If you’re an advisor working with pre-retirees and retirees, you already know that there’s no perfect method for creating income and mitigating risk in retirement. Some popular approaches, including static withdrawal-oriented methods like the 4% rule, require selling regardless of market conditions. This risks drawing down portfolios during market downturns, creating the potential for long-term damage to a client’s retirement savings.

During periods like the Great Recession, this approach wreaked havoc on pre-retiree and retiree profiles. The S&P 500 fell by 57% from peak to trough over a 17-month period from late 2007 to mid-2009. The Covid crash of March 2020 hammered the S&P 500 by 34% within a mere 33 days, just in case anyone has forgotten the pain of bear markets.

Not only do withdrawal rate-oriented strategies create the potential for financial pain, they also can undermine a retiree’s sense of security and contentment during retirement. Research reveals that retirees with a consistent source of reliable income are happier and actually live longer.

In working with retirees and pre-retirees, I’ve found that a cash-flow strategy based on a predictable, reliable source of income sets the table for ongoing sustainability. It’s an income-driven approach that covers ongoing living expenses, but also provides plenty of potential for capital appreciation. This strategy, coupled with a realistic assessment of retirement spending and optimized Social Security claiming, lays a foundation for a successful retirement plan.

This article will discuss how this approach to retirement planning works, as well as the benefits of employing it with your clients.

In the absence of a clearly defined retirement plan, income production within a retirement portfolio can be haphazard at best. Clients may lack a real awareness of their spending patterns and how to match that spending with consistent, reliable income. The goal of an income-driven approach is to place cash flow at the center of the retirement planning process and not chase returns.

Consequently, this cash-flow strategy uses three key steps to produce income for retirement:

Estimating the retiree’s specific income needs based on their anticipated retirement lifestyle. This budget — or spending plan — should include non-discretionary and discretionary expenses. You’ll also want to cover other contingencies that arise in retirement, such as inflation, taxes and rising medical costs in later retirement.

Optimizing Social Security and other sources of income. This involves determining what sources of income a retired couple or individual retirees have and the best timing and sequence to activate those sources of income.

Filling the income gap. With steps one and two complete, this becomes super simple. You subtract the anticipated income from the anticipated expenses to obtain this number. While there are a number of ways to generate this income, I prefer an approach based on multiple dividend strategies and structured notes, which I’ll explain in the example below.

Major benefits and risk mitigation

One major benefit of an income-driven approach is that it doesn’t depend upon selling shares for income. When income is automatically provided from dividends and yields, the retirement portfolio remains whole — meaning drawdowns and selling aren’t required during a bear market or recession. The portfolio also has time to recover from adverse events such as bear markets and ongoing volatility.

In fact, the 2022 stock and bond markets were highly volatile, which illustrates the benefits of approaches that avoid ongoing forced sales of shares to fund a client’s lifestyle. While selling shares for income in a bear market isn’t good for long-term retirement portfolio health, such activity during volatile markets is also potentially risky. That’s because bad luck, due to bad timing, could exert a more negative impact on a portfolio than if such selling occurred during a more placid market.

Clearly, not being forced to sell shares for income mitigates sequence-of-return risk. You probably already know that sequence-of-return risk occurs when withdrawals during a down market further deplete a portfolio, leaving less principal to recover when the market rises again.

Another point in favor of an income-generating portfolio is liquidity. Many advisors favor long-term fixed-index annuities for the income portion of a portfolio. Unfortunately, these instruments lack liquidity and also limit participation in market gains.

How cash-flow-driven retirement planning works

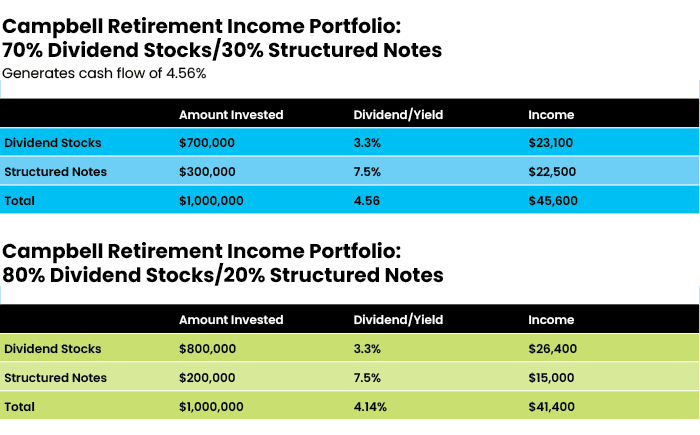

For example, let’s talk about a hypothetical couple whom I’ll call Carl and Cindy Campbell. After discussing their retirement goals and potential lifestyle, we determined that they have an income need of $100,000 gross, to a 4% year-over-year inflation rate was applied.

Carl is one year older than Cindy. They wanted to retire at the same time, so to optimize their retirement income, we planned for Carl to claim Social Security at 66 and Cindy at 67, their full retirement age. Together, their Social Security added up to a benefit of $64,000 a year.

That left an income gap of $36,000 a year that needed to be filled by creating a source of income from their $1 million investment portfolio. That portfolio was rolled over from their employer-sponsored 401(k) plans into tax-deferred IRAs.

Let’s assume I invested 70% of the Campbells’ portfolio in growing companies with a history of increasing their dividend payments over time. The dividend growth aspect is important, because growing companies are more likely to continue to pay dividends than companies that aren’t growing. When you invest in companies that have a history of growing their dividends, that helps mitigate the impact of inflation within the portfolio.

While these are solid dividend rates, they aren’t the highest available. That’s because chasing yield is seldom sustainable. The dividends pay a cumulative rate of 3.3%, yielding $23,100 in annual income. The goal of a dividend strategy is to receive a 4% to 10% increase on the total dollar amount of dividends year-over-year.

The remaining $16,900 in necessary income comes from laddered structured notes. Structured notes are debt instruments with a derivative component. They’re available through financial institutions and come in a variety of maturities and styles. In this case, we’ll use a laddered group of 12-month structured notes paying a coupon rate of 7.5%.

The coupon rates associated with structured notes fluctuate based on market factors, interest rates and other variables. Equity-linked structured notes such as these are associated with a particular market index, such as the S&P 500, the Dow Jones Industrial Average and Nasdaq. The type of equity-linked structured note that I favor for retirement income portfolios includes a feature known as a barrier and European style.

A barrier is a point at which you believe the index you invest in won’t fall beyond within the period of time of your investment. In this case, we’ll use a barrier of 50%. The notes are designed for investors who seek a contingent interest payment with respect to each review date for which the closing level of a group of indices — in this case, the S&P 500, the Nasdaq 100 and the DJIA — is greater than or equal to 50 percent of its initial value. That 50 percent is known as an interest barrier.

In other words, the interest barrier means that if these three indices don’t fall by 50% after a 12-month period, the structured note would pay back the principal plus the full interest collected. However, if any of the indices did fall by 50% or more from the starting point to the ending point, your client could lose up to 50% of their investment.

It’s important to understand that you can negotiate barriers, term lengths and coupon yields that are higher or lower depending on your client’s risk tolerance. Like all investments, structured notes are subject to risk and potential loss. This example is for illustrative purposes only.

There are a variety of ways to construct the portfolio depending on the amount of assets involved and the client’s risk tolerance. I show two examples below:

A final word

This type of retirement income portfolio has much to recommend. The approach creates liquidity while mitigating sequence-of-returns risk and market risk. This can be a successful niche approach and could work for other advisors pursuing the retirement income market.

Kyle Hammerschmidt is the founder and CEO of Mokan Wealth Management, an Overland Park, Kansas-based fiduciary wealth management firm that offers comprehensive retirement planning for individuals over 50. He is eager to share his research-driven, tax-focused approaches with other advisors catering to pre-retirees and retirees. Mokan offers investment advisory services through CreativeOne Wealth, LLC, a registered investment advisor.