Connecting with Your Next Generation Retiree Clients about Long-Term Care Planning

The MIT AgeLab and MassMutual are collaborating to understand retirees' perceptions, language, emotions, and interests related to funding long-term care.

The United States is in a period of rapid demographic change — also known as disruptive demographics.1 With average life expectancy just shy of 80 years, the population of older adults in the U.S. continues to grow.2 The aging of the U.S. has resulted in broader compositional shifts in the overall population, such that by 2040 the percentage of the population age 65 or older will be larger than the percentage of the population younger than age 18. For the first time in U.S. history, there will be more older adults than children.3 As the U.S. population ages, the need for long-term support services will continue to grow.

At the same time, however, it is vital to acknowledge that family composition and relationships in the United States are also changing. These shifts, including lower rates of marriage and higher rates of unmarried cohabitation,4 lower birth rates,5 and higher numbers of individuals of all family types identifying as LGBTQ+,6 may change the way individuals navigate the complexities of caregiving and long-term planning. In line with this growing diversity, we can expect that long-term care (LTC) planning within family contexts will take a wider variety of forms than it perhaps has in the past. The composition of one’s family and overall support network greatly influence how people think about and prepare for their own long-term care needs.

In light of major demographic shifts and the evolution of the long-term care industry, it is important for financial professionals to understand how the next generation of retirees describe their own long-term care planning ideals. As useful context for helping clients to move from planning to preparing, it is also vital for financial professionals to understand how clients perceive, purchase, or withhold from purchasing insurance policies that provide long-term care benefits, as well as how clients involve their loved ones in conversations about their long term care planning.

A Study about Individual Risk, Framing and Perceptions around Long-Term Care (LTC) Insurance Among Next Generation Retirees

To explore the next generation of retirees’ perceptions, language, emotions, and interest in options to help fund their potential LTC needs, the MIT AgeLab and Massachusetts Mutual Life Insurance Company (MassMutual) have been working together to explore people’s perceptions of LTC planning in general, people’s own risk tolerance and expectations around their future care needs, and ultimately how financial professionals can most effectively connect with clients around LTC planning.

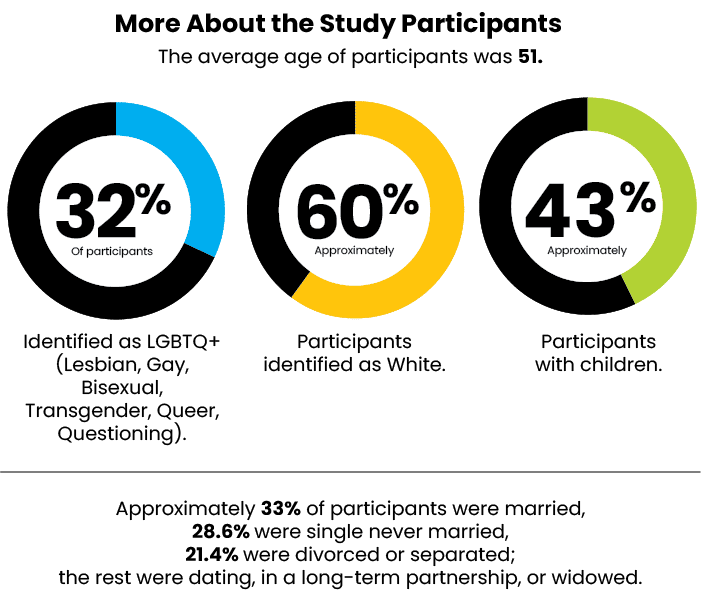

The first part of an ongoing multi-stage research collaboration involved 12 virtual focus groups held during March 2022 with 84 participants, all of whom lived in the United States, were between the ages of 40 and 64, and had at least $75,000 in liquid assets (not including home equity and dedicated retirement accounts). Just over 32% of participants had a current insurance policy with long-term care benefits; the rest were strongly considering purchasing an insurance policy that would provide long-term care benefits within the next several years.

Approximately 57% of participants reported working with a financial services professional who gave them advice. Given our interest in understanding this topic as it relates to life course development and changing relationship dynamics, focus groups were organized at the intersection of age, marital status, parenting status, and sexual identity and orientation.

Five Key Takeaways for Financial Professionals

Here were the top five takeaways from our focus group research that financial professionals can leverage to better connect with clients about long-term care planning:

1. Make it Personal

Preparing for LTC needs has always been a deeply personal and often fraught topic. COVID-19 has raised many people’s personal awareness of their own physical fragility and the nature of care provided in assisted living and nursing home facilities.

For some, prior caregiving experience, accidents, injuries, or medical issues may have already made them cognizant of potential care needs and/or concerns about quality and costs of care. Connect with clients about what, specifically, makes long-term care planning feel personal and actionable.

2. Consider Family Situation

Family, or lack thereof, was mentioned often among focus group participants as a motivation for considering an insurance policy that provides long-term care benefits.

For many, the fear of burdening family members (often children and spouses) can catalyze thinking and action related to long-term care planning. In our study, we found this was often the case for people who were married or in long-term partnerships, as well as those who had children. For others (especially those who were unpartnered), the question of “who will take care of me” raises its own anxieties.

Be the person clients feel permitted and encouraged to speak with about a variety of topics, including long-term care planning. Prior research we have conducted⁷ has shown that the more topics clients felt they could connect with their financial professional about, the more satisfied they generally were.

3. Discuss the Specifics

The majority of participants we spoke with (similar to 90% of the general public) say that if they needed care, they would want to receive that care in their own home if possible.

Engage with clients around the specifics of long-term care planning,7 learn what comes to their minds when they think of long-term care planning, including where, how, and from whom they would potentially want to receive care should they need it in the future. Curate a list of potential costs of care your client could expect based on real costs in your locality.

4. Offer Multiple Scenarios

Most participants in our study expressed an intention to purchase an insurance policy that provides long-term care benefits as one way to prepare for a potential long-term care event. However, many expressed the desire to wait for “the perfect time” or “magic age” to purchase a policy (e.g., not too early, so as to avoid paying premiums longer than necessary, but not too late, so as to avoid the emergence of health issues or accidents that could raise one’s premium or make one ineligible for coverage).

Participants’ desire to create a sense of security for the future, while also postponing a decision, created a prolonged sense of limbo and period of inaction as they tried to determine the optimal purchasing time. As part of ongoing planning and advising conversations with clients, talk through potential scenarios around timing of purchasing an insurance policy that provides long-term care benefits if that is something they are interested in but have expressed confusion about.

5. Help Navigate the Shopping Process

We heard from many that beyond the standing question of, “Will I actually use a LTC policy,” the process of shopping for — and purchasing — an insurance policy that provides long-term care benefits, was often difficult to muddle through. In fact, many described the process to be cumbersome and confusing.

Many people were not aware of various policy features available today. Even those who were more knowledgeable on the topic experienced confusion in deciding which features of a policy they were personally most likely to need in the future. Still others were concerned about restrictions and waiting periods that could prevent them from truly being able to take advantage of their LTC policy features when they needed them.

Among other features to discuss with clients, financial professionals can share that if policyholders do not need their long-term care benefit, hybrid policies allow them the versatility of leaving a legacy through a death benefit or withdrawing funds if needed. Ultimately and depending on the features of the policy, there are different ways in which an insurance policy that provides long-term care benefits can serve as an investment.

Conclusion

Based on what we have learned thus far, the next phase of our collaborative research explores how different framings or narratives around LTC affect interest in and acceptance of insurance policies that provide long-term care benefits. With effective framing or narratives around LTC, financial professionals have the unique opportunity to help clients identify long-term care planning as a timely and important issue that should be prioritized and work with clients and their families to think and talk through different care options, including associated costs. Effective framing can also equip clients with the knowledge and confidence to choose a solution that meets their needs and help protect what they value. With increased awareness of the types of solutions currently available, more people may be better prepared for the potential of unforeseen long-term care events.

About the authors

Julie Miller, PhD, MSW, is a research scientist at the MIT AgeLab. Samantha Brady, MPA, MA, is a research specialist at the MIT AgeLab. Sophia Ashebir, BA, is a technical associate at the MIT AgeLab. Lisa D’Ambrosio, PhD, is a research scientist at MIT AgeLab. Caryl Falvey, MBA, CLTC, leads marketing strategy for MassMutual. Matthew DiGangi, MBA, CLTC, heads annuity/hybrid-LTC distribution for MassMutual Strategic Distributors. Joseph F. Coughlin, PhD, is director of the MIT AgeLab.

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC. 1 Coughlin, J. F. (2007). Disruptive demographics, design, and the future of everyday environments. Design Management Review, 18(2), 53. 2 Population Reference Bureau. (2020). 2020 World Population Data Sheet. |

www.prb.org/wp-content/uploads/2020/07/letter-booklet-2020-world-population.pdf 3 MIT AgeLab analysis of U.S. Census data, 2017 National Population Projections Tables: Main Series. 4 Schoen, R., & Owens, D. (2019). A further look at first unions and first marriages. In The Changing American Family

(pp. 109-117). Routledge. 5 Kearney, M. S., Levine, P. B., & Pardue, L. (2022). The Puzzle of Falling US Birth Rates since the Great Recession.

Journal of Economic Perspectives, 36(1), 151-76. 6 Human Rights Campaign Foundation. (2021). https://hrc-prod-requests.s3-us-west-2.amazonaws.com/We-Are-Here-120821.pdf 7 Brady, S., Miller, J., & Balmuth, A. (2020). “Navigating Client Relationships During COVID-19”. Journal of Financial Planning. https://www.financialplanningassociation.org/article/journal/AUG20-navigating-client-relationships-during-covid-19