Student loan forgiveness is a complicated topic that has recently become even more confusing to millions of borrowers amid legal skirmishes.

The Supreme Court announced on December 1 that it will expedite review of President Biden’s plan to cancel federal student loan debt. During its February 2023 argument session, the court will argue a case brought by six states that wish to permanently block the program that President Biden established through an executive order he issued in August. The U.S. Department of Education halted the program in mid-November.

The president’s plan has met some serious resistance because Congress generally enacts the rules related to student loans. The 8th Circuit Court of Appeals issued a continued nationwide injunction against the loan-forgiveness program after those six states argued the program threatened their future tax revenues and circumvents legal authority.

Separately, in early November, a federal district court in Texas issued a ruling calling the program “unconstitutional.” The U.S. Justice Department has appealed this ruling.

The 26 million borrowers who applied for the program — including 16 million who were approved for loan forgiveness — are in limbo. Meanwhile, families who are thinking about student aid options for their children who currently are or will be attending college also need clarity and confidence.

As the politically driven spotlight shines on student loans, this is an opportunity for us to help the families we serve become better consumers of higher education and understand their financing options.

It also pays to understand what the program offers, should its court-ordered pause be just temporary. And whether or not things come to fruition, advisors should be armed with the salient talking points for client discussions.

Who would qualify?

The Biden Administration promises to continue to fight for student debt relief as its program remains tied up in the courts.

The program promises to forgive between $10,000 and $20,000 for qualifying students and/or qualifying parents with outstanding federal loan balances due. The program aims to make this one-time student loan debt relief available to “eligible” borrowers who meet any of the following criteria:

Borrowers who received a Pell grant would be eligible for up to $20,000 in debt relief; debt relief is capped at $10,000 for borrowers who did not receive Pell grants. It is important to understand that this program only applies to federal loans (including Parent Plus loans) held prior to June 30, 2022. New loans are not eligible for the $10,000 or $20,000 “disappearing act.”

Payment pause extended again

Students and parents were encouraged to file for loan forgiveness by November 15, 2022, although they may technically have had until the end of 2022. These deadlines were driven by the student loan payment pause that was most recently scheduled to sunset on December 31, 2022, after a number of extensions.

Many borrowers have taken advantage of the loan repayment pause that began in March 2020 as part of the CARES ACT signed by former President Donald Trump. It was originally promoted as an emergency relief bill that paused payments and involuntary collections on federal student loans.

The goal posts on the loan repayment pause have been moved again, to June 30, 2023, pending the outcome of the court cases that have been filed.

What’s keeping clients up at night

The most common question I’m hearing from my clients is, “What should I be doing now?” All this stopping and starting regarding loan repayments has created confusion and anxiety for borrowers, so we have a real opportunity to provide some concrete steps for people to take in the midst of all this chaos.

The savviest advice we might give our clients is to make monthly payments on their loans: 100% principal payments since no interest is being charged at this point. If any/all of the loans are forgiven, the repayment funds will be returned to the borrower. If the loans are not forgiven, our clients will have put a dent in paying off the debt by being back in the habit of making monthly payments.

‘Built-in’ loan forgiveness

We also need to help our clients understand that the student loan program already has loan forgiveness built in (poorly administered but recently much improved) and several repayment options that deserve consideration.

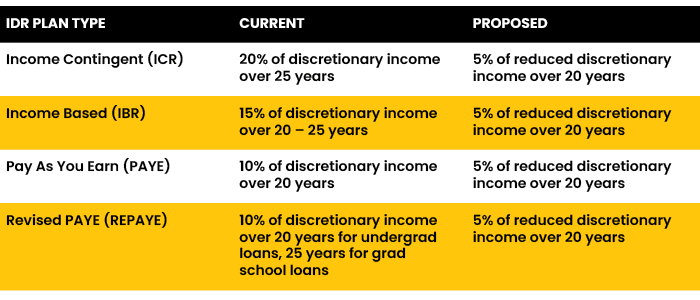

Another part of President Biden’s plan that hasn’t received as much attention but is very meaningful for our clients are the changes to the income-driven repayment (IDR) plans. These changes have yet to be approved but are slated for implementation in the summer of 2023.

Currently there are four IDR plans. The table below spells out how much participants are currently expected to repay compared with what is proposed:

Payment cuts. Reducing repayments from 10% to 5% of discretionary income basically cuts payments by 50%.

A higher threshold for “discretionary” income. Borrowers would be required to pay 5% of what they earn in excess of about $33,000 per year (225% of the poverty line, up from 150%). An undergraduate loan borrower wouldn’t pay the full amount they owed unless they had a starting salary of $60,700 or more.

Unpaid-interest assistance. If a borrower’s payments do not cover monthly interest, the government will cover the remaining interest so loan balances don’t increase. This is a major change that effectively “freezes” the loan so it will not grow over time, even if monthly payments don’t meet the minimums.

The Department of Education has also addressed the “small loan” issue by suggesting that loans of $12,000 or less be forgiven after 10 years (compared with the 20 or 25 years under current rules).

The Department of Education will automatically enroll or re-enroll certain students in an income-repayment plan if they allow their income data from the IRS to be used. Bottom line: If the income-repayment proposals are enacted, most college students will be eligible to make substantially reduced payments and the majority of borrowers are likely to have some debt forgiven after 20 years.

However, the program could also have some unintended consequences such as increased borrowing.

Taxes and time considerations

Advisors should also make sure that clients fully understand the implications of participating in loan-forgiveness programs — notably, the big tax caveat:

If and when loans are forgiven, the amount forgiven will be considered taxable income in the year of forgiveness.

In addition, some borrowers will be able to take advantage of longer repayment time frames. This is not a bad thing, but it will require that they have the right mindset from a behavioral-finance perspective. It could take them longer to become debt free and they’ll end up paying more in interest over time.

Action steps for outstanding loans

As advisors, we need to lead our clients through this morass and help them get to the other side of their student loan liabilities. Students and parents that borrowed money to pay for college need to prepare for the pending realities. Here are some “action steps” we can advise our clients to take:

Contact your loan servicing company and make sure your contact information is up to date and you are receiving the most current information from them regarding your loan(s).

Make sure you are on the best repayment plan available to you. Don’t assume the one you were on is the best one for you now.

Ask your loan servicing company to provide details regarding your next payment (interest rate, payment amount, due date, etc.)

Prepare your monthly cash-flow plan to include the loan payments that you haven’t had to make for the last 18 months.

Borrowing can be a good deal

If the proposed changes are approved and implemented, our first college funding recommendation should be to take the federal student loans with the idea that the borrower will enroll in the most cash-flow efficient income-driven repayment plan available after graduation. These loans should be held the full term (10 or 20 years) and the borrower should plan to make only the minimum payments in an effort to have as much forgiven as possible. This approach to student loan management will free up funds for saving for houses, marriage, retirement, and other lifestyle expenses that can’t be supported under the current rules.

According to a recent Brookings Institution opinion piece, current and future borrowers in IDR plans would pay back approximately 50 cents, on average, for every $1 they borrow in federal student loans. Whether you agree with the Biden plan or not, if the plan goes through, getting $1 worth of value for 50 cents makes financial sense.

With so much confusion about student loans, it’s clear clients desperately need our expert advice on college funding. We owe it to our clients to leverage every available tool, regardless of whether we believe the policies that created them make economic sense for the United States.

Beth V. Walker is a wealth advisor with Carson Wealth Management and founder of Center for College Solutions, which is based in Colorado Springs, Colo. She is also the author of the book “Never Pay Retail for College” Beth supports the SFC Consortium by collaborating with IECs, assessment coaches, and test prep coaches to provide services to families. She can be reached at bwalker@carsonwealth.com or 719-522-2278.

Borrowers who received a Pell grant would be eligible for up to $20,000 in debt relief; debt relief is capped at $10,000 for borrowers who did not receive Pell grants. It is important to understand that this program only applies to federal loans (including Parent Plus loans) held prior to June 30, 2022. New loans are not eligible for the $10,000 or $20,000 “disappearing act.”

Borrowers who received a Pell grant would be eligible for up to $20,000 in debt relief; debt relief is capped at $10,000 for borrowers who did not receive Pell grants. It is important to understand that this program only applies to federal loans (including Parent Plus loans) held prior to June 30, 2022. New loans are not eligible for the $10,000 or $20,000 “disappearing act.”