If you were told another financial advisor’s book of business is available for purchase and produces almost $1 million in annual revenues, what would your first impressions be and what additional questions would you have?

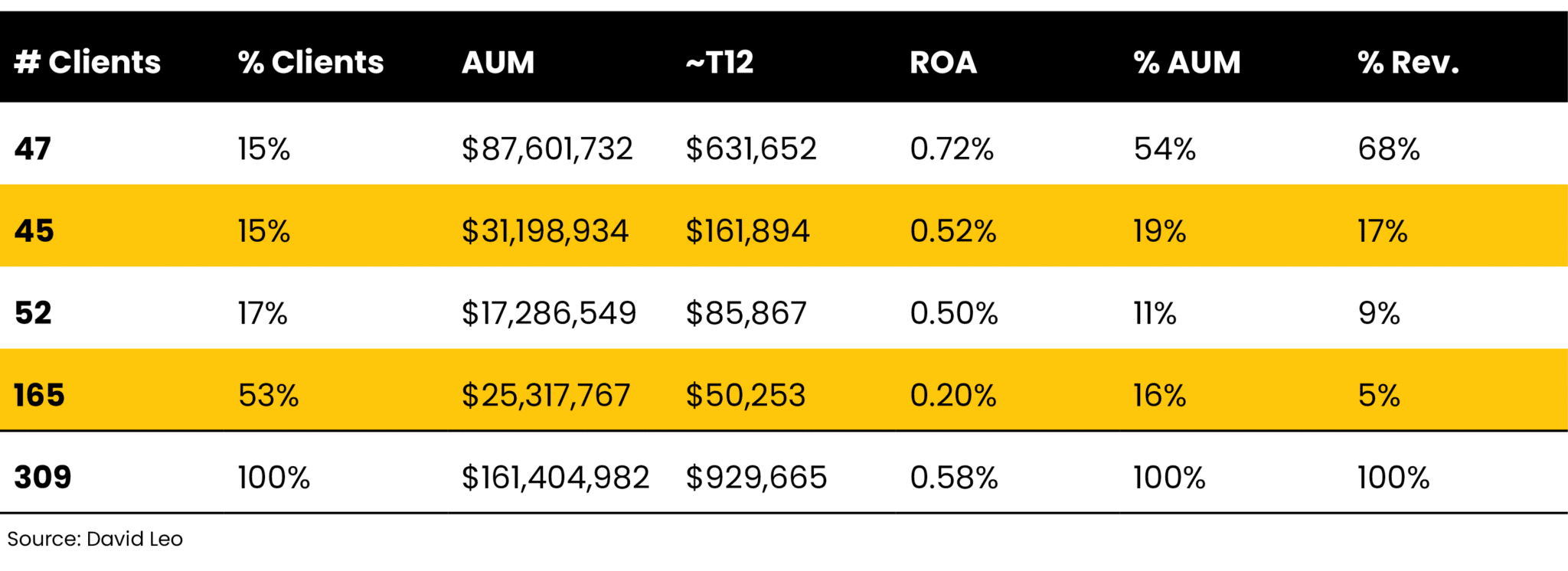

Let’s say you were also told the book has 309 clients, $161.4 million in assets under management (AUM) and $929,665 in trailing 12-month revenues (T12).

If you’re a solo practitioner, you may think this is too many clients for you to effectively manage while providing high levels of service across the book. You can also see that the return on assets or velocity is about 58 basis points ($929,665/$161.4 million ) This is below industry average, which tends to be about 1% of AUM (100 basis points).

This scenario calls for more data and it should also raise more questions.

A Case Study

This isn’t just a hypothetical situation. When one of my clients considered merging with another advisor in a different state, I suggested looking at that advisor’s book of business so we could learn more. This enabled us to develop a set of hypotheses and additional questions to ask the advisor.

I’m sharing this true story with you to show you how to identify red flags and potential hidden opportunities within books of business when a limited set of data is initially provided.

For example, if an advisor’s book shows many clients with a low return on assets (ROA), as was the case here, it might that suggest the clients have transactional accounts. These accounts generate income through commissions, which could lead to unnecessary trading and unprofitable clients. In contrast, managed accounts provide ongoing, constant fees and often show significantly higher valuations. Low ROA numbers could also mean that clients aren’t being offered financial planning and other services that are more typical with managed accounts.

A big request

I encouraged my client to ask his potential partner to provide a list of clients with a sequence number only ( i.e., no client names or contact information) and additional data. My client was able to get approximate trailing 12-month revenues and AUM data, by client. We were then able to calculate return on assets and group the clients by revenues, assets or profitability.

What was missing

Although AUM is an important factor, we were missing four or five more subjective factors about clients that significantly contribute to the value of a book of business. This includes whether a client:

- Enjoys the relationship. The quality of the relationship between you and your client is a binary decision — either good or not good. Advisors and teams know the type of relationships they have with most of their clients, or at least those they wish to continue to work with.

- Takes your advice. Do they listen and follow your advice much of the time?

- Serves as a source of referrals. How many clients have a network of potential clients they can introduce you to and do they take the time to do so?

- Can potentially maintain or grow their value for your business. If clients are in the accumulation stage and manage their expenses rationally, this is a positive. If clients are planning large expenditures or are withdrawing assets and will significantly reduce their AUM in a small number of years, this is a negative.

Positive factors make a client more valuable to the business while negative factors reduce the client’s value.

Assigning Tiers

To further evaluate the potential of the clients held in this other advisor’s book of business, we decided to break them into four tiers by revenue generated over the trailing 12 months.

Tier 1 = $5,000 or more.

Tier 2 = $2,500 to $4,999.

Tier 3 = $1,500 to $2,499.

Tier 4 = Less than $1,000.

We elected to evaluate clients by revenue because the business had some clients who generated “good” or “very good” revenue but didn’t show any assets. That’s because their assets were on the books of their 401(k) provider, not the advisor servicing the accounts.

We also wanted to ask the advisor about his clients who had “good” AUM but generated low revenues. Perhaps these assets belonged to new clients for whom fees had not yet been received or recorded, nor transactions yet executed. Or perhaps these clients had passed away and their estates had not yet been settled. We wanted to understand the potential of these low-revenue-generating clients.

Here is the breakdown by tiers:

Observations, Hypotheses and Questions

Looking at the data, we made some observations, developed hypotheses and generated follow-up questions for our client to ask when deciding whether or not to purchase and merge this book with their own.

Observation 1

There is a relatively normal distribution of clients across tiers. In brief, 73% of client assets produce 85% of client revenue, 30% of clients provide that 85% of revenue and 15% of client assets produce 68% of client revenue.

Questions to pose about the 47 top-tier clients:

- Seventy-two basis points for million-dollar-plus clients (average of $1.86 million) is acceptable considering some stagnant assets and fixed income components of a portfolio. How many of these clients are fee-based and what is the average fee by tier?

- Can you detail the relationships and longevity of each of these 47 clients using the subjective factors above?

- What is the service model for these clients and the number of annual proactive and reactive contacts? Proactive contacts include the annual, semi-annual or quarterly meetings advisors provides as part of their service strategy, plus any “check-in” call on months where no review meetings are scheduled. Reactive contacts refer to returning client calls, preferably the same day.

Advisors should also ask these three questions about clients in Tiers 2 through 4, plus some additional questions that we’ll discuss in a minute

Observation 2

In Tier 2, 15% of client assets produce only 17% of client revenue. Meanwhile, 52 basis points (Tier 2’s average ROA) for clients with an average of $693,000 in assets ($31.2 million divided by 45 clients) is considerably below average. Assuming we could bump Tier 2’s average ROA by 20 basis point to match Tier 1’s ROA, this would yield another roughly $62,000 in revenues.

Observation 3

Of the 217 low-producing clients (Tiers 3 and 4), Tier 3 has 52 clients with an average AUM of $332,000 ($17.3 million/52 clients). Their 50 basis-point ROA is also considerably below average. An additional 20 basis points would yield another roughly $35,000 in revenues for the tier. Tier 4 has 165 clients, with an average AUM of $153,000 ($25.3 million/165). The average 20 bps is extremely below average. An additional 50 basis points (approaching Tier 1’s ROA) would yield another roughly $127,000 in revenues.

I don’t want to focus solely on the amount of money being left on the table but these are the types of questions one should ask when evaluating a book of business.

It’s also possible that Tier 3 and Tier 4 clients are being underserviced. This would be indicated by low retention rates and overt complaints. Addition questions to pose about clients in these two bottom tiers:

- What is the retention rate for these clients?

- How many of these clients are first year clients? (This would lower the average bps.)

- Is there a formal feedback process for all clients?

Meanwhile, 27 clients in the lowest tier report no assets under management although several are 401(k) plans being managed and/or serviced by the advisor, not individual clients. So, another question to ask is, are these 401(k) plans productive?

Observation 4

Additional data we received shows that 99 clients have AUM less than $100,000. Collectively, they represent less than $4 million in AUM and less than $25,000 in the firm’s total trailing-12-month revenue. Questions to pose about this group of clients:

- How many are related to top clients?

- Why are they accepted as clients?

- Should these clients be moved to a service center or a “Vanguard” or other “low-end provider?”

Although as many as all 165 clients in Tier 4 may be unprofitable, better management could yield excellent opportunities over time. Here are some additional questions to pose:

- Do you see potential with these clients?

- Have you considered hiring a junior financial advisor to work with these clients? Why or why not?

Better Service, More Referrals

As you can see, there are a number of ways to ask for and analyze data. It’s also a balancing act deciding which clients are worth retaining.

Additional Reading: Working On and In Your Business

The advisor my client has held exploratory talks with has done a good job attracting and building a book of business from the ground up. Strong technical skills helped him acquire more than $160 million in AUM and more than 300 clients.

Although it would be time consuming to convert most of that advisor’s clients to a higher ROA, this is often easier than generating similar growth through acquiring new clients and assets. A number of the advisor’s $1 million-plus clients might be able to provide referrals. Lower tier clients who receive good service and understand how much more their advisor can help them may also provide referrals. In this case study, we hypothesize that there is as much potential in introductions and referrals as there is in increasing ROA across the advisor’s book.

We also believe his book would benefit from better management and a high-value service model. In a future article, we’ll examine what a high-value service model could look like. (Bear in mind that implementing one may require additional staff and other costs — so that’s something that an acquiring or partnering advisor must also factor in.)

By asking questions like the ones posed in this article, you can begin to evaluate and optimize your book of business or decide whether it’s worth moving forward with buying or merging with another advisor’s book. In addition to these primary questions, there are many more questions that can be raised about the quality of the book. Further analyses could reveal additional red flags and opportunities.

David Leo is the founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant and trainer to financial professionals. David is an experienced business manager who works solely with financial advisors, planners and firms who want to organize, structure and grow their businesses by attracting, servicing and retaining affluent clients. He can be reached at David@CoachDavidLeo.com, 212-598-4229 (office) or 917-379-1249 (cell). To contact him for a book analysis, go to www.calendly.com/davidileo.