Student loans, car loans, home mortgages — most of us at some time or other have used debt (or leverage), to purchase something we didn’t have the upfront cash for. That’s because there are some purchases that, due to the sheer scale of upfront cost, typically rely on the use of debt.

Commercial real estate is one such example. Debt is regularly used to finance commercial real estate projects. In fact, it is common for most acquirers and developers to borrow more than half of the total cost of the project.

When using debt to finance a project, ideally, the goal is to achieve higher returns from the project than may have been achieved without it. The reason? Utilizing debt typically requires placing the lender in a priority repayment position, meaning all debts must be paid before any returns can be distributed to investors in the project. This subordinate repayment position for investors adds risk, as there is no guarantee that there will be sufficient returns to both pay off the debt and pay distributions. That is why the goal when financing a project with debt is to achieve higher returns to mitigate the risk of cutting into the investor’s returns.

There are two primary ways that project returns can potentially be enhanced when using leverage on a project to help mitigate potential risks to investor returns:

When there is a positive spread (difference) between a project’s operating cap rate and its debt interest rate, it enables the equity holders the potential to earn higher annualized yields, all else equal.

The use of debt offers the potential to amplify returns for investors in the event the asset appreciates. In this case, once the outstanding principal balance is repaid, all additional upside or appreciation is distributed to investors

When we refer to positive or negative leverage in a real estate project, we are looking at the difference between the operating cap rate and the debt interest rate, which may enhance or dilute returns. Let’s tackle positive leverage first.

Simply put, positive leverage occurs when the operating cap rate from a deal is greater than the interest rate of its debt. In this scenario, using debt can actually improve the annualized yield on equity because the debt costs less to service than the cash flow received from the leveraged portion of the project.

Conversely, negative leverage occurs when the operating cap rate is lower than the interest rate of the debt. So, in this scenario, using debt can actually decrease the annualized yields on equity because the debt costs more to service than the cash flow received from the leveraged portion of the project.

When interest rates exceed operating cap rates, the use of debt is considered dilutive from an operating cash flow perspective because it cuts into the annualized cash flow for investors to pay off the higher cost of debt. Investors then have to increasingly rely on potential profits at sale in order to have the opportunity to generate their risk-adjusted returns. Accepting negative leverage in a project may still translate into favorable returns at exit or sale for investors, but the longer it is tolerated, the more risk it carries by diluting annualized cash yields.

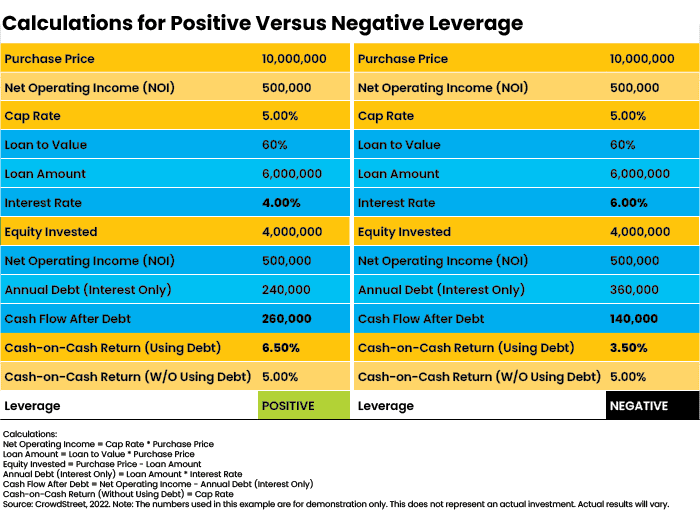

Consider the example below in Figure 1. This example is for illustrative purposes only and does not represent an actual investment or project. We begin with a $10,000,000 project that has an operating cap rate of 5% and for which we are borrowing 60% of the project value, or $6,000,000.

In the calculation on the left, when the interest rate is 4.00%, the investor pays $240,000 in annual debt service and earns an annualized yield on equity, or cash-on-cash return, of 6.50%. In the calculation on the right, when the interest rate increases to 6.00%, the investor must now pay $360,000 in annual debt service, earning a lower cash-on-cash return of 3.50%. In essence, all else equal, the investor earns $120,000 every year. Unless additional profits are generated at exit, the additional interest expense will dilute returns to equity.

This difference in the cash-on-cash return is due to different interest rate values. As you can see in the below example, other base values are constant.

As you increase the amount of debt and/or the interest rate in a negative leverage scenario, the dilutive effects on equity returns can be exponential. Thus, not only is it important to carefully consider the justification for pursuing a negative leverage scenario, but also the amount of debt used and its cost above the operating cap rate.

Does this mean negative leverage is to be avoided at all costs? Not necessarily. There are a couple of key takeaways to keep in mind:

Negative leverage may be justified during periods of overall market volatility. When the price paid for the asset is discounted enough to more than compensate the investor for the reduced yields or cash flow, then its use may be warranted. In this scenario, the potential for higher returns will now be concentrated into the profits at sale rather than into periodic yields during the holding period.

When the project’s rents are well below current market rates, it may be possible for a project to flip from negative leverage to positive leverage during the holding period as rents are adjusted upwards to match the market rates.

Negative leverage can make sense when there is an opportunity in a volatile market or in a special situation where the potential reward is higher than the risk. However, for any project that uses negative leverage, there must be a plan to transition to positive leverage during the holding period. Ultimately, the key is to understand whether negative leverage is temporary and if it is, then it may be prudent to remain patient and ride along the path to positive leverage for potential rewards at exit–the ride may not be as smooth, but there is the potential to unlock hidden gems in the form of mispriced opportunities.

This article was written by an employee of CrowdStreet and has been prepared solely for informational purposes. All information is from sources believed to be reliable. Nothing herein should be construed as an offer, recommendation, or solicitation to buy or sell any security or investment product issued by CrowdStreet or otherwise. This article is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any investor. Investing in commercial real estate entails substantive risk. You should not invest unless you can sustain the risk of loss of capital, including the risk of total loss of capital. All investors should consider their individual factors in consultation with a professional advisor of their choosing when deciding if an investment is appropriate.

CrowdStreet, Inc. (“CrowdStreet”) offers investment opportunities and financial services on its website. Broker dealer services provided in connection with an investment are offered through CrowdStreet Capital LLC (“CrowdStreet Capital”), a broker dealer registered with FINRA and a member of SIPC. Advisory services are offered through CrowdStreet Advisors, LLC (“CrowdStreet Advisors”), a wholly-owned subsidiary of CrowdStreet and a federally registered investment adviser. CrowdStreet Advisors provides investment advisory services exclusively to privately managed accounts and private funds and does not otherwise provide investment advisory services to the CrowdStreet Marketplace or its users.

As you increase the amount of debt and/or the interest rate in a negative leverage scenario, the dilutive effects on equity returns can be exponential. Thus, not only is it important to carefully consider the justification for pursuing a negative leverage scenario, but also the amount of debt used and its cost above the operating cap rate.

As you increase the amount of debt and/or the interest rate in a negative leverage scenario, the dilutive effects on equity returns can be exponential. Thus, not only is it important to carefully consider the justification for pursuing a negative leverage scenario, but also the amount of debt used and its cost above the operating cap rate.