As a financial behavior specialist who spends a lot of time both professionally and personally with financial planners, I’m continually exploring what they find most frustrating about their work. “Having clients ignore my advice” is always at the top of the list.

These intelligent, dedicated, creative professionals care deeply about their clients and spend a lot of time crafting solutions to solve their clients’ problems only to be disappointed to find their sage advice ignored.

As my friends and I say after we have been particularly “wise” discussing what others in our lives “should” do, “The world would be a better place if people would just listen to us.” We say it tongue in cheek and yet …

Defining What Success Looks Like

When I first began helping people with their relationship with money, I innocently thought that success meant that my clients’ behaviors would change in the way that I thought best for them. (I was the helper, after all.) And what I thought was best usually aligned with the way they said they wanted to change.

Then I worked with a dynamic woman, I’ll call Lois, in her late 70s who wanted to meet with me because her husband had passed away after a long battle with Parkinson’s disease. She inherited $1 million-plus from “his” retirement accounts but couldn’t allow herself to consider it was now her money.

Lois was (and is) intelligent, curious, insightful, funny, loving and passionate about life. She was also grieving the loss of her husband and at a loss for what her role was in life now that she was no longer a wife and caregiver. In addition, she had a six-decades-long story that she was “bad” with money and a four-decades-long story that, as opposed to her, her husband was “good” with money. “This is going to be fun and easy,” I thought.

So, we diligently worked together exploring her money scripts, reframing her stories about how “bad” she was with money. (After all, she and her husband accumulated several million dollars.) We also discussed how the money in the non-retirement account, which she did consider hers, was accumulated the same as the money in the retirement account.

Six months and eight meetings later, Lois told me our work together was done and that while she still didn’t feel that the retirement account was hers, she felt at peace with that feeling and thanked me for my help.

Finding an Authentic Behavior

On the 40-minute drive home, I was devastated. I had failed. Lois hadn’t changed. What had I done wrong? As I pulled into my driveway, I had one of those aha! moments. My job was not to get her to behave with her money as I wanted her to. My job was to help her find her own authentic way to behave with money. Ultimately, my job is to do no harm — which means to do nothing to impede her journey towards her version of financial health — and, in the best of circumstances, to assist her moving forward towards financial peace.

Luckily through my training and mentorship with Drs. Brad and Ted Klontz at the Financial Psychology Institute and Creighton University, I know the best way to help a person is to use my “exquisite listening” skills to assess where my clients are in the stages of change and base my meetings upon the stage they are in to help them determine their next steps.

Did I lose you? Did you know that there is an entire area of study devoted to how and why people make behavioral changes?

Six Steps for Change

“Changing For Good,” the seminal book by James Prochaska, John Norcross and Carlo DiClemente, explains that there are six stages in the change process:

Pre-Contemplation. At your annual meeting with your clients, a married, retired couple, you tell them and show them that if they continue giving money to their adult son, their ability to fund their life will be severely compromised. They look at you politely but stonily and assure you it will be fine.

Contemplation. Three months later your clients call you because their son needed another $30,000 to pay for “unexpected” repairs (a 25-year-old roof) and while they want to give it to him, they know the market is down and now is a terrible time to sell investments but …

Preparation. A month later, your clients request a meeting to talk about what they need to do to adjust their spending for the year due to the $30,000 unanticipated withdrawal and they wonder if you have seen other parents in their situation “fix” the problem. They are interested in what their options are in terms of talking to their son and/or changing their lifestyle.

Action. Two weeks after the last discussion, your clients call and want to practice having a discussion with their son. They also want reassurance that they are doing the “right” thing. They schedule a date to have the discussion with their son.

Maintenance. After a difficult but ultimately productive discussion with their son, they are committed to not giving any money other than birthday and holiday gifts. They ask you to help keep them accountable with monthly check-ins and support when the inevitable requests come in.

Termination. After several years, both your clients and their son and his family have stopped the unhealthy money behaviors. It took several ups and downs and giving “one last time’s,” but ultimately healthy boundaries have been established and they send you a lovely gift certificate to thank you for your assistance.

Helping May Be Hurting

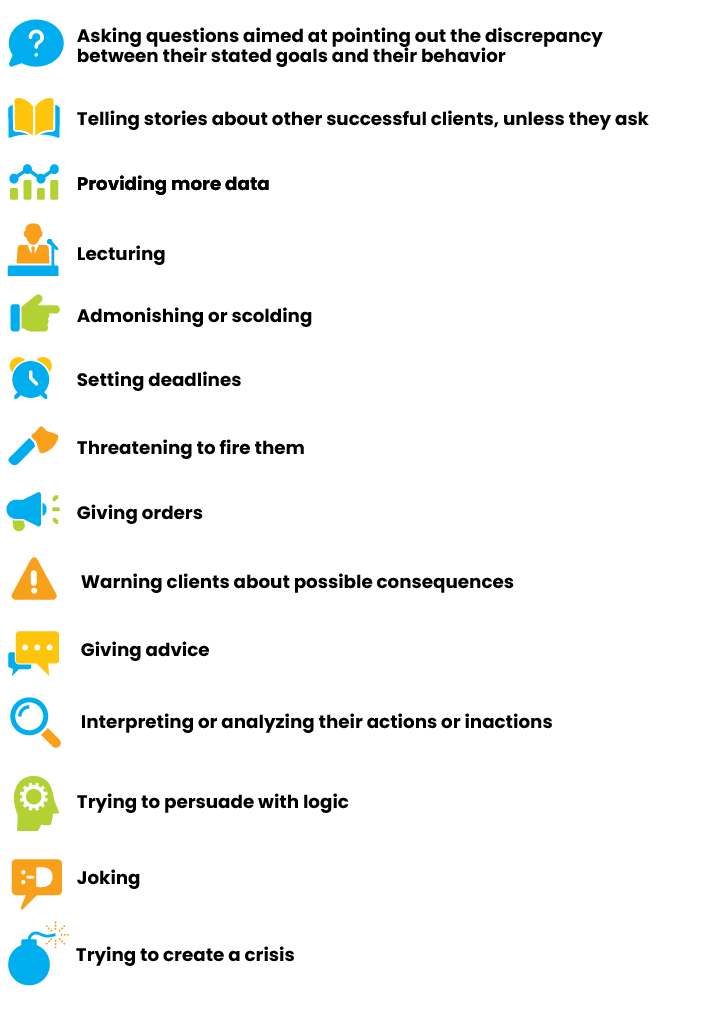

When a person is at any stage other than action, it is important that you do not do any of the traditional things we consider as helping. When your clients are in pre-contemplation, contemplation or preparation, they are not yet ready to change. They are ambivalent about changing and you can either increase the chance they change or cement them deeper into continuing the problematic behavior. And sadly, most of what we are taught to do to help people is only applicable to the 20% of our clients who are in the action phase.

When a person is in pre-contemplation, contemplation or preparation, if you take any of the actions in the chart below you will get the opposite of what you are hoping for:

Your Job

So, what can you do? Your job is first to listen and to try to assess where they are in the change journey. And don’t worry if you guess the stage wrong; your client will let you know by resisting your input. Rather than being annoyed, look at the resistance as a signpost telling you where they are. You thought they were in preparation; guess not. Time to slow down.

Your second job is to elicit the three components necessary for change:

Belief that change is important now.

Confidence that they can change.

Readiness to make that change happen.

For the moment it is important to put your ideas, expertise and advice aside and be present with that person. Ask questions about why they want to change and don’t argue with their reasons or give them additional reasons. Ask about times they’ve made changes in the past and why they think they were able to do so. Ask if they can see themselves using similar techniques, strengths or strategies with the current issue. Ask them again why they want to change now and, again, don’t argue or tell them why now. Your job is to listen and to honor where your client is on his or her or their journey now.

If you push for change too soon, you may slow down their change and you could alienate them. I encourage others, and myself at times, to remember that there are times that I can be right or times that I can be connected. I choose to be connected. After all, even the best financial plan is worthless if the plan isn’t followed.

Julia Kramer, CPA, CFT- I, is a certified financial behavior specialist and owner of Iaso Consulting LLC.