With gifting on everyone’s mind, now is a great time to discuss 529 plans with clients. Plus a new federal law provides a major incentive for grandparents.

Saving for college remains a top priority for families. And while parents are typically the primary savers, other family members, like grandparents, are also looking to help offset the cost of college.

With gifting on everyone’s mind right now, this is a great time to discuss 529 plans with clients, especially those with grandchildren. 529s are a strong tool to save for college and can be used for gifting in many ways.

Inviting family and friends to give

As you know, 529 plans are tax-advantaged savings accounts designed for educational expenses. 529s come in two basic types: 529 savings (investment) plans and 529 prepaid tuition plans. Both types offer remarkable incentives and benefits that continue to improve over time.

If some of your clients are already saving in a 529 plan, encourage them to use eGifting. This feature exists in nearly all 529 plans and lets account owners invite family and friends to contribute to their account. Some plans, like Private College 529 Plan, also provide social sharing links for sending invites over group text and email.

If clients open an account with Private College 529 Plan, they can use eGifting as soon as the enrollment process is complete. And that’s great news with the holiday season upon us.

If clients familiarize themselves with the gift contribution process now, they’ll be in a good spot to use the feature throughout the year. There’s never a shortage of reasons to give and milestones to celebrate with 529 gifting.

Opening a 529 account as a gift

Some clients may want to take gifting one step further and open their own account(s). This option is especially appealing to grandparents. Since a child can be the beneficiary on several accounts under the same plan, there’s plenty of room to be generous.

One of the changes in the FAFSA Simplification Act impacts how non-parent 529 plans are treated in the financial aid formula for federal student aid. In prior years, distributions from 529 plans owned by grandparents (or anyone other than a parent) were counted as untaxed student income on the FAFSA form. But starting with the 2024-2025 academic year, these accounts will no longer count against students and impact financial aid eligibility. This is a major incentive for family members, like grandparents, to save for the children in their family, either alone or together with the parents.

It’s important to note that this FAFSA change does not impact how 529 assets are reported on the CSS Profile, a second financial aid form used by many private colleges and universities to award scholarships and other non-federal aid.

Additional perks of 529 plans

The benefits of grandparent-owned 529 accounts don’t end with favorable FAFSA treatment. Other advantages include:

1. Gift tax exclusion

Anyone can gift up to $17,000 per beneficiary in 2023 without filing a gift tax return. And the amount doubles for married couples filing jointly. That’s excellent news for grandparents since 529 contributions are considered completed gifts. Even if clients exceed the annual gift tax exclusion amount, they most likely won’t pay taxes. The excess can be deducted from their lifetime estate and gift tax exemption – $12.9 million in 2023.

It should be pointed out that the annual gift tax exclusion amount includes all gifts given to a person in a year, not just 529 contributions.

Although there are no federal tax deductions for saving in a 529 plan, there could be other tax savings depending on where clients live. Several states offer tax deductions for residents who contribute to their state-owned 529 plan. Residents in the following nine states may be eligible for a state income tax benefit regardless of which plan they contribute to, including Private College 529: Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, and Pennsylvania.

2. Superfunding

A special rule in the Internal Revenue Code allows anyone to superfund a 529 account up to five times the annual gift tax exclusion amount — $85,000 per beneficiary in 2023 or $170,000 for married couples filing jointly.This lump sum is treated as if clients are giving money evenly over five years, so their lifetime estate and gift tax exemption isn’t reduced. To superfund a 529, clients must file a federal gift tax return (Form 709).

3. The option to prepay

For clients looking to minimize investment risk, a prepaid 529 plan might be the best option. As the name suggests, these 529 plans allow college savers to prepay all or part of tuition and mandatory fees at a predetermined rate, protecting against tuition inflation. The state or colleges sponsoring the plan guarantee the prepaid dollars.

Currently, there are nine prepaid plans accepting new enrollments. Eight plans are sponsored by states, while Private College 529 Plan operates nationwide with a network of nearly 300 colleges and universities.

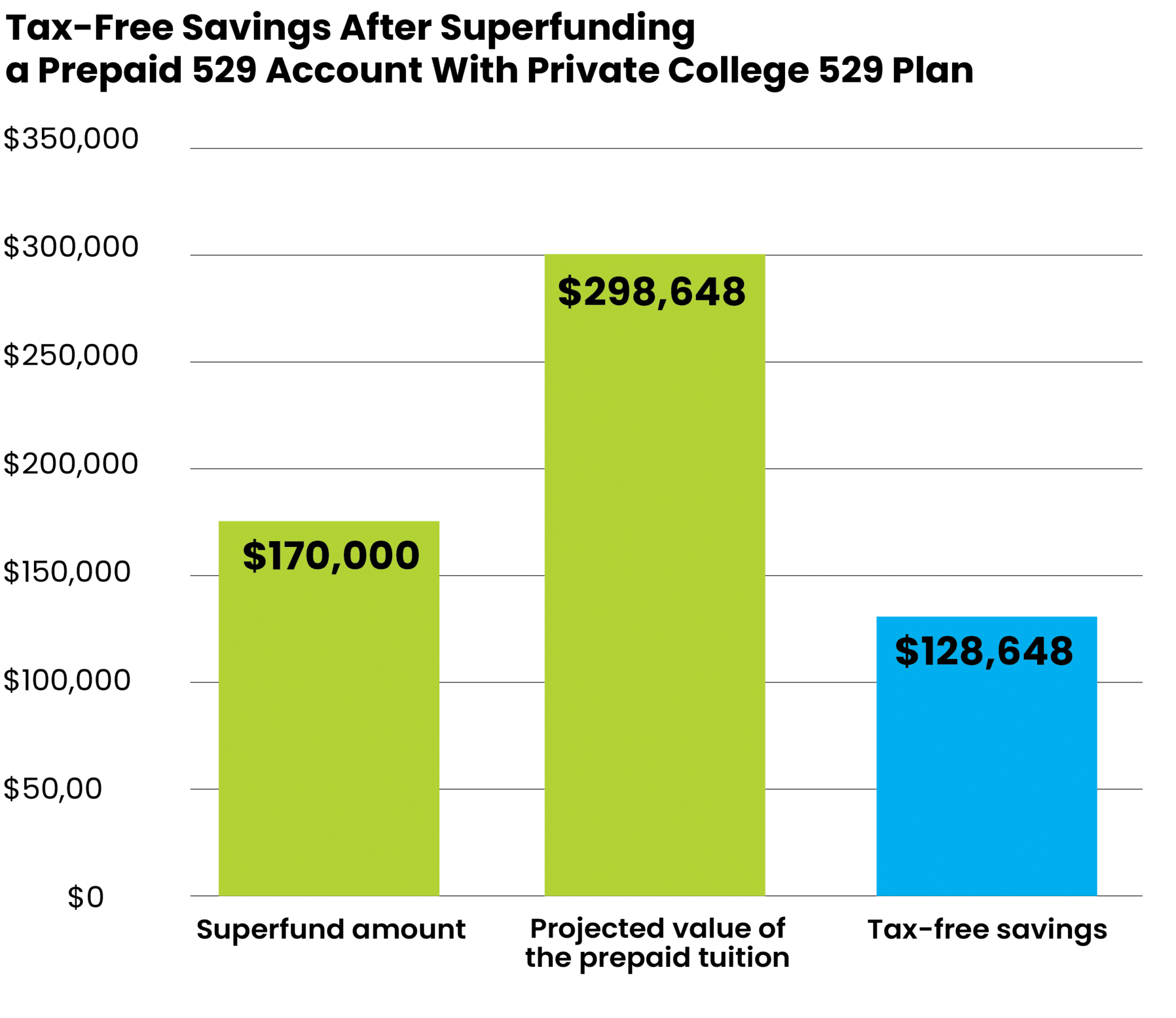

If clients open a prepaid 529 account and superfund it, just imagine the savings. Consider the following example.

Let’s say a grandparent opens a Private College 529 account for their 5-year-old grandchild in 2023 and superfunds the account with $170,000. By the time the child is ready to enroll in college in 2036, the account is now valued at $298,648. *

What the grandparent has done is save $128,648 (tax-free) on the cost of college while purchasing nearly 4 years (3.62) of tuition and mandatory fees. **

* Assumes a 4% tuition and fee increase year to year. ** Based on the average tuition and mandatory fees for all colleges participating in Private College 529 Plan ($46,903 in 2023). Example is for illustration purposes only.

4. Estate planning tool

Owning a 529 account allows clients to move finances out of their estate while still retaining control of the assets. Because 529 contributions are considered completed gifts, they’re no longer part of an estate and, therefore, excluded from federal estate tax.

Giving the gift of education

The big takeaway is that clients don’t have to save for their children’s college education alone. There are options that allow family members to help. For clients who are grandparents, there is the added benefit of providing financial support for younger generations while protecting their gifts from tax liability. As a financial advisor, you can help your clients understand what’s possible and the best tool for the job.

Disclosure: CollegeWell and Private College 529 Plan (the Plan) are established and maintained by Tuition Plan Consortium, LLC (TPC). This material is provided for general and educational purposes only, and is not intended to provide legal, tax, or investment advice, or for use to avoid penalties that may be imposed under U.S federal tax laws. Intuition College Savings Solutions, LLC (Intuition) is the Plan Administrator. Participation in the Plan does not guarantee admission to any college or university. Tuition Certificates are neither insured nor guaranteed by the FDIC, TPC, any government agency, Intuition or their respective subcontractors and affiliates. However, Tuition Certificates are guaranteed by colleges and universities solely for tuition and mandatory fee credits. Tuition Certificates must be held for at least 36 months from the issue date before they can be redeemed to pay for tuition at a participating school. The issue date is the first date during a plan year that a purchase of a Tuition Certificate is made. Please read the Disclosure Statement and Enrollment Agreement carefully and consider your financial objectives and risks before purchasing a Tuition Certificate. TPC, Intuition and their respective subcontractors and affiliates do not provide financial, legal or tax advice. Contact your attorney or other advisor regarding your specific legal, investment or tax situation.

Private College 529 Plan assets can be used to pay any qualified expense at any college or university, public or private. The tuition guarantee applies only to participating institutions. Outside the network, the value of the account is calculated as your total contributions adjusted for net investment returns subject to a maximum increase of 2 percent per year or a maximum loss of 2 percent per year, compounded annually. If the refunded amount is not used to pay qualified education expenses, the earnings portion will be subject to federal income tax and an additional 10 percent penalty. See Disclosure Statement for details.