If it’s June, it must be time for wedding bells across the land. But what’s a couple likely to do if they can’t afford all the extras or exotic locales that can make getting hitched such a memorable event?

Call their friendly banker or non-banking financial company (NBFC), or course

The wedding-loan market has become very lucrative because many couples pay not out-of- pocket for the big day but with borrowed money.

A report published in May by Allied Market Research about lending options reveals that wedding loans reached $11.63 billion in 2023 globally. The researchers project that figure will double in 10 years, to $23.26 billion. Two-thirds of these loan revenues come from North America, with borrowing growing in the Asia-Pacific region, says the report.

That’s serious money for what used to be considered a once-in-a-lifetime happening. But with the national divorce rate for women at nearly half the national marriage rate in 2021, the latest data from the U.S. Census Bureau, there’s even more potential for borrowing. That’s because there are those who try marriage again, often with the expensive bells and whistles intact at their next wedding.

Although the U.S. remarriage rate has been declining, 515,783 males and 488,707 females remarried in 2021, estimates the National Center for Family & Marriage Research at Bowling Green State University.

A Pricey Three-Month Marriage

Take widow Theresa Nist, 70 of New Jersey, and widower Gerry Turner, 72 of Indiana: They met on ABC-TV’s “Golden Bachelor’’ show, and married Jan. 4, 2024 in a destination wedding held at a resort in California. Reports in Wedding Spot say ABC picked up much of the wedding reception cost — 125 guests at $250 a head, or about $31,000 — and paid for Nist’s Badgley Mishka gown and flying guests to the resort .

On April 12, 2024, Turner and Nist announced they were divorcing. They’re not alone: Divorce.com estimates that a marriage breaks up every 46 seconds in the United States.

Premarital Counseling Could Save Money

Thomas R. Sobolewski, a CFP professional based in Amherst, N.Y. has some pithy thoughts on the subject of marrying expensively then divorcing.

“I work as part of a divorce mediation group, and one of our pet peeves is that people spend a fortune (including borrowed funds) on an outsize wedding, and NOTHING on preparing each other for married life,’’ Sobolewski says.

“By the time they come to see us it’s typically too late, and we’re left thinking that they might not be seeking a divorce at all if they’d spent a couple thousand on premarital counseling up front, as opposed to $20,000 or more on a one-day party (and then thousands more on a divorce),” he adds.

“So, borrowing money for a wedding? Absolutely not, unless it’s both modest and necessary. Unlike the couple who just talked to me about their ‘destination wedding’ in Tuscany, who expect their not-rich family to spring for their own airfare and hotel,’’ Sobolewski says.

Reality Check

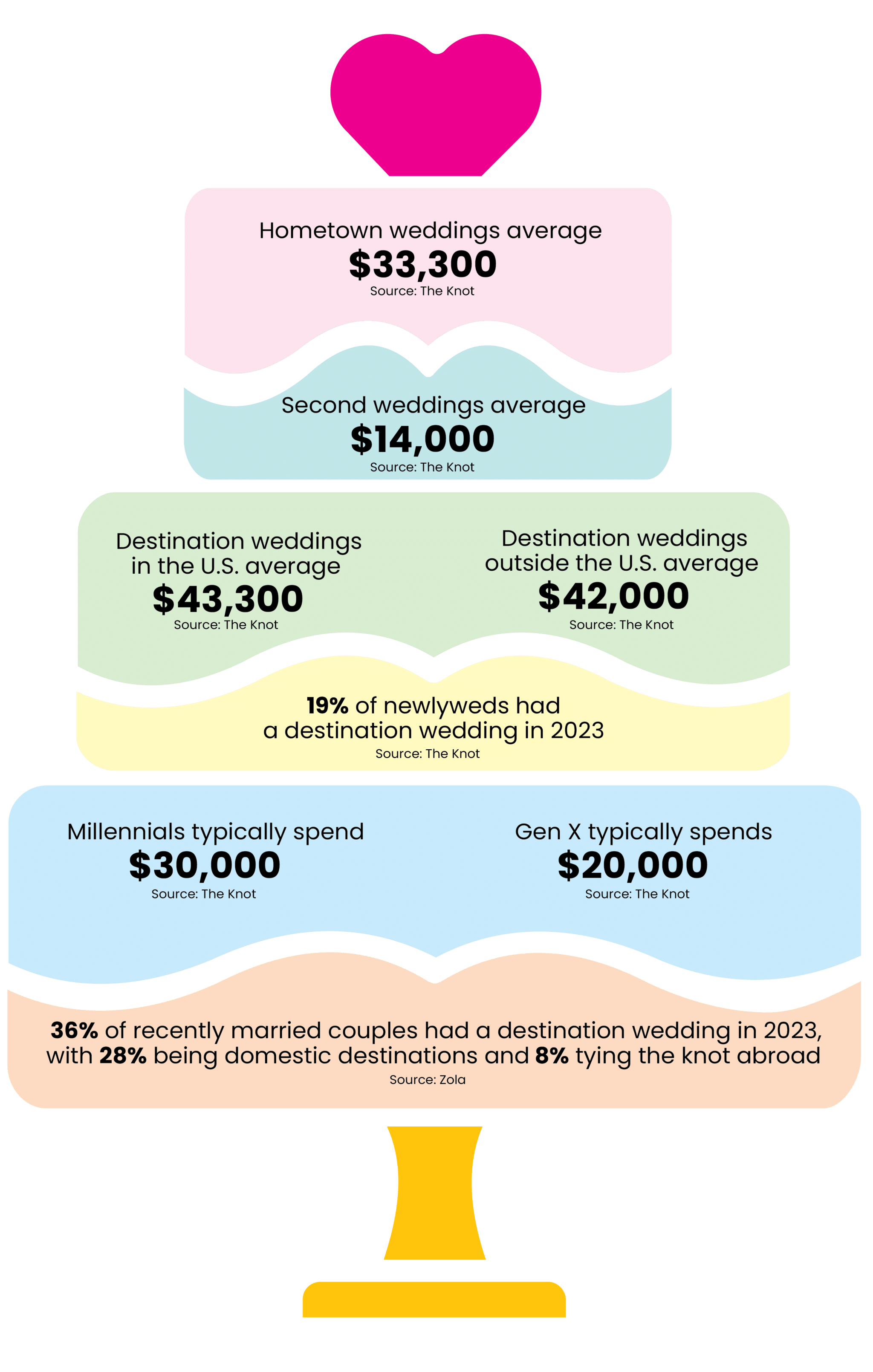

Destination weddings are driving up the wedding loan market, the Allied Market Research report says, so that the average wedding in the United States costs $30,000.

The Knot, a wedding-planning website, says that the most popular destination wedding locales for U.S. couples are Hawaii, Mexico, and Napa Valley, California, with Maine, Newport, R.I. and Arizona growing more popular. Italy, where newlyweds Nist and Turner honeymooned, is also a strong wedding destination, The Knot reports.

Even traditional weddings held locally are costing more, Allied Research Market’s report shows.

According to Money magazine, the most expensive states to get married in, on average costing $40,000, are New Jersey, New York State and Long Island, eastern Connecticut, Massachusetts and Vermont. It costs upwards of $39,000 on average to get married in coastal states such as California, Maryland, Maine, Delaware, Louisiana, Florida and South Carolina. New Jersey leads the pack at more than $50,000 a wedding, on average. Weddings are least expensive in Utah, Oklahoma and Kansas, at $16,000, reports Money magazine.

Putting a Plan in Place

Michelle Crumm, a CFP professional based in Ann Arbor, MI, says weddings can be a burden, not a blessing, if they’re not carefully financed.

“I read that the average cost for a wedding now is $96,000. For my clients and most Americans, that is out of reach for them to spend without severely impacting their retirement plans. We put a plan in place that allows them to contribute to the wedding,” she says.

“We start with assessing their financial health to make sure that any money they give their children for the wedding does not impact the date they want to retire or how much they want to spend in retirement,’’ Crumm says.

There are ways to lower the costs of a wedding without crimping the style of the event, she adds.

“After assessing their financial health, we look for alternatives to be able to help guide their children to different venues, alternative dates that are less popular, and less expensive food so that it helps the children cut costs,” she says.

Eye on Retirement

When Crumm’s clients take her advice, they avoid using other’s people money to finance the event.

“I encourage them not to borrow for the wedding. Borrowing means do not get a line of credit, personal loans, or charge anything on the credit card that can’t be paid off at the end of the month,’’ she says.

“We discuss the long-term financial consequences of going into debt for a wedding. We discuss open communication with their children. I think letting them know what the budget is and sticking to it is the best plan for success. I also speak with the children to let them know how we came up with the budgeted amount for their parents to contribute,’’ Crumm says.

One of her client couples, both spouses age 54, have a $2 million net worth. Their daughter, 23, a recent college grad getting married this season, has a good job, earning $80,000 this year. The starting budget for the wedding topped $90,000, of which the couple had saved $65,000. The couple needed to stay in budget because they want to retire within five years, says Crumm, adding that’s “less time to recover from overspending on major life events.”

“We focused on retirement vision which helped them say ‘no’ to overspending on wedding,” she says. The clients saved $25,000 by moving the event to a venue on the west side of Michigan instead of the east side of the state (Detroit area). “They also reduced the guest list and made wedding and reception earlier in the day which saved money on food,” Crumm says.

Budget-breaking Mistakes

A survey from the Consumer Reports National Research Center found that nearly two-thirds of the newlyweds who budgeted for their reception said they overspent by at least 20%. Inflation — including higher food costs that wedding vendors are passing on to clients — is also pumping up the cost of celebrating.

Among borrowing options, three-quarters of wedding loans are at fixed interest rates and about two-thirds of the loans are made with traditional banks, according to the Allied Market Research report.

Floating interest rate loans, which can be cheaper if interest rates drop, and NBFCs, which offer online and digitalization borrowing, are becoming more popular as more couples emerge who prefer online rather than in-person transactions, the Allied Market Research report finds.

Important Questions

Neighborhood bank or AI loan, one planner nixes the whole idea of borrowing to tie the knot.

Paul Monax, CFP, Littleton, Colo., preaches to couples just starting out that they should consider the financial consequences of a lavish wedding versus the long-term needs of a marriage.

“It’s Ok to use debt, but it should always be a conscious decision and one that you fully understand the ramifications of and how it will impact your future and the rest of the pieces of your planning for that future,’’ Monax says.

“Keep in mind if you are going to use debt to fund your wedding, then you are then going to have to give up something else in the future to cover those payments plus interest,” Monax says. “Is that wedding and the related expenditure a part of your plan? Do you want it to be? Should it be?”

In a four-decade career in journalism, Eleanor O’Sullivan has reviewed many books on best practices for financial advisors, has written for Financial Advisor and the USA Today network, and was movie critic for the Asbury Park Press.

According to Money magazine, the most expensive states to get married in, on average costing $40,000, are New Jersey, New York State and Long Island, eastern Connecticut, Massachusetts and Vermont. It costs upwards of $39,000 on average to get married in coastal states such as California, Maryland, Maine, Delaware, Louisiana, Florida and South Carolina. New Jersey leads the pack at more than $50,000 a wedding, on average. Weddings are least expensive in Utah, Oklahoma and Kansas, at $16,000, reports Money magazine.

According to Money magazine, the most expensive states to get married in, on average costing $40,000, are New Jersey, New York State and Long Island, eastern Connecticut, Massachusetts and Vermont. It costs upwards of $39,000 on average to get married in coastal states such as California, Maryland, Maine, Delaware, Louisiana, Florida and South Carolina. New Jersey leads the pack at more than $50,000 a wedding, on average. Weddings are least expensive in Utah, Oklahoma and Kansas, at $16,000, reports Money magazine.