Thinking about retirement can be exciting. It’s an opportunity to travel more, take up new hobbies and spend more time with loved ones. Yet planning for retirement can also be stressful with many complex questions: Have I saved enough? How long do my assets need to last? What about health insurance? Am I ready to leave the workforce and my career?

What’s the best age to retire?

While good saving and investing habits are critical components of retirement lifestyle and income, one of the most powerful tools participants have is deciding at which age to retire. Working longer has some obvious benefits, such as salary, employer benefits coverage and more time for assets to grow. Other benefits may be less apparent, such as the impact on Social Security payments and how a later retirement date can impact withdrawals from retirement accounts.

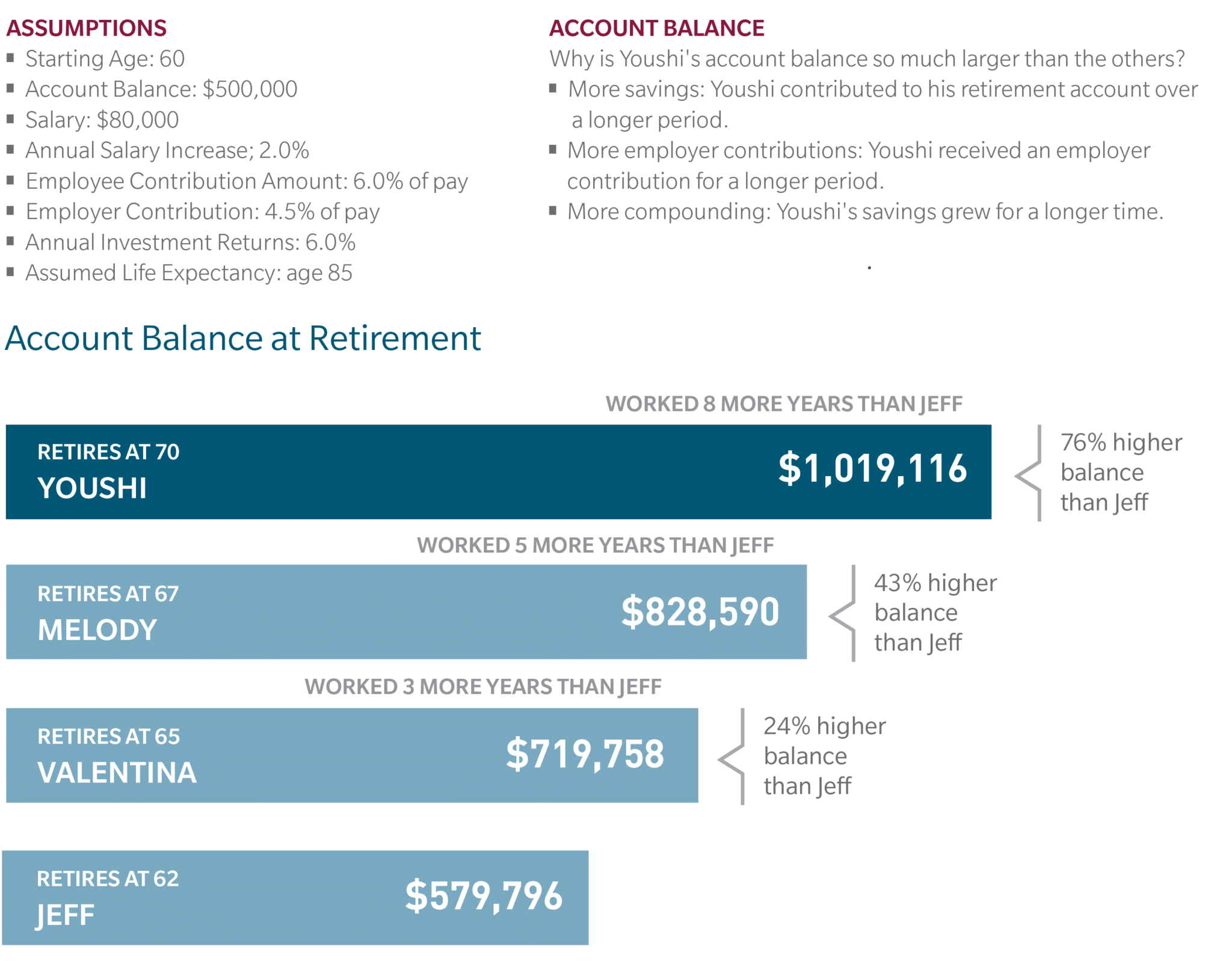

The hypothetical example below shows the impact that working longer could have on retirement savings. We looked at four participants, all age 60 and with a 401(k) account balance of $500,000. Each is projected to retire at a different age, and as you can see, working longer could have a significant impact on account balances. Youshi, Melody and Valentina saved more (both via their savings and employer contributions) than Jeff, and their savings had more time to grow.

Translating account balances into retirement income

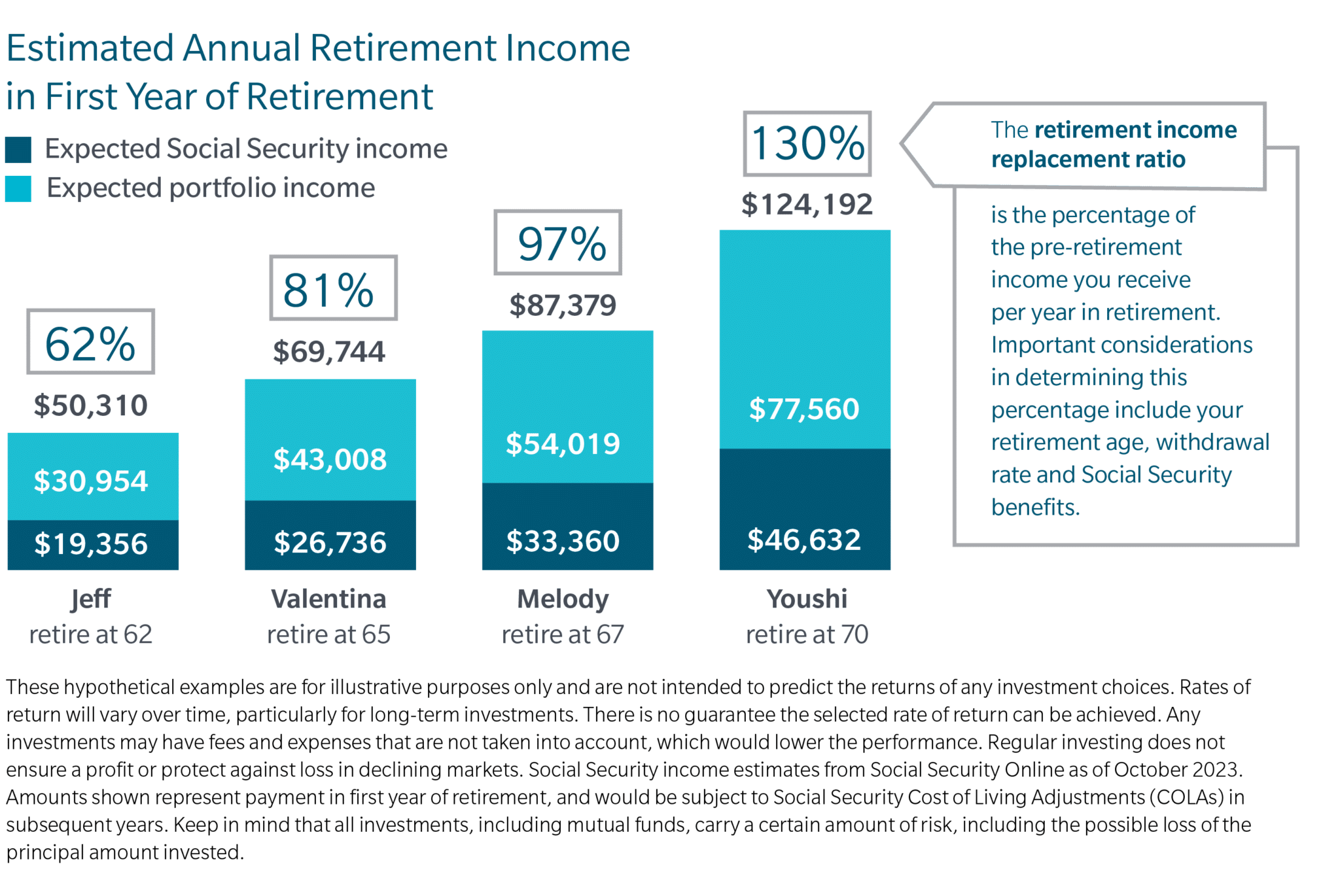

Account balances are only one part of the story. What really matters is how much income a person will have in retirement along with expenses. Understanding Social Security and its impact on retirement income and the surviving spouse is critical. For many prospective retirees, the Social Security Full Retirement Age (FRA) is 67. 1 Social Security benefits can begin at 62; however, claiming Social Security before your FRA reduces benefits. 2 On the other hand, after you reach FRA your retirement benefits grow by 8% per year until age 70. 3 If you are married and you are the higher earner, at your death, your surviving spouse may step up to the benefit you were receiving.

Another important factor in the retirement date equation is Medicare health care coverage. Medicare coverage is available at 65. Retiring before age 65 may mean paying health care costs out of pocket.

Going back to our four hypothetical pre-retirees, we estimated their potential retirement income from their 401(k) balances (bright blue bar in chart below) and added in their Social Security benefits (dark blue bar). Next, we determined the percentage of their pre-retirement income that would be replaced by this income (gray boxes), often called a retirement income replacement ratio. Not surprisingly, working longer and letting Social Security benefits grow could result in a significant increase in annual retirement income and a corresponding increase in income replacement at the later retirement ages.

Key takeaway

Deciding when to retire is a personal decision based on many factors, such as health, financial goals and needs, and working longer is not always viable. However, those who have some flexibility may want to consider weighing the pros and cons of working in retirement as a part of the retirement planning process.

1Social Security Full Retirement Age (FRA) is age 66 for anyone born 1943 to 1954. It increases by two months for every year from 1955 to 1959. FRA is age 67 for anyone born in 1960 or later.

2Social Security retirement benefits are reduced by 6.67% per year for the first 3 years prior to FRA and 5% per year for the next 2 years, resulting in a total reduction of 30% at age 62 for a retiree with an FRA of 67.

3Social Security retirement benefits are increased by 8% per year after FRA, resulting in a benefit increase of 24% at age 70 for a retiree with an FRA of 67.

The views expressed are those of the author(s) and are subject to change at any time. These views are for informational purposes only and should not be relied upon as a recommendation to purchase any security or as a solicitation or investment advice from the Advisor. No forecast can be guaranteed.

MFS does not provide legal, tax, accounting or Social Security advice. Individuals should not use or rely upon the information provided herein without first consulting with their tax or legal professional about their particular circumstances. Any statement contained in this communication (including any attachments) concerning US tax matters was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code. Contact the Social Security Administration at 1-800-772-1213 or go to www.ssa.gov to determine the benefits that may be available to you and your spouse.

MFS FUND DISTRIBUTORS, INC., MEMBER SIPC, BOSTON, MA MFSP_FLY_980302_10_23 49382.5

Translating account balances into retirement income

Translating account balances into retirement income

Key takeaway

Key takeaway