Mary has been a teacher at the local elementary school for 25 years. She is not presently eligible to retire with full benefits, based on her age and service credits, but the retirement plan offered through her school district just announced the option for employees to buy years-of-service credit. This would allow her to retire early with full benefits.

Mary and her husband Randy, your clients, are interested in doing this. Randy loves his job and has no intention of retiring. But he works remotely and if Mary retires, they could move closer to their only daughter and grandkids, who live two states away. They schedule a meeting with you because they want to understand if it would make sense for Mary to purchase these credits.

Years-of-service credits can be quite expensive because one is, in effect, buying an annuity (more on that later). The only bucket of money the couple has that could provide enough funds to purchase the credits is Randy’s 401(k). But taking an early 401(k) withdrawal would be costly since they would owe income taxes and a 10% penalty. However, there is one tool — an Marital Qualified Domestic Relations Order or QDRO — that may allow Mary to use the 401(k) money tax free to buy the credits.

How QDROs Work

A QDRO is an order issued by a court or state agency that allows retirement money to be retitled in the name of an alternate payee. Those payees can only be spouses, former spouses, a child or other dependent of a retirement plan participant.

QDROs, introduced by law in 1984, are commonly used in divorce to equalize assets from one spouse’s qualified plan to the other spouse. But a QDRO can also be used in other ways. For example, couples can use the orders to divide a public pension that one of them has. Here is guidance from the Department of Labor and the IRS.

A Marital QDRO is an order for assets to be divided within a marriage, as there is no intention for the couple to divorce. After a couple marries, they have marital property, which is everything that is earned during the marriage, as well as separate property. An example is an inheritance that is received by one party outside of the marriage. Marital QDROs aren’t that common, but there are a few situations in which they may make sense:

All of the assets are in one spouse’s name and, for personal reasons, they want to move some funds to the other spouse.

There is a need to access inaccessible funds. Distributions from assets received as the result of a QDRO are not subject to the 10% early withdrawal penalty. (Distributions from retirement plans prior to age 59 ½ are usually subject to a 10% penalty. Note that some plans will only allow a one-time distribution from assets received through a QDRO, but a portion can be rolled over to an IRA or other qualified plan, and a portion can be distributed to the client. Once funds are rolled under a QDRO into an IRA, the 10% penalty will apply if no other exceptions exist.)

A client is still working but wants to move money from current retirement plan into a Rollover IRA in the other spouse’s name.

A client believes a pension plan will not be able to meet its obligations and they want to exit the pension but can’t due to plan rules. A spouse can transfer pension assets to the other spouse to gain control.

QDRO Becomes Separate Property for Couples

When doing a Marital QDRO, both parties must understand that assets become separate property. There has to be a great deal of trust between the spouses because one could take the QDRO and then file for divorce. The QDRO is no longer part of the marital division of assets and the spouse whose account it was distributed from will no longer have a marital claim to it. Also, when you file a QDRO, the company plan rules will sometimes not permit contributions into the retirement plan for a period of time, so that could impact the company match and your tax deferment opportunities.

While clients may consider a Marital QDRO, they should work with legal professionals, tax experts, and their financial planner to determine if this is the best course of action.

Back to Our Client Example

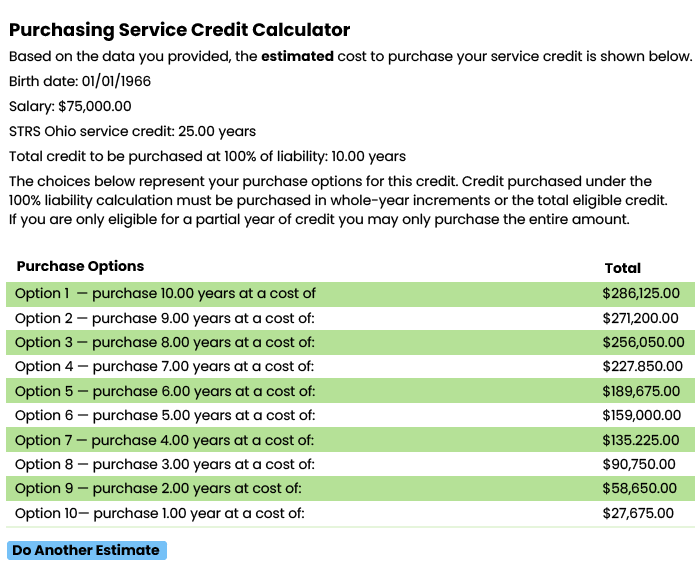

As mentioned earlier, it won’t be inexpensive for Mary to purchase service credits. As an example, the chart below shows how much if could cost an employee of The State Teachers Retirement System of OHIO (STRS Ohio) to purchase service credits.

Based on this calculator, if Mary retires two years short of being eligible for full benefits, she would receive $3,863.45 instead of $4,502.58 per month, which is a 14% reduction. Ten years of payments of the reduced amount is $463,614 vs $540,309.60; this is $76,695.60 less of income.

Let’s say Randy would have to take roughly $60,000 out of his 401(k) so Mary could purchase two years of service credits. The opportunity cost of making this purchase is that the $60,000 will no longer be invested in the market, but it would only take 14 months of $4,502.58 payments for the couple to recover the purchase amount.

Additional Considerations

For an advisor to help a client determine if this is an appropriate choice, he or she will need to look both at the financial factors and the impact on the client’s life. This would include looking at Mary and Randy’s monthly income needs and how responsible they are with money. If they are not disciplined, they might be tempted to take cash out of Randy’s 401(k) to pay for a new home, cars and trips — purchases that often show up right after a couple retires. Receiving monthly payments reduces this risk since the funds will be received over time.

At the same time, having a larger lump sum in Randy’s 401(k) may do little for the couple if they aren’t invested appropriately for their situation. Being overweighted to equities, remaining all in cash or concentrating assets in one sector are all potential problems.

A financial advisor should also look at:

The couple’s life expectancies. The trade-off for the purchase of service credits is that these assets will not be available for other purchases. The longer the life expectancy the more likely that the purchase is worth examining. Giving up the assets and passing shortly thereafter would be a significant loss.

Other sources of guaranteed income. This includes Social Security and any annuities. How likely are the payments to be received as promised? Financial planners should consider examining multiple scenarios under which full or partial payments are received to stress test the plan.

How the purchase will impact an estate plan. If leaving money to loved ones is a priority, then the purchase will make less sense.

The default risk of the pension plan. This is a significant concern as pensions will struggle significantly to make all of the promised payments to the next generation of retirees. The first step in examining the health of a pension is to look at the assumed rate of return.

Moving Forward

Let’s assume you determine that purchasing service credits makes financial sense for Mary and Randy and they decide to move forward with this. They can have an attorney draw up a Marital QDRO which will allow Mary to receive a transfer into her name from Randy’s 401(k). Because a Marital QDRO is a court order that’s allowed by the plan, the money will move regardless of which state Mary and Randy reside in.

John M. Gehri, CFP, ChFC, and Monica Dwyer, CFP, CDFA, are advisors with Harvest Financial Advisors in Cincinnati, Ohio. John may be reached at john@harvestadvisors.com. Monica may be reached at monica@harvestadvisors.com.