Advisors are sometimes overwhelmed that they don’t have the expertise to handle all the needs of all of their clients. This can be particularly true for newer advisors and those working with clients undergoing major life changes including gray divorce, a major health crisis, or a messy lawsuit that threatens their financial wellbeing.

Clients often feel that disconnect too.

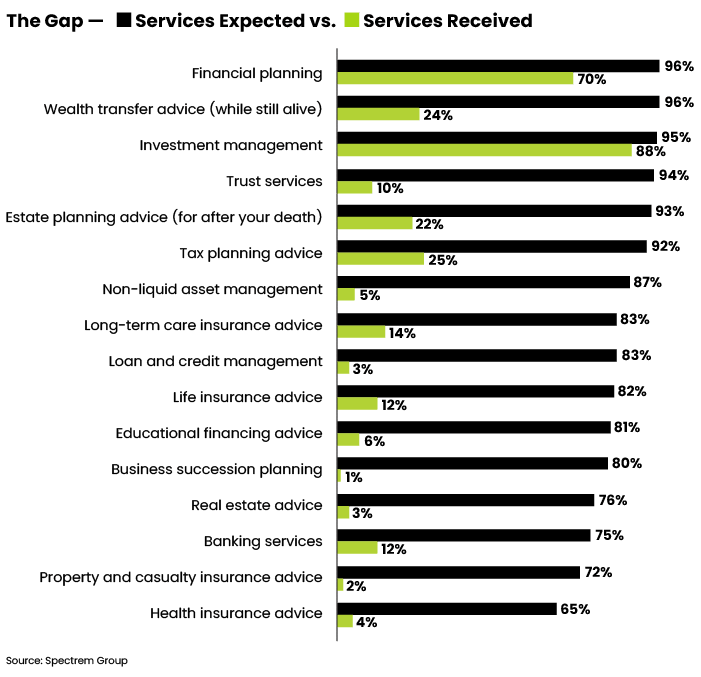

Spectrem Group did a study last year that shows the average gap between the services clients expected compared with the services they received is 73%. In other words, almost three-quarters of investors do not receive what they expected, hoped for, or needed in some cases.

Trust services had the largest gap, 84%. Although health-insurance advice had the smallest gap, it was still a sizeable 61%. Business succession planning had a gap of 79%, with only 1% of clients receiving services in that area.

Here are a couple of things to think about, though.

First, studies and research show that not every client needs, wants, or values services in every area. Business succession planning is a good example because many advisory clients aren’t business owners.

Second, some financial advisors are likely deficient in the less-sought-after areas of advice —including health insurance, real estate, and certain non-liquid investment advice — but most are excellent at addressing client’s main concerns.

What really matters

Clients aren’t going to give you a pass if you fail to help them with their concerns. As a “supposed” comprehensive wealth management advisor, you must understand the breadth of concerns your clients have regarding their financial well-being. For example, they’re likely to need advice on estate planning and trusts, wealth transfer, insurance and credit management.

That being said, it is not necessary to be the expert in every area for clients. However, you can and should be capable of helping resolve many issues where you don’t have in-depth expertise by calling upon qualified professional affiliations who can provide advice in those areas.

The point is, a comprehensive financial advisor or planner should at least ask questions about each area, to get a picture of a family’s comprehensive financial wellness, even if they don’t provide a solution themself. Open items become “comments of need of coverage” on a financial plan you provide. An example is the One Page Plan discussed by Carl Richards.

Mind the gaps

One area that’s getting harder for advisors to pass off is financial planning. It’s no longer just a nice extra to tack onto investment management services. According to the Spectrem study, 96% of investors expect to receive financial planning as part of their wealth management services, yet only 70% are receiving that service.

“No longer are investors just seeking investment advice. They are looking for more complex advice. However, financial advisors are most comfortable providing investment advice. This leads to significant gaps in the relationship between investors and their advisors,” reports Spectrem Group.

True, most investors want and are receiving investment management advice, says Spectrem. But it has found that clients are experiencing big gaps in estate-planning advice, wealth-transfer advice and tax-planning advice. Clients would also like to see more help with insurance products, education planning and charitable services, says Spectrem.

Altogether, Spectrem identified 16 areas where clients reported a gap between the services they expect and the services they receive.

Action points

It is important that financial advisors review their service models and their discovery process to determine what gaps exist between each of their client’s wants and needs. Advisors should also take inventory of what they deliver directly or through affiliated relationships.

Asking a client if they need advice or help in a particular area can make a positive difference in your relationship because it shows you are thinking about them and their needs.

Simple questions — such as, “Are you satisfied with your banking services or your insurance coverages in XYZ area” — can help you understand your clients better. Hopefully, you have asked business-owner clients about their succession plans. If not, that’s a fertile area as well.

Asking “Are you satisfied with your tax preparer” or “Do you have any questions about your taxes, or do you need any advice in that area?” can also reveal client needs and concerns.

Presumedly, you know if your client should be considering trust services or has questions about wealth transfer. But if not, asking where they are in their estate-planning preparations could open these conversations.

It would seem logical that most, if not all, of your clients have property and casualty coverage. However, this too is a good talking point. Questions such as “Are you happy with your P&C coverage?” and “Who do you work with and would you recommend them to family members?” may reveal they are dissatisfied and need a change.

It is not uncommon for investors to own real property outside of their investment portfolios. Do your clients? Ask them.

Each of these areas represents an opportunity to discuss with your clients their wants, needs, current situation and their satisfaction with that situation. Knowing your client and showing interest builds relationships.

It takes very little time to show clients you care. Asking questions of concern will give you the opportunity to learn so much about clients you want to retain for a lifetime. Not only will it help you enhance those relationships. it should also give you entry points to connect with potential centers of influence. It’s all about the questions and knowing more about your clients. Be curious!

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant and trainer to financial professionals. David has worked with the financial services industry for decades, originally as a consultant with IBM and then with UBS/Paine Webber before starting his own firm. If you would like more information about his services, contact him at David@CoachDavidLeo.com or visit www.CoachDavidLeo.com.