Editor’s note: The authors, a financial wellness expert and a financial advisor, collaborated on this article to proactively support Mental Health Month celebrated in May. Their goal is to raise awareness around cognitive and behavioral health and reduce the stigma too often attached to mental health issues and diagnoses. They also want to help financial advisors understand the impacts mental health can have on financial planning and share tips advisors can use to help clients.

Keena Pettijohn and Lawrence Sprung

Both of us know firsthand the trauma and financial devastation that mental illness can inflict on families.

Keena: I grew up with a mentally ill father, but it wasn’t until now that I have been willing to share my personal story, one that I kept secret for 53 years. As I look back on my childhood, I now understand the financial devastation my family endured as a result of the “breadwinner’s” mental illness — a mother and two young children lost everything with no one and nowhere to go.

Larry: Losing my 24-year-old brother-in-law to suicide opened my eyes to how devastating mental illness can be. In response, my wife and I have become mental health advocates. We feel by sharing Keith’s story we can open a dialogue and create a safe place for others to discuss their own situations. We also created the Keith Milano Memorial Fund at the American Foundation for Suicide Prevention. With the help of some great people, we have been able to raise more than $1.7 million. In May we are dedicating all the episodes at the Mitlin Money Mindset to mental health topics.

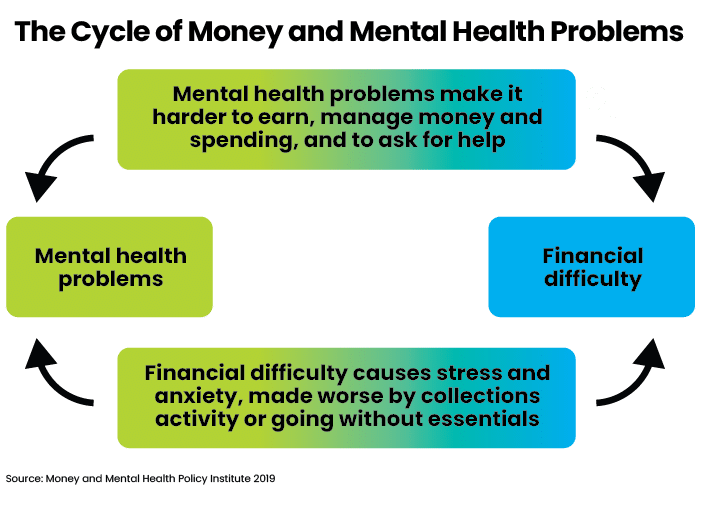

Our personal experiences have taught us the importance of focusing on the relationship between money and mental health, although that’s not something financial professionals usually do. However, a considerable amount of research has shown strong links between financial wellness and mental health. Poor financial decision-making and mental health problems often go hand in hand.

In fact, financial management is often one of the first skills to decline for individuals with mental health problems. Even for cognitively and behaviorally “normal” adults, concerns about finances and financial management can often provoke intense feelings of anxiety and stress.

Nearly half (46%) of people with debt also have a mental health diagnosis.

The majority (86%) of people with mental health issues and debt say that their debt makes their mental health issues worse.

People with depression and problem debt are 4.2% more likely to still have depression at 18 months compared to their counterparts without debt.

Those with debt are three times more likely to contemplate suicide due to that debt.

The American Psychological Association has found that money is a major source of stress. Many Americans are more stressed about their finances than they are about their health or personal relationships. High levels of debt are a common source of stress, which can cause anxiety, depression and sleep disorders, among other conditions.

However, “Few mental health programs include tools and educational materials that help adults to manage personal finances more effectively, prepare for behavioral/cognitive/physical health-related financial risks, or assess financial decision-making capacity,” writes Chris Heye, PhD, founder of Whealthcare Planning LLC.

“Healthcare providers, advocacy agencies, financial professionals, and technology companies need to work together to offer resources aimed at increasing financial literacy, identifying and mitigating (especially health-related) financial risks, and improving financial decision-making,” Heye continues.

A team approach

Because financial concerns are the No. 1 cause of stress for so many individuals, finding an empathetic financial advisor is critical. Many advisors underestimate the emotional value they can deliver simply by organizing a client’s finances and “cleaning up the mess.”

Making sure clients’ affairs are in order can go a long way toward lowering anxiety levels. This includes helping them create budgets, reduce and eliminate debt, create estate plans and get important documents in order. The National Institute on Aging has published a checklist that includes the steps individuals need to take and the information and documents they need to assemble.

Confronting serious mental illness within the family — which may include addiction or substance abuse, depression, anxiety, bipolar disorder, or similar mental conditions — is usually too much for a single family member to try to manage on their own. In these cases, it is essential to assemble a “wellness” team that should include other family members, friends, and caregivers, as well as financial, legal and healthcare professionals.

Recognize signs and jumpstart conversations

Warning signs of mental illness, noted here by the American Psychiatric Association, include sleep or appetite changes, mood changes, withdrawal, a decline in functioning, apathy and more.

Financial advisors may spot such signals as disorganization, confused thinking and compulsive buying behavior (CBB), which may be observed by binges and splurges. Sometimes referred to as shopping addiction or pathological buying, this mental health condition includes purchases that are persistent, excessive, impulsive and uncontrollable — despite the financial and other consequences.

Financial advisors must have important, tough conversations with clients. Mental and physical health are directly tied to better financial outcomes for all families. Most of us are comfortable talking about what we’re doing to take care of our physical selves but we need to be as comfortable talking about our mental health. People talk about exercising, getting checkups, going for surgery, etc., a lot more than they talk about seeing a therapist or taking medication for depression, for example.

We should be able to encourage clients to feel comfortable about discussing their mental health with us. In addition, we should encourage them to seek the appropriate mental-health help if needed. This is no different than identifying a tax issue and referring the family to a new tax professional.

According to this article from the American Psychiatric Association, “You don’t have to be an expert. You don’t need to have all the answers. Start by expressing your concern, as well as your readiness to listen and be there for the person. Don’t be afraid to talk about it. Reassure them that you care about them and are there for them. Use ‘I’ statements.”

Having these conversations and bringing mental health out of the darkness will lower the stigma and allow us to help put families on a path to success. We can make them feel that they are not alone and help them understand and seek the support they need when helping themself or a loved one cope with mental illness.

Larry Sprung is a wealth advisor and the founder of Mitlin Financial. Keena Pettijohn is the founder of Lifelogixs Strategic Consultancy Group. Together, they have over 50 combined years of financial services experience.

An intrinsic link

An intrinsic link