College funding

The formula can be a little tricky because all three elements are not going to be balanced. For example, if you haven’t saved for college, you’ll have to borrow more. Or if your child doesn’t have a good academic FICO® score, they are not likely to earn many discounts.

Cash, credit, and collateral don’t need to be equal parts of the formula. This is where a financial advisor adds value for families. You can help clients “solve for D,” which will be unique to their circumstances.

The percentages I previously noted (25–30% cash, 25–30% credit, 40–50% collateral) are aspirational, but very few families hit these exactly due to their specific situation.

Let’s look at each element of the formula a little more closely.

1. College Cash

This is money that comes from income and assets on the family balance sheet before, during, and after college.

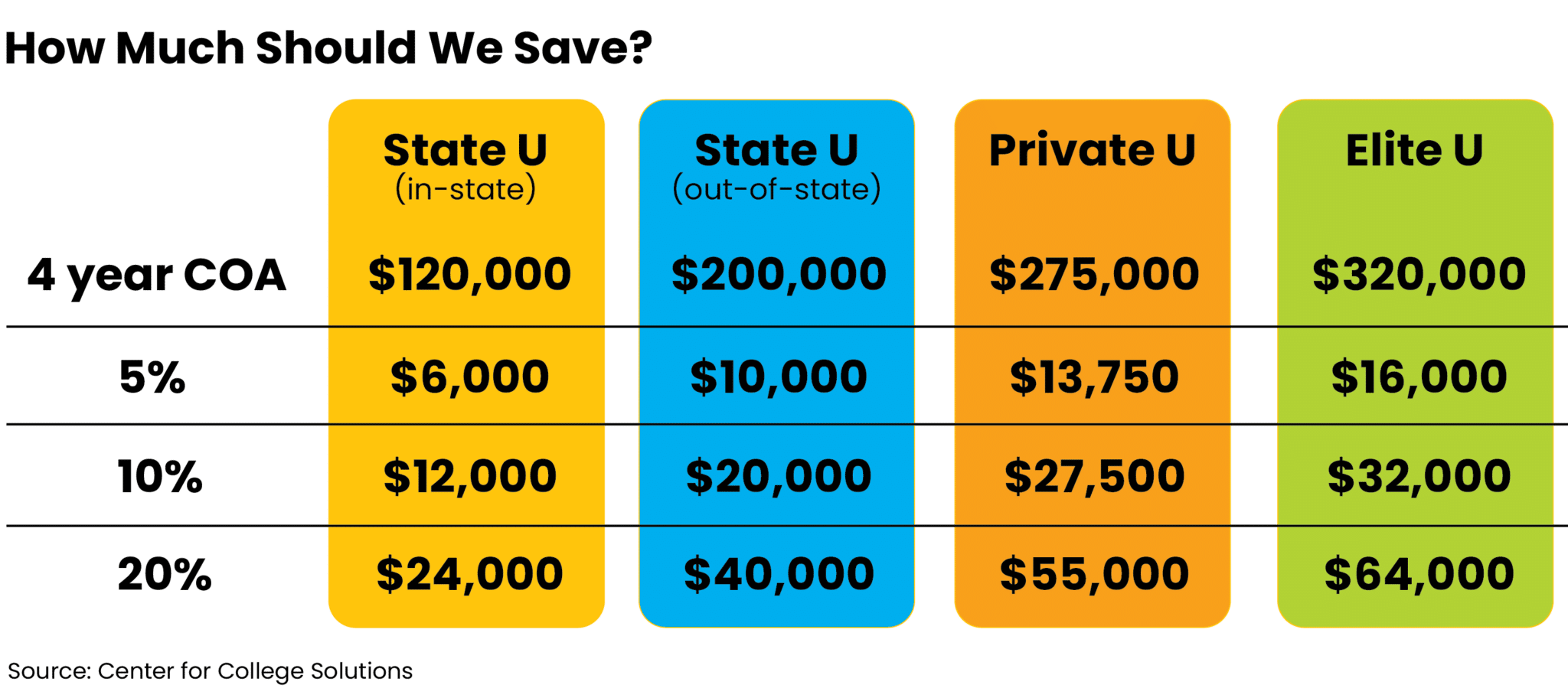

Many families like to set aside some money specifically for college. Think of this as a down payment on the total college purchase price before the student begins their freshman year.

If they haven’t saved the amount suggested by the time your student is about to go to college or aren’t “on track” to reach these targets, tell them not to panic!

A shortfall in the down payment simply leads to a need for more money in a different part of the equation. This is no different than putting a lower down payment on a house and having to pay private mortgage insurance (PMI) or a higher interest rate, resulting in a larger monthly payment.

This payment formula provides guidelines and aspirational goals for each area of the funding formula, not rigid constraints that can’t be tweaked and massaged to accommodate the “real world” financial circumstances of the family.

2. College Credit

Perhaps the most misunderstood and overlooked component of the college funding strategy is that the student could or should pay for an entire year of college, generally defined as “earning through learning.”

Think of it like this: The student’s job is to clip coupons during high school and bring them to the register when it’s time to pay the bill. What does that mean? A student can “clip coupons” by getting good grades and taking honors classes like Advanced Placement (AP) or International Baccalaureate (IB) classes. They can also take a leadership position in a club or extracurricular activity and enroll in test preparation courses, or apply themselves in a manner that improves their ACT or SAT scores. Anything they do to improve their overall academic FICO® score could be considered “clipping a coupon.”

No one ever explains this to families, so most of the time, they suffer from “would’ve, should’ve, could’ve” regrets that prove to be very, very costly.

Not every student can clip the most valuable coupons, so this part of the funding strategy can and should have an impact on the actual college purchased. Some kids won’t bring any coupons to the register, so they end up buying a discounted or generic brand. There’s nothing wrong with that. It will get the job done.

Other kids will have clipped several coupons and are able to buy the more expensive, recognized brand name product at a discount. Good for them! They will have pride of ownership in the purchase.

Understanding how to “clip coupons” is a perfect example of where it pays to get some coaching and guidance.

In addition to “clipping coupons,” parents can earn discounts and points for college simply by living their lives and paying their bills. Think frequent flyer miles for college.

Furthermore, families can take advantage of Sage Tuition Reward Points. You can earn these through your employer, health insurance providers, or participating financial institutions. These points create student scholarships which produce a guaranteed minimum amount of financial aid at member schools. With nearly 500 participating private colleges, imagine being able to pay for 25% of college just by using a particular 529 plan or opening a checking account at a participating bank or credit union.

3. College Collateral

Not all debt is equal.

There’s the “I need to borrow money today but promise I’ll pay it back at the end of the month or over the next few months” kind of debt. Then there’s the “I have an asset (a car, a house, a savings account, an investment account, an insurance policy) that I want to collateralize so I can use other people’s money instead of my own for a specified period.”

The kind of debt the Department of Education extends is a little bit of both. The “rental rate” for using student loan debt is quite reasonable because the government believes a college graduate will get a great job and be able to repay their loans in a reasonable amount of time.

Investing in the right education still holds the promise of exponential return on investment. Because of that, financing the cost of college is generally a savvy strategy, provided the family stays within appropriate funding guidelines.

What Are the Best Financing Options for Buying College?

As we consider the best ways to finance college, I want to point you toward the three most important options: government loans, interest-only loans, and private loans.

Government loans are unlocked by completing the Free Application for Student Aid (FAFSA).

Just like a car loan or mortgage, the FAFSA application process is invasive and challenging. It was recently simplified and will be integrated with the IRS for seamless sharing of tax-related data, so there is less friction in this process than there has ever been.

While not every family completes a FAFSA, I believe it’s a must instead of a should.

The Department of Education backs both subsidized and unsubsidized undergraduate student loans. These loans offer some benefits that simply aren’t available from the private sector, which include no requirement of credit history, a fixed interest rate, loan forgiveness options, and affordable income-driven repayment plans.

Interest-only loans involve collateralizing an asset (such as home equity, marketable securities, or cash value in a permanent life insurance contract) and “renting” access to lump sums of money by making interest-only payments for an extended period.

At some point, the loan does come due. However, the ability to limit the payments to interest only is very cash flow friendly and buys time for families during the college years.

Once the kids are out of school, the lifestyle cash flow that was “offshored” to the college can be redirected toward paying down the principal on these loans.

The most attractive sources of interest-only loans during the college years are:

1. Home equity line of credit (HELOC).

2. Insurance-backed line of credit (credit collateralizing the cash value in a life insurance policy).

3. Asset-backed lending (non-retirement investment account line of credit).

Private loans are “last resort” options for financing college. Not to say they can’t come into play, but the federal student loans and interest-only loans are much more cash flow friendly, so they rank higher on the list.

A Better Future

If we could flip a switch and convince parents to buy college like they buy a house, we would fundamentally change the course of personal finance in America in the time it takes for one class to graduate from college.

Parents would understand their college capital capacity—literally what they could afford to buy college and how they would pay for it.

Families would shop for schools in the right zip code. Students would be where they need to be, studying what they need to learn, and parents could maintain their current lifestyle and stay on track for retirement.

That’s why the M in the MAGIC Method is the most misunderstood element.

Beth V. Walker is a business owner, author, mom to Mack, and financial advisor focusing on helping college-bound students find the right education for the right price at the right school. As a Certified College Planning Specialist (CCPS), she is trained in the complex strategies suitable for reducing a family’s out-of-pocket college expenses, routinely saving families 25%-50% on the cost of college.

Beth is the author of two books, An Employee’s Guide to Stock Options (McGraw-Hill, 2003) and Never Pay Retail for College (Prussian Press, 2017). This article is based on an excerpt from her latest book, Buying College Better.

The formula can be a little tricky because all three elements are not going to be balanced. For example, if you haven’t saved for college, you’ll have to borrow more. Or if your child doesn’t have a good academic FICO® score, they are not likely to earn many discounts.

The formula can be a little tricky because all three elements are not going to be balanced. For example, if you haven’t saved for college, you’ll have to borrow more. Or if your child doesn’t have a good academic FICO® score, they are not likely to earn many discounts. If they haven’t saved the amount suggested by the time your student is about to go to college or aren’t “on track” to reach these targets, tell them not to panic!

If they haven’t saved the amount suggested by the time your student is about to go to college or aren’t “on track” to reach these targets, tell them not to panic! Beth V. Walker is a business owner, author, mom to Mack, and financial advisor focusing on helping college-bound students find the right education for the right price at the right school. As a Certified College Planning Specialist (CCPS), she is trained in the complex strategies suitable for reducing a family’s out-of-pocket college expenses, routinely saving families 25%-50% on the cost of college.

Beth V. Walker is a business owner, author, mom to Mack, and financial advisor focusing on helping college-bound students find the right education for the right price at the right school. As a Certified College Planning Specialist (CCPS), she is trained in the complex strategies suitable for reducing a family’s out-of-pocket college expenses, routinely saving families 25%-50% on the cost of college.