While optimizing investments to save on U.S. taxes has long been a fundamental of sound portfolio construction, now is a particularly good time to explore how you might help clients generate more “tax alpha.”

After 10 years of above-average returns, we expect markets to produce more modest results and experience greater volatility in the next decade. While it is unclear whether any tax provision of the Build Back Better bill may ultimately get passed, changes adopted years ago are scheduled to go into effect in 2026. For example: • Income taxes. Today’s highest marginal income tax rate of 37% is set to increase to 39.6% after 2025. • Transfer taxes. While in 2022 the lifetime exemption (amount that any individual can transfer to a non-spouse free of transfer tax) is $12.06 million per person, starting in 2026 it is slated to be reduced to $5 million per person (indexed for inflation).

Make sure you work with a team to ensure your client’s portfolio has a solid tax management plan. Given the complexities of both U.S. tax law and today’s investment options, this is not a do-it-yourself project. It’s not even a job for a single type of highly trained specialist.

“Given the complexities of both U.S. tax law and today’s investment options, this is not a do-it-yourself project. It’s not even a job for a single type of highly trained specialist.”

Still, you will want a big-picture understanding of how portfolios can generate tax alpha. So here is your guide to three key steps that might help clients keep more of the money they earn.

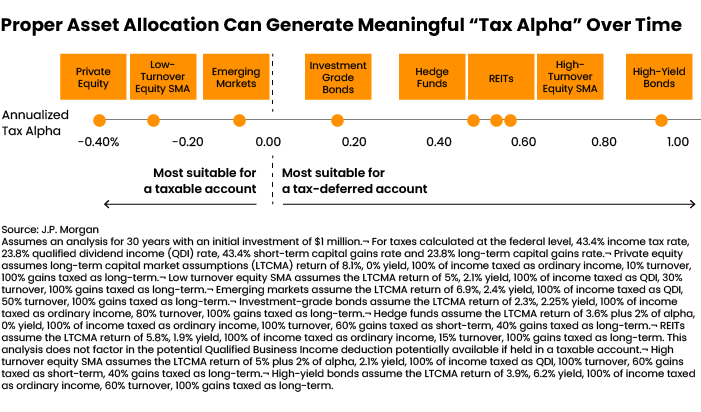

It’s not just what you own, but where you own it. The type of account in which a specific asset is held can dramatically impact your tax exposure.

A quick asset location suitability test is this: Your client’s portfolio may not be tax-optimized if (a) all their assets are in one kind of account (i.e. taxable or tax-deferred), or (b) they have all of the same holdings in different types of accounts.

The general rule is that, all else being equal, you want to hold tax-inefficient assets (especially those with higher growth potential) inside tax-advantaged accounts such as a 401(k), deferred compensation, IRA, Roth or annuity.

The reason behind the rule is simple: Tax-deferred accounts — such as 401(k)s, deferred compensation, traditional IRAs and annuities — all delay income tax liabilities until assets are withdrawn. This delay allows them to grow and compound tax-free. With a Roth IRA, you pay the income tax on the assets upfront, but then the money in the account gets to grow tax-free, and there is no tax bill upon withdrawal.

Good candidates for tax-deferred accounts are high yield bonds, high-turnover equity strategies, hedge funds and other investment products that tend to generate taxation at ordinary income rates via interest or net short-term capital gains. Assets that generate predominantly qualified dividend income or long-term capital gains, both of which are taxed at a preferential rate, are generally better off in taxable accounts.

In contrast, private equity is generally a less efficient asset to hold in a tax-deferred account because most (if not all) of the returns it generates will be taxed at preferential long-term capital gain rates. It would be better to put your clients’ private equity holdings in a taxable account, such as an individual, joint or (even better) a grantor trust where future growth is shielded from transfer tax.

Of course, to put your clients’ dollars and investments in the right accounts, you have to know the types of accounts they may need and for which they are eligible. In general, maximizing one’s contributions to qualified plans (401(k), 403(b)) and deferred compensation arrangements can be a great first step in creating account diversification.

Trade With Tax Awareness

Markets’ increased and likely prolonged volatility creates opportunities for more active tax-loss harvesting.

Indeed, it now can be costly to wait to do your tax-loss harvesting at the end of the year or even the quarter. A better practice is to review client portfolios regularly for embedded losses.

Clients also might benefit from a separate, tax-managed account — one that is specifically designed to constantly look for losses and harvest when opportunities arise.

Of course, to harvest tax losses, you sell a stock in which you have experienced a loss so that you can claim that loss against gains (already realized or future). Then, if you like the stock sold and/or want to preserve your portfolio’s asset allocation, you can purchase an equity with similar, but not exact, characteristics (e.g., sell Coca Cola, buy Pepsi). However, care must be taken to avoid the Wash Sale Rule (IRC section 1091), which prevents investors from taking a loss if they buy a security considered “substantially identical” within 30 days before or after the loss trade date.

Similarly, if you are transitioning your client’s portfolio to a new strategy, you’ll want to make sure to do so tax-efficiently. This means weighing the tax costs of changing vehicles versus the new position’s potential return; it also means seeing if any positions of their current strategy can be transferred “in kind” to the new strategy in order to defer realizing a gain.

Look for Tax-Smart Tactics

In addition, help clients look for opportunities to boost tax alpha when:

• Donating to charity

If your clients want to give to charity, for example, consider these two tax-efficient moves: 1. Public charities/donor-advised funds (DAFs). Clients who donate long-term, appreciated securities (individual stocks, exchange-traded funds, mutual funds, etc.) to a DAF will not need to pay the capital gains tax incurred if they sold the asset and then donated the proceeds. Yet they still might be able to claim a fair market value charitable deduction for the tax year in which the gift is made. (The deduction is subject to limitations based on a percentage of your client’s adjusted gross income.)

2. Qualified charitable distributions (QCDs). Instead of taking a required minimum distribution (RMD) from a traditional IRA, your client might make a QCD. The money (up to as much as $100,000 each year) would go directly from the IRA custodian to the public charity of their choice. (For this purpose, a public charity does not include a DAF.) It would count toward their RMD for the year, and they would not have to pay taxes on it, but they would not receive a charitable tax deduction.

• Giving to family

If you think one of your client’s holdings could deliver outsized growth, and they have both the desire and capacity to give to their family, you may want to help them create a grantor retained annuity trust (GRAT).

GRATs are created for a limited time. GRATs are generally structured so that you, as the grantor, receive back the original amount put in plus growth, assumed at a minimum hurdle, or the 7520 rate. At the end of the trust’s term, while getting back what is put in, any appreciation of the asset over the hurdle rate goes — free of gift taxes — to the trust’s beneficiaries.

• Bridging lumpy cash flows

It is common to experience a mismatch between a need for ready cash and what’s liquid. For example, a desired work of art or home may come on the market, but there’s not enough cash sitting in your client’s portfolio to purchase it.

Using a line of credit can separate their purchase decisions from their decisions about investments. It can give clients time to raise the cash tax-efficiently in their investment portfolio, or the credit line can serve as a bridge until they receive an anticipated influx of cash.

Amanda Lott, CFP, is head of wealth planning strategy at J.P. Morgan Private Bank. A version of this article for clients was published here.