Millions of older Americans fall victim each year to some type of financial fraud or internet scheme and their reported losses are surging, according to a new report from the Federal Bureau of Investigation’s Internet Crime Complaint Center (IC3).

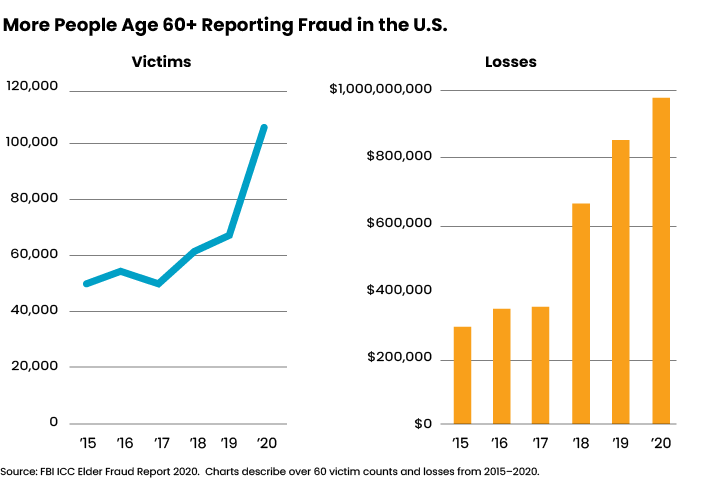

The 2020 IC3 Elder Fraud Report, published in June, notes that victims over age 60 accounted for 28% or nearly $1 billion in total fraud losses reported to the IC3 in 2020. That’s approximately $300 million more than the losses they reported in 2018 and roughly triple the 2017 figure.

As steep as these reported figures are, the FBI estimates that seniors actually lose more than $3 billion each year to financial fraud. The huge reporting gap is attributed to a couple of factors.

First, many seniors don’t report fraud because they’re embarrassed, afraid, worried their families will take away their independence, unsure how to report it, or unable to supply details to investigators, notes the FBI. Second, the Internet Crime Complaint Center only sorts reported losses into the over-60 category (or any age category) if the person provides their age range when filing a complaint; this is optional.

Even so, complaints from victims over 60 jumped 55% between 2019 and 2020 (from 68,013 to 105,301), as more seniors turned to the internet for online shopping, social media and other needs during the pandemic. Victims over 60 lost an average $9,175 in 2020, and 1,921 of them lost more than $100,000.

Several pieces of bipartisan legislation have been introduced this year with the aim of protecting the U.S.’s older population from financial scams. Financial advisors are also educating their clients about the risks and taking additional measures to protect them.

Don’t Pick Up the Phone

While internet scams receive a lot of attention, Peter Creedon, CFP, the CEO of Crystal Brook Advisors in the Greater New York City area, also cautions about phone scams. Although fraudsters may be more likely to victimize lonely seniors, anyone can be fooled, he said.

“I always tell all clients to be careful. Never give a Social Security number over a phone — I don’t care who it is,” he said. “Scams stress urgency, create fear and cause you to react. You need to step back; sometimes these actors are very good.”

One of Creedon’s clients, a business owner, received a call on his cell phone purportedly from the electric company. The caller threatened to turn off power that day at the client’s workplace. Later on, a guy wearing a shirt with the power company name or logo showed up at the client’s workplace. The business owner couldn’t afford to lose power on that busy workday so he paid $200 in cash to the man who said he couldn’t accept a check.

Afterward, Creedon’s client called the power company, which told him it doesn’t make those kinds of calls and it never sends anyone out to collect money. With scams like these, “It’s kind of obvious afterwards, but the timing and luck can catch you off guard,” said Creedon. “They go after the small guy wearing three to four hats.”

“It’s a far cry from the Nigerian prince (scams),” added Creedon, “but how many times a day are you called from numbers that look local?” Directories and exchanges sell phone numbers, and scammers keep up with technology, he said.

Like many of us, “I was getting inundated with IRS calls,” said Creedon, although the IRS sends letters. He encourages people to reach out to the Federal Communications Commission to report calls that imitate government employees. “If someone is calling for the IRS, they’re going to jump on this stuff real fast,” he said.

Creedon also lets phone calls go to voicemail and looks up company phone numbers on their websites rather than calling back incoming numbers. While this is now routine for many, it’s helpful to remind clients to take these extra steps. He also emphasizes the importance of keeping computers and cybersecurity plans up to date.

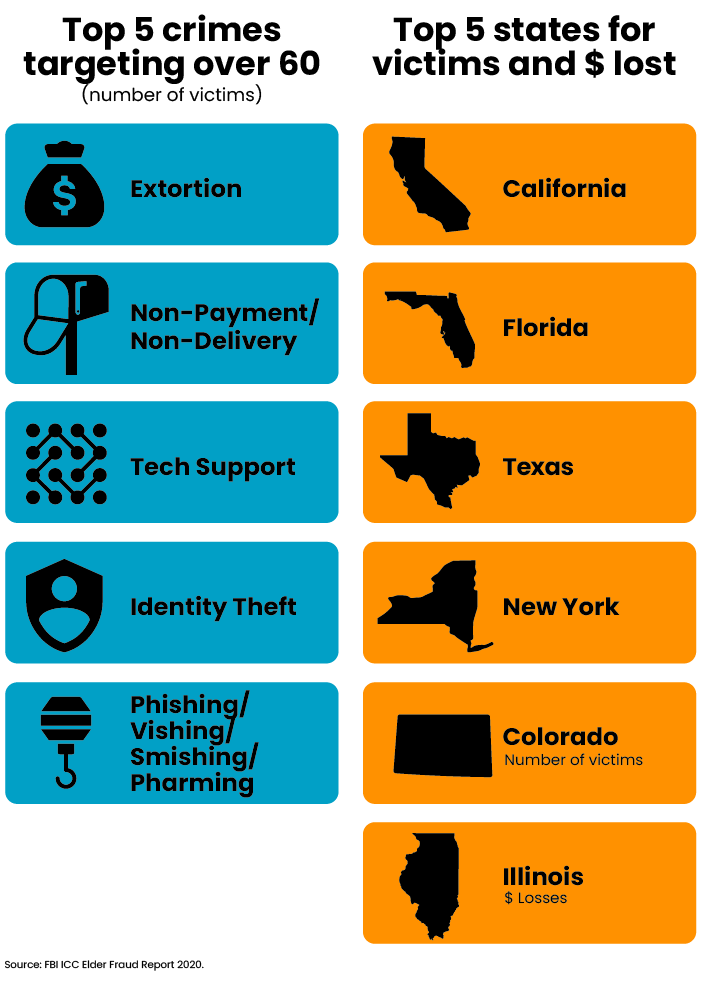

According to the IC3 Elder Fraud report, 23,100 victims over 60 lost money in 2020 through extortion. The second most common crime last year, non-payment/non-delivery of products, impacted 14,534 seniors.

Seniors lost the most money in 2020 through confidence fraud/romance scams, which are “designed to pull on the victim’s ‘heartstrings,’” noted the report. In total, 6,817 victims over 60 reported losses exceeding $281 million. This increasingly prevalent crime category includes grandparent scams — when perpetrators impersonate a loved one claiming to be in trouble and in immediate need of money.

Advisors should caution clients that scammers sometimes discuss personal information they know about their victims in order to make the communications seem legitimate.

The scammer who called William H. Webster in 2014 under the pretense of a Jamaican lottery win told him he did a background check and knew Webster was a judge who’d been in the U.S. Navy. What the criminal failed to uncover was that Webster had been director of the FBI and the Central Intelligence Agency.

Webster, now 97, and his wife recorded several phone conversations to help catch the caller, who is currently incarcerated. Webster created this video a couple of years ago, which includes the recorded conversations, to educate the public. During one call, the perpetrator threatened to kill the Websters and burn down their house.

Unsuspecting Smugglers

Seniors have also been conned into serving as drug mules for international drug trafficking rings. The New York Times recently reported on Victor Stemberger, an American septuagenarian sentenced two years ago to a seven-year term in Spain after being caught unwittingly smuggling cocaine for a Nigerian-based cartel.

Stemberger, a corporate coach who earned two master’s degrees and served 24 years in the U.S. Army, traveled from his home in Virginia to pick up a package in Brazil and deliver it to Madrid. Cocaine was sewn into jackets stashed in his luggage. During his trial, a medical expert testified that Stemberger’s logic and decision-making abilities were impaired by a brain aneurysm suffered in 2005 — but that didn’t keep him out of prison.

Stemberger is just one of many seniors whom drug traffickers have preyed upon. As of early 2016, the Department of Homeland Security (DHS) was tracking 144 cases of older adults being duped into acting as unwitting drug mules.

U.S. Senators Tim Kaine and Mark Warner of Virginia cited this statistic in letters they wrote last fall to the U.S. Departments of State and Homeland Security to ask what they were doing to help their constituent Stemberger and other seniors manipulated by drug traffickers. They expressed concern that Operation COCOON, DHS’s program to target drug traffickers who manipulate older Americans, may be endangering rather than protecting these unsuspecting victims.

Sen. Kaine’s communications director, Katie Stuntz, told Rethinking65 in an email that the senator continues to press for the immediate humanitarian release of Stemberger, now 77. He has been incarcerated in Madrid since July 2019.

“This scam has highlighted the disturbing trend of drug traffickers targeting older vulnerable individuals who have suffered from significant health challenges that limit their cognitive abilities,” added Stuntz. “Senator Kaine is in touch with both DHS and the State Department about Victor’s case and what more the U.S. government can do to prevent these scams in the future to protect older Americans from unknowingly becoming victims.”

Psychological Thriller Prompts Vigilance

Michelle Rand, founder and CEO of Cascade Investment Advisors Inc. in Oregon City, Ore., works with an older couple that had their identity stolen. The husband received a phone call and wasn’t savvy enough to recognize he was being conned, she said.

“He was beguiled into giving out information about credit card bills,” said Rand. “We rapidly alerted Schwab to put an extra layer of security on his account and we put their daughter on as durable power of attorney so she could watch the accounts.”

The daughter handled changes to his checking and credit card accounts although he raised the alarm about fraud to his credit card companies, said Rand.

Rand’s increased vigilance in fraud prevention began a number of years ago while visiting a client in Australia. During this trip, Rand started reading the psychological thriller series “The Girl with the Dragon Tattoo,” by Stieg Larsson, and was intrigued.

“It was this epiphany for me: ‘Oh my god, we’ve got to pay more attention to security,’” she said.

Rand now encourages clients to set up two-factor authentication to access their accounts. She also trains them to contact her team if they make significant withdrawals from their institutional accounts. Even so, “We pretty much watch every transaction, every day in every [institutional] account,” she said. “If it’s not scheduled and the client doesn’t call us, we call the client.” If they can’t reach the client, they call Schwab.

“You can’t do it alone; clients have to help you,” she said. “If they’re sloppy, that’s not good.”

Cascade Investment Advisors uses a virtual private network (VPN) that, unlike a browser, “cloaks your IP address,” said Rand. She tells clients about VPNs and said more tech-savvy clients use them. Her firm also made the decision early in the pandemic to ban Zoom because its app was hacked a number of times when everyone was flocking to it.

“We don’t just go with the flow on these things; products have to pass our cybersecurity review in order for us to adopt them,” she said. When she and her team looking into Zoom, they felt it hadn’t worked hard enough to be in the enterprise space. “Fine for family, not for running alongside my client data on my computer,” said Rand. Instead, she pays for a subscription to GoToMeeting, a long-time resource for businesses. She also encourages business owners to step up their systems security measures.

During the pandemic, a client called to tell her that false unemployment claims had been filed and were being paid out in the names of many high-paid employees in the client’s office. “It’s just abominable; it’s worse than bad,” Rand said, describing the security technology used by the state.

Playing Detective

On a personal note, Rand said she calls her credit card company every two years to request a new card to shake off any fraudsters who may be following it. She has also done some sleuthing in her free time.

When a neighborhood teen received a check written on Schwab Bank for an old Mustang he listed for sale on an online service, for the full amount plus prepaid shipping charges to send the car to the East Coast, his father was alarmed and reached out to Rand.

Rand did a cross check and discovered the buyer was an attorney. “As a complete shot in the dark, I emailed him at 10:30 at night and said, ‘It doesn’t seem like you’re the kind of guy purchasing a crappy blue Mustang that needs a lot of work,’” she said. “He emailed right back and said, ‘I’m not. I’ve been scammed.’”

The attorney told Rand he put an alert on his account and asked her for advice. “The scammer digitally got the signature from this guy, probably from court filings on the Internet, and scanned and reproduced it,” said Rand. “It looked completely legit.”

Legislative Outlook

Protecting older Americans from fraud is one area that both sides agree upon in an increasingly partisan Congress. In April, Senators Susan Collins (R-Maine) and Amy Klobuchar (D-Minn.) introduced the Seniors Fraud Prevention Act. The bill would create an office at the FTC to fight scams targeting seniors.

“Raising awareness — particularly among older Americans who are more likely to be targeted by financial scams — and cracking down on ruthless criminals are the keys to protecting seniors’ hard-earned savings,” Sen. Collins said via email. “We have made substantial progress to combat fraud, and we must not relent in our efforts to stop con artists.”

“The Seniors Fraud Prevention Act I introduced with Senator Klobuchar would enhance fraud monitoring, increase consumer education, and strengthen the complaint tracking system to help prevent seniors from becoming victims of threatening and manipulative scams.”

In July, Sen. Collins and Sen. Kirsten Gillibrand (D-N.Y.) introduced the Senior Empowerment Financial Act that would standardize and improve how senior financial abuse is reported, establish a national hotline to advise seniors on where and how to report fraud, and provide additional resources to fight and prevent financial exploitation of seniors.