While millennials in general may not be hot prospects at the moment, the young adult children of your best clients may be another matter. If you want to keep managing that money once it is passed to the next generation, then you need to start making millennial marketing part of your strategy.

Consider these statistics:

• According to a survey by Investment News, 66% of children fire their parents’ financial advisor after they inherit their parents’ wealth.

• Some estimates put this abandonment figure at more than 95% and three-quarters of investors say their children have never met their advisors, according to this article published by the Illinois CPA Society.

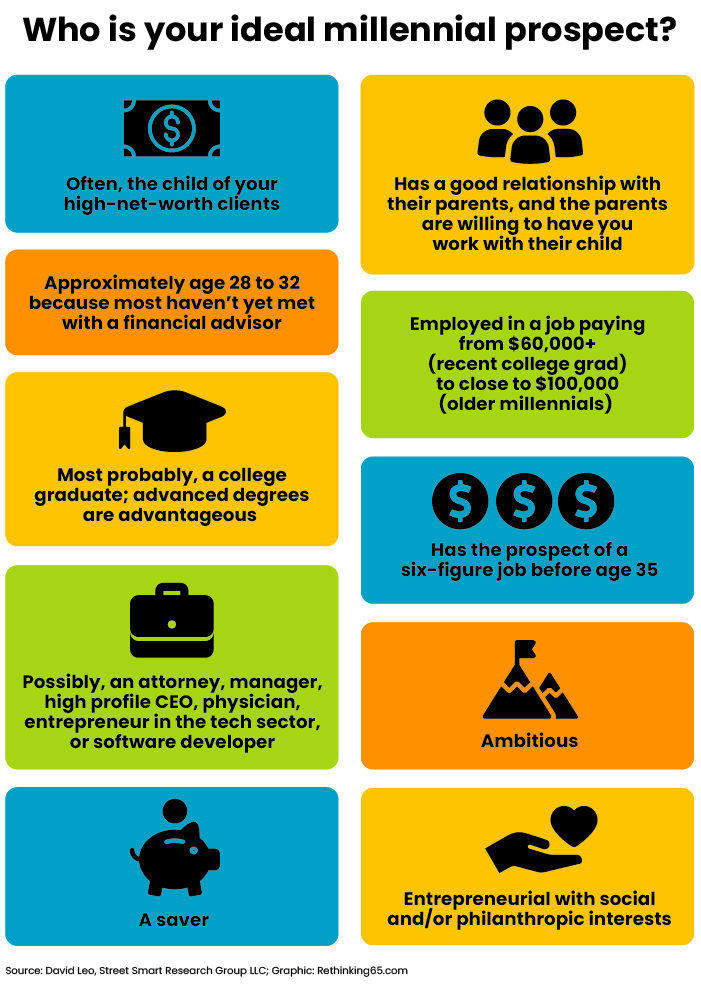

There are about 72 million Americans between the ages of 25 and 40. So what portion of these millennials should financial advisors be working with? The short answer is you primarily should be marketing to the adult children of your high-net-worth clients.

At what age should you catch clients’ children?

Ideally, financial advisors need to establish relationships with millennials before they reach the age of 35.

A recent Horsesmouth Chart Talk feature, “Prospecting the Younger Investor,” reported that about 60% of affluent investors met with their first financial advisor before the age of 45. Data from TIAA shows about a third of people in the group have already met with a financial advisor before they are 35.

Many advisors have increased their focus on millennials, not least because it is known that a high percentage of children will move inherited money to a new financial advisor. Don’t let the competition grab your clients’ children.

Getting clients involved at a young age can also score points with their parents.

Although many wealthy clients want to leave an inheritance to their children, only one in five strongly agrees that their children will be well prepared to handle family wealth they’re likely to inherit, according to a study from U.S. Trust. Four in 10 respondents over age 70 don’t believe their children are ready to handle family wealth until at least age 40.

And while most wealthy families surveyed by U.S. Trust say their family would benefit from establishing a set of principles to guide the purpose of their wealth, less than half have. Only one in 10 have developed a family mission statement that reflects the values and wishes about how the family’s wealth should be used.

Meanwhile, nearly half (48%) of respondents to an RBC/Campden Wealth survey worry their children will lose the wealth their family built. And they should be worried: 70% of wealthy families lose their wealth by the second generation and 90% by the third generation (data frequently attributed to the cited Williams Group wealth consultancy).

These are good talking points for discussion with your wealthy clients, especially those older ones. I also suggest putting a plan in place today to develop relationships with the adult children of your best clients.

Do millennial assets make it worthwhile?

Financial advisors are concerned about whether or not the millennial marketplace has enough assets to warrant the effort. It’s a good question.

Factors to consider include the wealth and age of parents, age and occupation of children, which colleges the children graduated from or are attending, their family situation, their interests, how committed their parents are to having you work with their children, the number of children your clients have, their relationship with their children and so on.

It is not likely that most millennials have enough wealth to warrant marketing to them as a specialty. However, for newer financial advisors, some millennials can be both profitable and also serve as an important learning opportunity in building their businesses and experience in marketing, sales, and service while helping younger investors.

In larger, mature practices, contact with the millennial children of high-net-worth clients is about developing a multigenerational practice as a longer-term plan to retain the assets of your older clients and, on some cases, to earn the assets of your competitors’ HNW clients.

What should your millennial service strategy include?

Millennial clients should not take an inordinate amount of time. You have to strike a balance between time spent and potential for asset retention or growth based on your clients.

A millennial strategy would primarily address only a subset of your clients, e.g., the top 20% or 30% of your clients that provide 80% of your revenue and assets. I am thinking of clients who have or will have, perhaps $2 million to $3 million or more and who have three or fewer adult children. I should also note that the financial advisor should have the agreement of the parents to engage in a relationship with their adult children.

You should have “regular contact” with adult children of HNW clients, but there would not likely be lengthy in person meetings. Even if the millennial children of your top clients are not your clients, yet you may also want to speak with them perhaps twice a year and meet occasionally to build that relationship. Included in your strategy would be educational and other events, emails of relevant articles, research relevant to millennials, e.g., Bitcoin, Tesla, ESG, etc. and even your experience in educational, personal and career development in appropriate cases. [According to the recent CNBC millionaire survey, nearly half of millennial millionaires have at least 25% of their wealth in cryptocurrencies.]

If the millennial becomes a client, you should offer them your core set of deliverables, including, but not limited to, financial planning, liability, estate and risk planning as appropriate, and so on. Once they become clients, scheduled meetings will in part be a function of their asset level and that of their parents, assuming they are also clients.

Who are current and potential millennial investors?

There are already approximately 618,000 millennial millionaires, according to WealthEngine data cited in a 2019 report from Coldwell Banker. https://blog.coldwellbankerluxury.com/wp-content/uploads/2019/10/CBGL-Millennial-Report_SEP19_FINAL-4a.1-1-1.pdf]. And over the next 30 years, the U.S.’s 72 million millennials are expected to inherit $68 trillion from baby boomers.

Back when Fidelity conducted its 7th Millionaire Outlook Study in 2014, which explored the wealth potential across all ages, the average age for the emerging affluent was 40. The oldest millennials, born in 1980, are just past this threshold now. Many more millennials will be turning 40 in the next five to six years and they too may soon be seeking advice because the majority (90%) who don’t use an advisor feel they aren’t knowledgeable enough about investments to make decisions on their own.

A handful of years ago, there were already 720,000 young adults in the millennial 1%, earning over $100,000 per year, and another 7 million millennials in fields that offer salaries of about $60,000. These folks need help — especially if they are children of your clients.

What do young high-net-worth individuals want?

What do young high-net-worth individuals want?

Millennials need evidence and logic to support their investment decisions. Many also tend to be self-directed or want to be part of the decision process. Educating millennials and offering transparency on how you get paid can help you establish trust.

You need to discuss your comprehensive offerings that go well beyond investment management, and that your services go well beyond what discount brokers are offering. You should also understand the drivers and deep interests of millennials that go beyond money, whether community service, politics, or other.

The majority of younger people have little experience with investing, “wealth management,” and even money in general. But like most of us, they don’t want to fail. You can point out to them, just like to their parents, that data shows 70% of wealthy families lose their wealth by the second generation, and a stunning 90% by the third. Help is needed.

You can also play an important role in helping these constituents develop a healthy relationship with money and investing — if one does not exist — by helping provide financial education on compounding and other important concepts.

Each of these factors is part of your discovery process, the process by which you get to know your clients and their families. This is especially important with your high-net-worth clients — those whose assets you would like to retain in perpetuity.

It’s time to get your millennial strategy in place. If you collaborate with the right millennials, they can grow into top clients.

David Leo is the founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant and trainer to financial professionals. If you would like more information about his services, contact him at David@CoachDavidLeo.com or visit www.CoachDavidLeo.com.