Although health savings accounts have been available since 2004, these triple tax-free tools haven’t caught on as widely as they could have, and many people who own HSAs are not using them to their full advantage.

In fact, now would be a good time to remind clients with these accounts that they have until May 17 to make 2020 contributions under the extended tax deadline. The maximum contribution limits for 2020 are $3,550 for an individual and $7,100 in total for families. There is also a $1,000 catch-up provision for accountholders age 55 and older.

Many people continue to shy away from HSAs because they assume they won’t be worth it since they must be used in conjunction with a high-deductible health plan (HDHP). According to KFF, 20% of firms offering health benefits in 2020 offered an HSA-qualified HDHP. The benefit is more common at firms with 200 or more workers (52%) than at smaller firms (19%). Nearly one quarter (24%) of covered workers across all firms are enrolled in an HSA-qualified HDHP.

Lack of information has also kept many HSA owners from fully embracing the power of these accounts, which offer tax-free contributions, tax-free earnings and tax-free withdrawals.

“You would be shocked at how many people have been in an HSA for years and have never realized that they actually have the ability to invest,” says Kevin Robertson, chief revenue officer of HSA Bank, a leading HSA administrator. Part of this challenge is lack of awareness, he says, and the other part is hesitancy to plan for healthcare needs 20 years down the road. “Life gets in the way,” he says, as with other retirement planning.

According to the Employee Benefit Research Institute (EBRI), only 56% of accountholders age 55 to 64 made a contribution to their HSA in 2019. Yet time is running out for this group: Accountholders aren’t permitted to make contributions to HSAs once they enroll in Medicare.

Only about 7% of all HSA accountholders invested at least some portion of their account balance in 2019, according to EBRI. Not only could accountholders use some education about the investment power of HSAs, they should also be reminded to check their balances. At the end of January, about 18% of the industry’s 30.2 million HSAs were unfunded, according to Devenir, a leader in HSA investments.

“The longer people have an HSA, the more likely they are to invest, but even then you’re only getting up to 10% to 13% investing among people who have had an account for a decade or more,” says Paul Fronstin, director of the Health Research and Education Program at EBRI.

“We need to better understand why people aren’t investing, because I would argue most people should be investing in their HSA, even though they have a high deductible,” he says. His argument is based on healthcare’s 80/20 rule: Only 20% of the population accounts for 80% of healthcare spend.

“The flipside of that is 80% of the population uses very little healthcare,” he says, and most won’t reach their deductible. So the many people with health insurance who use no or next to no healthcare in any given year should be in a position to invest in an HSA, he says.

To encourage clients to take advantage of their HSA, advisors should remind them that “from a tax perspective it’s the best thing out there — the money goes in tax free, builds up tax free, and comes out tax free if you use it for a health service,” says Fronstin.

“And for somebody who uses a lot of healthcare who is never going to invest and never going build up a balance,” he says, “I think the conversation is, ‘You should still be putting money in the account — just take it out when you need it and at least you get the tax break on it.’”

Building balances can be challenging since, unlike retirement accounts, HSAs are designed for owners of any age to take distributions; the majority of accountholders 35 and older do.

At the end of 2020, the average HSA balance for accounts with contributions was $4,782 for accountholders 45 to 55 and $5,814 for those 65 and older, according to EBRI. Many advisory clients could be saving more than they are and probably would if they remembered how much pre-tax dollars they could stash away.

The maximum 2021 contribution is $3,600 for individuals, $7,200 in total for families. Accountholders age 55 and up can also make a catch-up contribution of $1,000. So can a spouse in this age band (for a total family contribution of $9,200), but only if they have their own HSA, notes Robertson. Individuals with high-deductible plans can open HSAs even if their employer doesn’t offer one or if they’re self-employed or unemployed.

Every bit of savings helps. According to Fidelity, a 65-year-old couple that retired in 2020 will need about $295,000 for medical expenses in retirement excluding long-term care.

“Advisors can do a really great service to their people by saying, ‘Look, this is a need; we need to prepare for this; and the earlier you start, the better off you are,’” says Robertson.

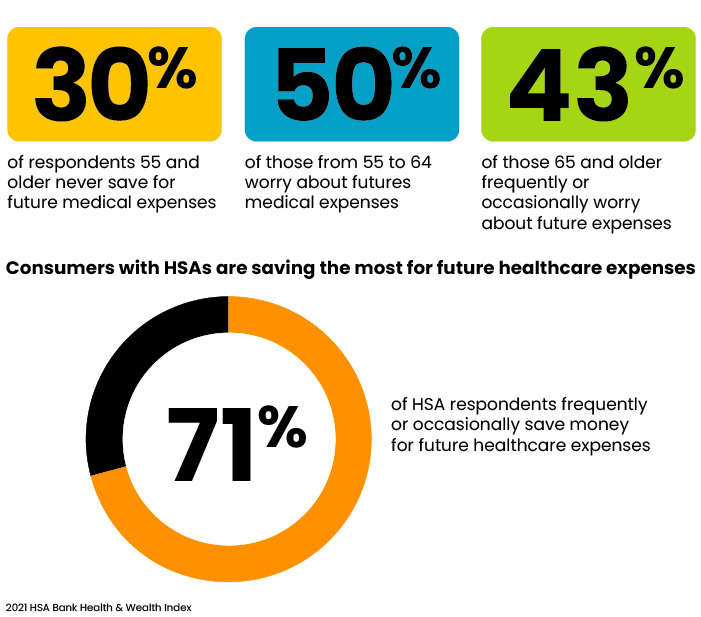

There is a great disconnect between being concerned and being proactive about healthcare costs. Nearly all respondents 55 and up (93%) surveyed for the 2021 HSA Bank Health & Wellness Index worry about future medical expenses, yet 30% of this group never save for them. In the survey, baby boomers (56 to 75) scored lower on health and wealth engagement than any group except for Generation Z (age 18 to 24).

Robertson isn’t surprised. Regardless of their generation, few Americans really have a deep understanding of their health insurance and medical benefits, he says. While individuals with health insurance coverage generally feel they’ll be taken care of should they face a significant problem, such as cancer or a heart attack, they lack an understanding of “the day-to-day utilization of benefits,” he says, “or the nuances of stretching healthcare dollars further.”

HSAs give people the opportunity to be more engaged in their healthcare decisions, says Robertson. Although savings rates can use improvement, the HSA Bank Health & Wellness Index found that 71% of respondents with an HSA frequently or occasionally save money for future healthcare expenses, compared with just 54% of respondents with a PPO (preferred provider organization).

Robertson encourages accountholders to divide their HSA balances into three investing buckets — a near term bucket of “instant funds” held in cash (maybe $1,000 for a couple), a long-term bucket that can be invested more aggressively depending on the time horizon before distributions will be needed, and an intermediate bucket for qualified medical expenses one will start to incur in a year or so (such as premiums for Medicare Part B and Part D for someone who will be turning 65 and starting Medicare).

Do the Math

“HSAs are not going to be for everyone, and they’re not going to be perfect in everyone’s situation,” says Robertson, but “the connotation that a high deductible means that it’s going to be a higher out of pocket really has been eroded, and that’s not necessarily the case anymore.” The lower premiums that may come with a high-deductible health plan could be well worth it.

Even if the savings on the premium versus the higher deductible “essentially make it a wash,” he says, every dollar put into an HSA helps save on taxes.

Financial advisors can add a lot of value by sitting down with clients to look at plan options and figure out the best choice, says Robertson, who notes that there are a lot of free online calculators to compare traditional and HSA-based health plans.

“I cannot underscore the importance enough of doing the math — it’s not that complicated, it’s not that scary, but the good news is, even if you don’t select an HSA based plan, you’re going to exit from that analysis with a better understanding of your health plan, a better understanding of the attributes like deductible and out-of-pocket and copay and coinsurance and all of that,” he says, “and after all, that’s a win.”

A couple of other nice benefits of HSAs are no required minimum distributions and no time limit for qualified reimbursements, notes Robertson. As long as accountholders hold onto their receipts for qualified medical expenses, they can let their investments appreciate and take those reimbursements at any point in the future that makes financial sense for them. Misplace a receipt and find it years later? Not a problem.

Here’s another potential benefit that may be relevant to your clients — or to you. A child under age 26 who is not a tax dependent but still on a parent’s high-deductible health plan, because it makes more economic sense (say a 24-year-old employed college graduate), can independently contribute up to the family limit in an HSA even if their parents contribute up to this limit in their own account(s), says Robertson.

“It’s kind of an interesting nuance and often missed by a lot of advisors as well,” he says.

Robertson is hopeful legislation, such as the bipartisan Health Savings for Seniors Act, introduced in the House by Rep. Ami Bera M.D. (D-Calif.) and Rep. Jason Smith (R-Mo.), will eventually allow seniors on Medicare to contribute to HSAs. Although the bill probably lost some attention last year amid the pandemic and presidential election, “we remain optimistic and vigilant that this or a similar provision will get passed,” he says. “There’s a groundswell of support for that notion.”

Jerilyn Klein is editorial director of Rethinking65.

Limits Likely to Help Older Americans Most")