Target-date funds are an increasingly common investment choice in 401(k) plans. Some advisors will choose to ignore them because they cannot “manage” them. Thoughtful advisors will learn more about them and develop a strategy to work with them to provide the client with the optimal investment plan.

What they are

These funds address investors capital needs at some future date — hence the name “target date.” The date most often used is an investor’s retirement date. The asset allocation — and risk — becomes more conservative as the target date is approached. Target-date funds are often default options in 401(k) plans to assure that employees are fully invested in appropriate vehicles.

How they work

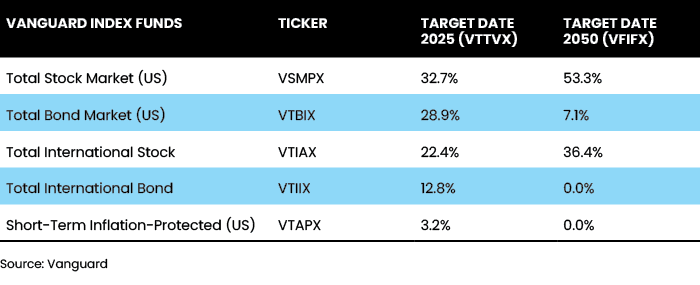

The asset allocation follows a risk-reducing glide path that gets more conservative as the retirement date approaches and into retirement. Table 1 demonstrates Vanguard’s approach.

Pros — from the client perspective

For a client, a target-date fund is an all-in-one vehicle. It provides a diversified portfolio that is on autopilot with risk reduction up to and into retirement.

For the advisor, a target-date fund is unlikely to reflect optimal investment opportunities at any given time given its static nature.

By way of example, the Target Date 2050 (VFIFX) above, which would be appropriate for an investor with about 30 years until retirement (age 30+), shows an international stock allocation of about 36%. Our current view is that U.S. equity markets have been and will continue in the near term to be stronger than international markets — so our allocation for this investor would be closer to 15% — an underweight vs. the Target Date 2050.

Going the other way, the Total Stock Market (VSMPX) fund holds about 16% of its assets in smaller companies, or about 8% of the total portfolio (as the holdings are based upon market cap). Our view is that as the U.S. economy recovers, smaller companies will do well and we hold about 17%+ in small and midcap equities for this investor — an overweight to the Target Date 2050.

An advisor is often hired for — among other reasons — navigating the financial markets for the client. A target-date fund limits the ability to do this.

There are some circumstances where a client is essentially “locked in” to using target-date Funds in a 401(k) and the advisor should create a “work around” strategy with the non-401(k) funds. Some 401(k) plans have many target-date options and very few other options — most often a limited number of mutual funds. For this client, the advisor should understand what the underlying securities are in the target-date fund and invest in other funds (IRAs and taxable accounts) to offset these “locked in” positions and produce an overall portfolio that best reflects the advisor’s outlook.

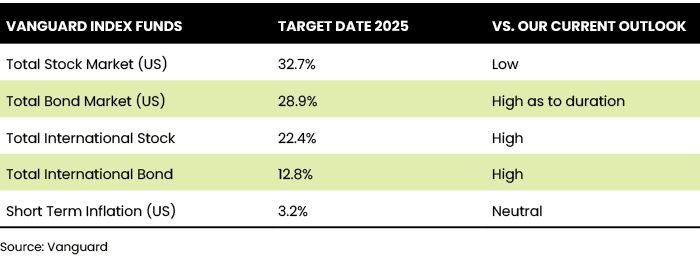

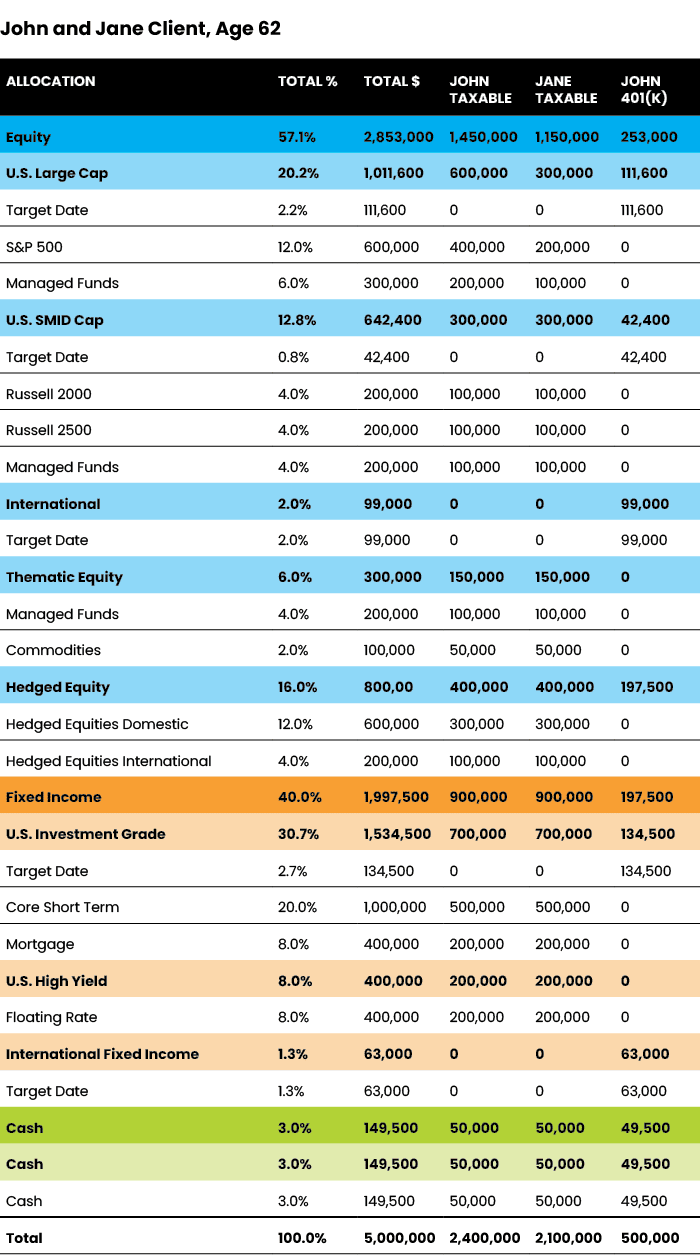

As an example, see the schedules that follow. The 62-year-old client has $500,000 in a 401(k) and is limited to target-date funds. As the client is near retirement, a target date 2025 was chosen. As a reminder, the allocation of this fund is static — the allocation remains the same regardless of what is happening in the economy and financial markets. This will most likely not reflect our current investment outlook. These differences are expanded in Table 2.

In creating the “work around” strategy shown in Table 3, there are four steps:

Identify the asset categories and associated percentages underlying the target-date fund (see bottom of schedule) using Morningstar reports which provide portfolio “look through” information that goes beyond what Vanguard provides.

Using the 401(k) balance of $500,000 and the asset category percentages, create a schedule showing the amounts allocable to each asset category. See far right column titled “John 401(k).”

Create the remainder of the schedule using non-401(k) assets that you manage. These are shown as “John Taxable” and “Jane Taxable.”

Adjust the non-401(k) assets to arrive at a Total % schedule that comes closest to reflecting your market outlook.

Conclusion

It is important for every advisor to understand what is “under the hood” for each investment available to a client so that smart portfolio decisions can be made. Fully integrating all investments into a client’s investment plan is the best way to assure optimal results for a client.

Richard B. Freeman, CFP is a senior director, wealth advisor with Round Table Wealth Management and is based in New York City. He can be reached at Rich@Roundtablewealth.com.