Tom Brady and the Tampa Bay Buccaneers won this year’s Super Bowl because they executed a better game plan on all fronts. Patrick Mahomes and the Kansas City Chiefs appeared frustrated, confused and defeated long before the final whistle blew.

When it comes to paying for college, parents today resemble the Kansas City Chiefs. Families are using an outdated, ineffective playbook that results in financial defeat.

Parents think they should get their kids to and through college and then get serious about saving for retirement, and this error could sabotage their retirement savings efforts. And although college can be the perfect “wake-up” call for parents to get their financial house in order, they’re often hesitant or unable to find the kind of guidance and expertise they need to create the best possible outcome for their situation.

Also, unlike retirement, parents can’t move the goal posts on college another five or six years and tell their children they’ll have to wait until they’re 23 or 24 to begin their bachelor’s degree.

Balancing college and retirement savings is often particularly stressful for those parents who’ll be in their late 50s or 60s when their kids graduate from high school. While some of them got a jumpstart on building their assets in the decades before their children were born, older parents often have less time left on the work clock to earn money, save money and repay financing costs associated with college costs. I usually say they “have less runway.”

If only we explained to the parents of newborns that they would be buying two houses — one to live in and make memories as a family, and one as the halfway house their kids will occupy as they transition into adulthood. Families could understand they need to save/invest for the “down payment” and then look to financing strategies that allow them to maintain their current lifestyle while staying on track for retirement.

Older parents who have not saved for the down payment on college will be forced to look at financing a higher percentage of the overall purchase price. I think they’ll have to come to terms with the kids taking on student-loan debt that the kids will pay off (instead of the kids taking the loans and the parents making the payments to the kids to pay them off).

It’s important to do some stress testing to see how much extra cash flow the parents are likely to have in retirement. Parents may decide they will work another year or do some consulting in retirement — sort of a Chapter 2 approach to staying active and leveraging their skills and experience, but not enduring the stress of a fulltime job.

The Parent Plus loan may play a role for older parents — at the current lower interest rates. Because they can take a longer time to pay those loans back (the Department of Education does offer a 25-year repayment option!) and the loans are forgiven upon death, this becomes a smart move if there is a much older parent in the mix.

More than anything, older parents have to be prepared to talk to their kids about what’s “affordable.” They cannot go blindly into this and figure out the game plan after the student has accepted admission. They must begin with the end in mind and back into applying to colleges they can afford.

The whole notion of “saving” for college is flawed. As prices of a four-year bachelor’s degree have increased exponentially, it has become almost impossible for most families to set aside enough money to fund all four years — for each student — out of savings and investments.

And paying for college is not a savings or investment exercise like retirement; college is a current lifestyle expense. Like cars and houses, it’s a major capital purchase — something families buy that they can’t pay for fully with monthly cash flow. Unlike buying cars and houses, however, families often don’t know the price of the college education they are purchasing until after the fact — the single biggest financial mistake they make in this process.

To put this in more familiar financial terms, it’s unthinkable to go house hunting in a zip code you aren’t pre-qualified for by the lender; when it comes to college, families are touring campuses and applying for admission to schools they shouldn’t even be considering.

In his new book, “The Price You Pay for College,” Ron Lieber states, “For many families, the total bill for college could well add up to more than what they paid for their homes” and “This is the most complex and emotionally fraught financial decision that many families will ever make.”

Surprisingly, families have more financing options for higher education than they do when buying vehicles and real estate — they just don’t know it, or how to put them together.

Back to the Super Bowl: Families and their advisors need a better game plan on all fronts. Let’s start thinking like the Buccaneers. Tampa Bay didn’t do just one big thing really well; they did a lot of little things really well. It was the overall balance of their game plan that put them in the lead and kept them there. A playbook that balances offense, defense, special teams — that’s the approach families and their advisors need to take towards paying for college.

In simple terms, the game plan we need to share with our clients is, “Finance their future, fund yours,” referring to children’s education and clients’ retirement.

Parents with college-bound students have three competing priorities:

1. Maintain their current lifestyle.

2. Fund their retirement.

3. Pay for college — all kids, all years.

The fact is, as an industry we direct parents to save for college but we do not do a particularly good job of helping them save on college.

Too many families are left to a DIY approach to paying for college: Save/invest what they can, pay from current cash flow, reduce contributions to retirement plans during the college years and take on debt as a last resort. And by the time they realize this approach isn’t getting the job done, parents begin to resemble Patrick Mahomes during the 4th quarter of the Super Bowl — they begin to scramble and panic and go down in total defeat, wondering what just happened.

The Buccaneer’s playbook for paying for college would look more like this:

Offense

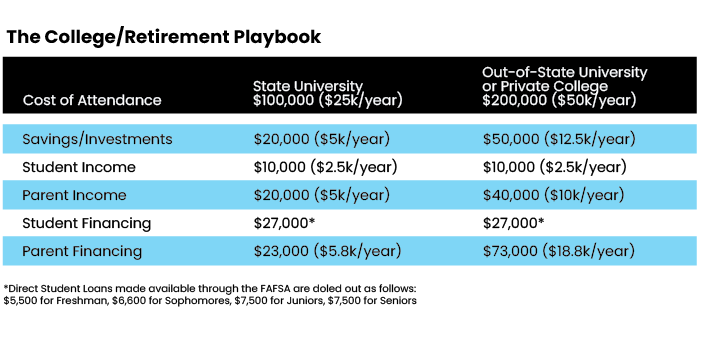

1. Save/invest 20% to 30% prior to the college years (think of this as the down payment on the college purchase).

2. Plan on directing 30% of current lifestyle cash flow toward the cost of college each year the student is in school (5% to 10% is from student-earned income — all colleges assume the student works and earns money to put toward their education each summer; 20% from parent-earned income).

Defense

Maintain parent contributions to retirement plans.

Special Teams

1. Student financing: Take 100% of the federal student loans offered to undergraduate students (see chart below).

2. Parent financing: Look for the most cash-flow-efficient financing options available. Examples include a home equity line of credit (HELOC) and insurance contract loans that are interest-only loans.

Should any parents consider changing their 401(k) contribution amount to save more for college? Or should they always max out on 401(k) contributions first? It depends. This question is exactly why a retirement income/sustainability forecast must be done when discussing the “cost of college.” It’s not just the current cost we need to evaluate; it’s the impact the cost of college will have on the parents in their mid-to-late 70s and 80s that we need to look at!

This is the “ah ha” moment for most parents’ understanding of how the decision to educate their kids impacts their life much later down the road. I like to tell parents, “Let’s not hand over your hard earned capital to colleges today; let’s finance those costs and keep that money on your balance sheet so you can take Disney cruises with the grandkids.”

Beth V. Walker is a wealth advisor with Carson Wealth Management and founder of Center for College Solutions, which is based in Colorado Springs, Colo. She can be reached at bwalker@carsonwealth.com or 719-522-2278.